Appendix 1: Simple Excel Automation Example

The embedded 401(k) calculator requires the user to enter the desired % deduction from remaining payments to meet the desired year end total contribution amount to the 401(k). That is:

- Make the sum of the deductions for the year (name this calculation cell “SetCell”) equal to

- a desired value (the allowable value in section III. of the calculator. Name this cell “ToValue”.)

- by changing the % in section IVa. of the calculator (Name this cell “byChanging”.)

Note: In Excel, you can name specific cells or ranges of cells. Formulas are a little more intelligible if they use names.

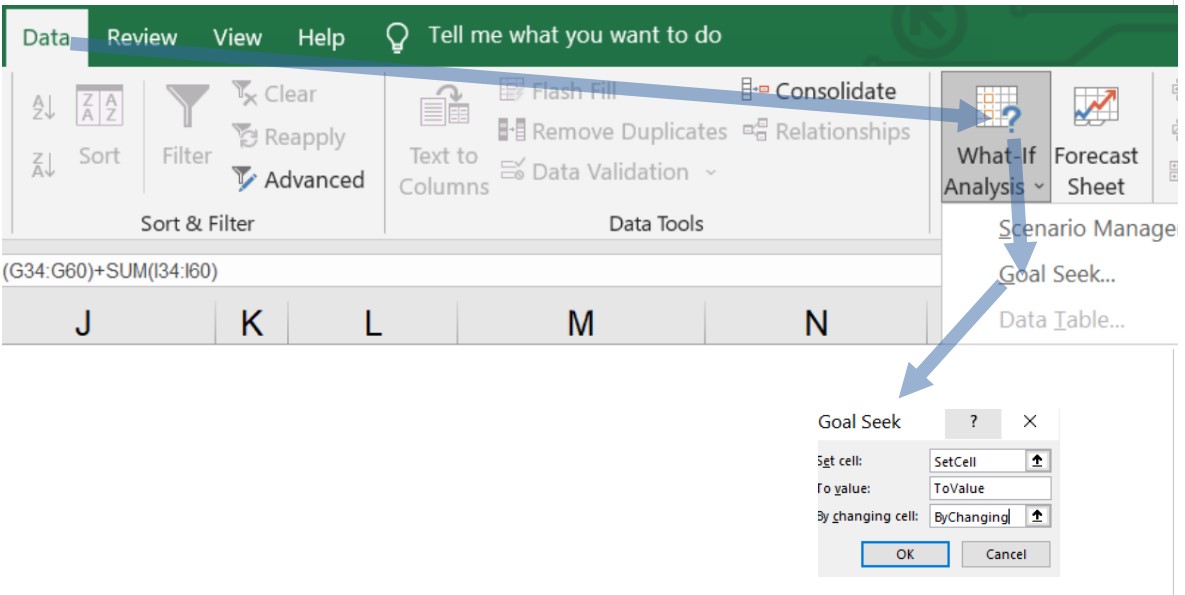

In Excel, from the top Ribbon, choose Data/What if Analysis/Goal seek to get the Goal seek box you see in Schematic 1.

Schematic 1: Excel Ribbon Menu Commands for Goal Seek Function

If we enter the values as shown in the Goal Seek box and hit OK, excel will do an iterative calculation and arrive at the solution (26.26% in example 1). Note: not quite…. an actual value has to be entered into the To_value box but in the automated version described next, we can substitute with “ToValue”.

Now, how can we automate this so the user doesn’t have to execute each of these steps manually?

First, we write a little program using a built in programming language called VBA. It will look as follows:

Private Sub CommandButton1_Click()

‘ Use Goal Seek to compute fixed percentage deduction from

‘ remaining paychecks to meet end of year total 401k deduction

‘ target

Range(“SetCell”).GoalSeek Goal:=Range(“ToValue”), ChangingCell:=Range(“ByChanging”)

End Sub

Let’s embed the little program above into a calculation button so the user can conveniently press the button and get a solution.

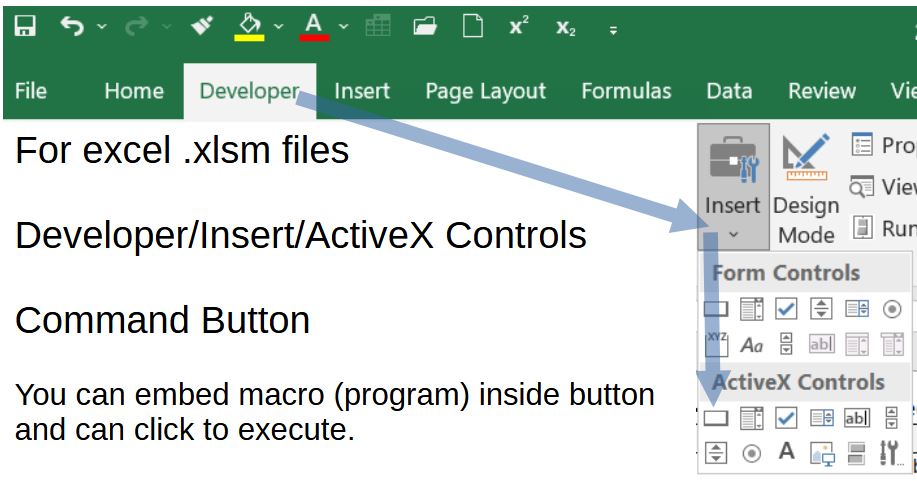

In Excel, from the Top Ribbon, choose Developer/Insert/ActiveX Controls Command Button. See Schematic 2.

Schematic 2: Excel Top Ribbon to Command Button

The button (just choose “properties” and “right click/view code” to set up) is then easily set up and formatted.

Then click on the button to execute the command.

Cool.

Note 1: You must save the excel file as an “.xlsm” type in order for VBA programs to work.

Note 2: The term “macro” is used to describe these automated programmed steps (see more on this term here).