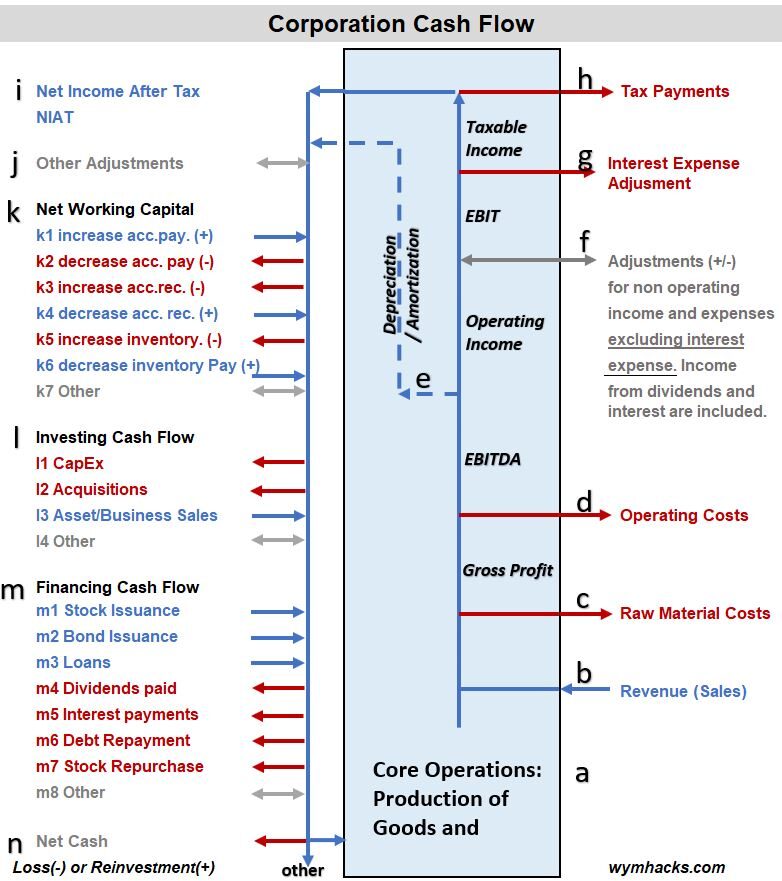

Corporate Cash Flow – General

A good place to start to understand stocks and bonds is to see how cash (money) flows in a corporation.

Refer to the cash flow diagram in Schematic 1 below.

It shows the inflows and outflows of cash from a typical public corporation (i.e. one that has shareholders).

The big blue box represents the core operations of a corporation and the red outbound arrows represent cash leaving the corporation (money spent).

The blue lines/arrows represent cash that the corporation possesses or is bringing in.

For completeness and just to remind the reader that there are numerous possible “ins and outs”, I’ve included grey lines for various cash flows that could be entering or exiting the corporation.

For now don’t try to figure exactly what all the items mean; just look at this drawing holistically and note the following:

- As long as we know all the inflows and outflows, we can do a “material balance” by adding all the inflows and subtracting all the outflows.

- We can account for all the numbers and gauge the health of the company.

- For example, is net cash (n) positive (good) or negative?

- All company stakeholders will be interested in this “balance of cash flows”.

- The managers will need to analyze the data and determine what the future steps need to be (to implement a strategy to correct losses and/or improve gains).

- The company owners and lenders will also be keenly interested in this information to determine their next investment moves.

- If the above can be done in a consistent and structured way, then people can follow standardized procedures to record, report, and analyze the data.

- That’s what the science of Accounting does.

Schematic 1 (Flow Schematic Showing Cash Flow in a Corporation)

Securities_Stocks

Stocks are initially issued by companies (in what is called a Primary Market) in order to raise cash for funding (called an Initial Public Offering or IPO).

Stocks represent a fractional ownership in the company (as a % of the total number of shares issued).

After the initial issue, stocks are bought and sold in a Secondary Market between investors.

The company DOES NOT directly gain or lose value with the rise and fall of the stock price.

The Secondary market is what the typical individual investor with his/her brokerage account is investing in

What do we mean by a fractional owner of a company (*)?

The box below in Schematic 2 shows a simplified summary of a company’s financial condition.

Assume it owns 100 million USD and it owes 60 million USD. We can translate the schematic into an equation: Assets = Liabilities + Equity.

This is called the Accounting Equation.

Schematic 2 (Simplified Corporate Balance Sheet Example)

The accounting equation defines Equity as what the company owns “minus” what the company owes.

A company shows this information in a financial statement called the Balance Sheet.

Stock owners have fractional ownership of the Equity (aka Owners Equity, or Shareholder Equity).

The total Equity in the example in Schematic 2 is 40 million USD.

Assuming there are 5 million shares of stock, the price per share is 40/5 = 8 $/share (this is called Book Value per Share).

Note that Book Value per Share will typically not equal the actual market price of the share i.e. Book Value and Market Value are not necessarily the same.

(*) If we bought some of this companies bonds, we would become fractional lenders of this company as well.

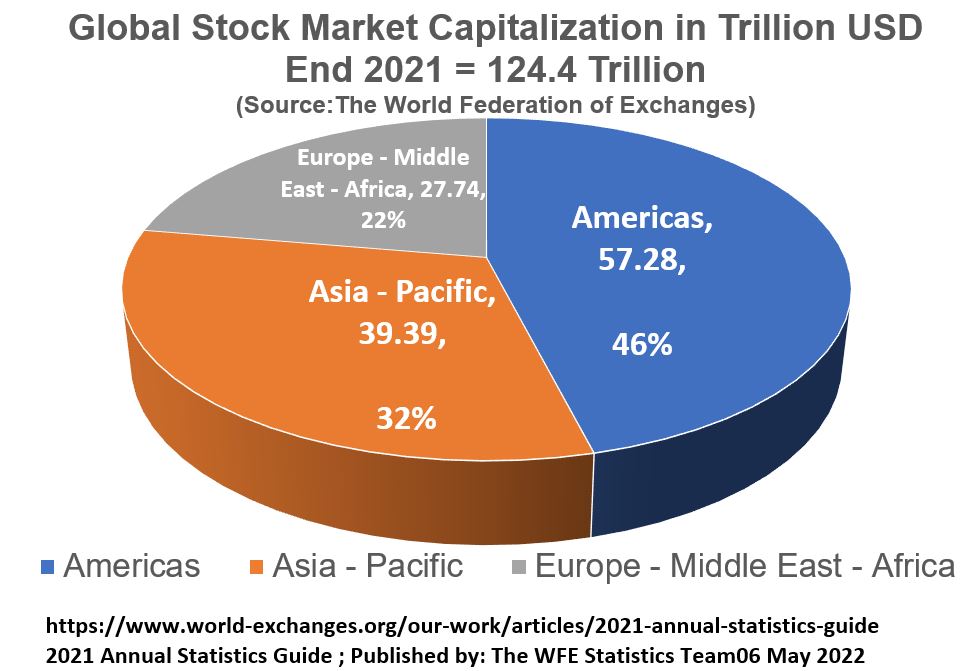

Global Stock Market Value

The total world stock market value at the end of 2021 was estimated to be 124.4 Trillion USD. See Schematic 1 below.

Note that the Americas component (91% of which are US stocks) is 46% of the total.

Many investors will include an international stock component to their asset allocation in order to participate in stock markets outside the USA.

Schematic 3 (2021 Global Stock Market Capitalization)

Stocks can be purchased through your brokerage account (or your company’s retirement account).

You can buy them individually or in pools or baskets (via mutual funds or ETFs).