Historical Stock Prices (Nominal Total Return Basis)

Lesson 1: U.S. Stocks go up over the long term

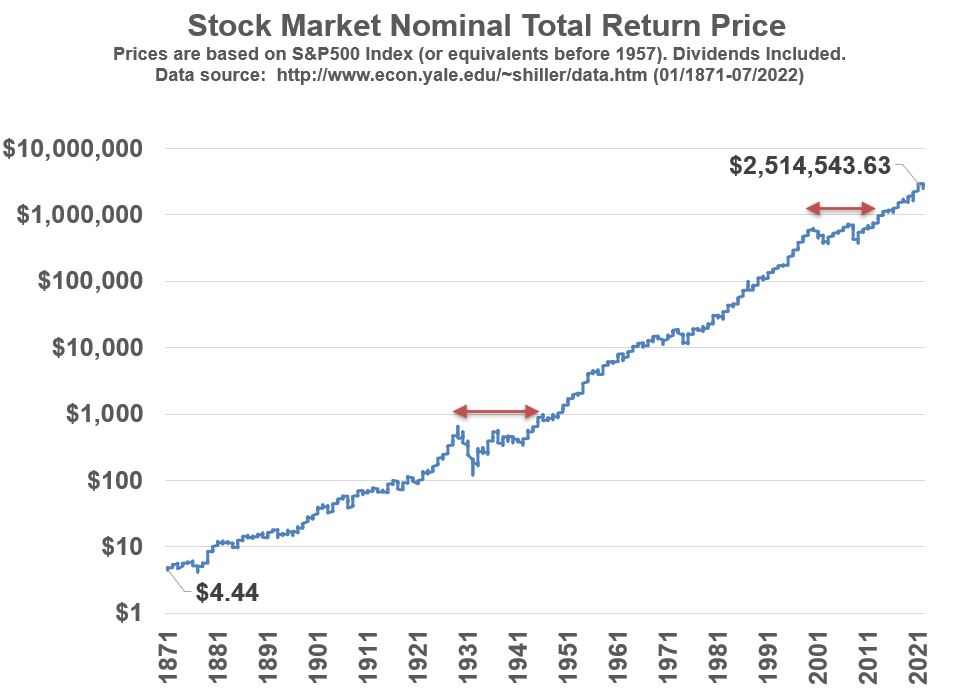

Take a look at Graph 1 below. U.S. Stocks grow in value over time. They do better over the long term than other investments. As long as we are able to innovate and develop new technologies and methods to improve our lives, I’d expect the long term trend to continue upwards.

Graph_1

From 1871 to 2022, stocks (as represented by the S&P 500 Index and pre-1957 indices used by Shiller) have returned an annual compounded growth rate of about 9% (Nominal).

If we adjust the values for the effects of inflation , we get a rate of return of about 6.9% (Real).

The graphs in this post show values on a Nominal basis, but be aware that inflation is a destroyer of purchasing power (i.e. money buys less over time) .

Knowing that stocks have a nice growth rate over a 151 year period might not make us feel that comfortable because, as you can see from the graph, there are long periods where the market does not grow (for example, see sections below the red arrows in Graph 1).

The following section explores historical price drops in the market and how long it took to recover from those price drops.

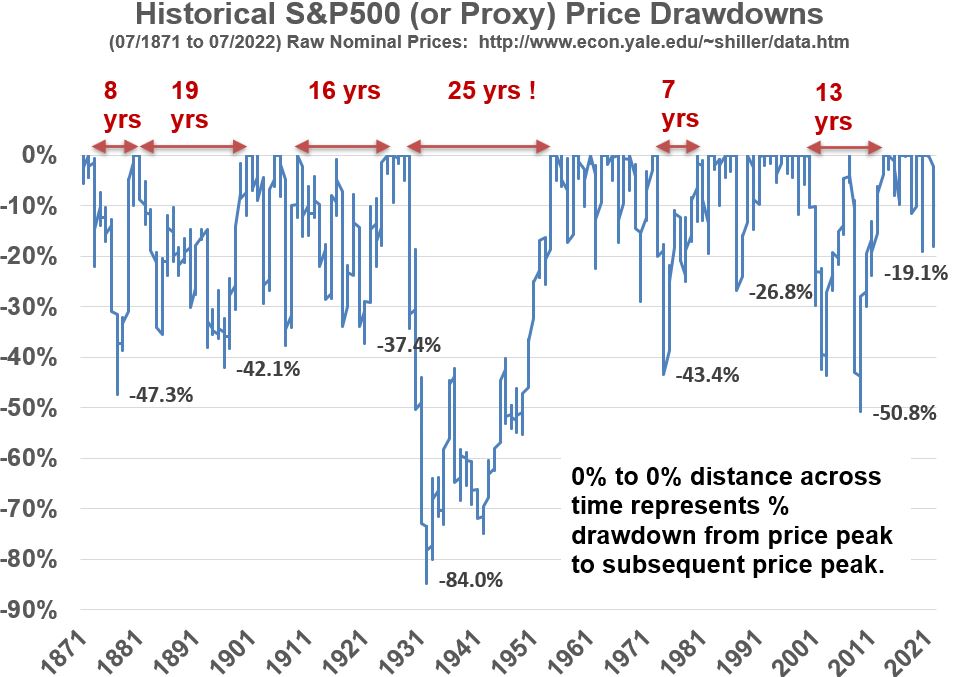

Historical Stock Price Drawdowns (Nominal Basis)

Lesson 2: U.S. Stock Market Prices can take a very long time to recover from losses.

In Graph 2 below, I’ve plotted the raw Nominal price (actual price; not adjusted for inflation or dividends) history in terms of drawdowns from price maximums (peaks).

Drawdowns help us view the magnitude and duration of price drops relative to historical peaks.

Each zero on the chart represents a price peak, and the gaps between the peaks show how long it took for the price to recover to its previous peak.

Note that the pricing is based on monthly averages.

Wow! Take a look at how deep and wide some of these stock declines have been!

Graph_2

Lets look at the big drawdown periods from Graph 2 above:

- The 2020 -19.1% drawdown represents the Covid Crash of 2020 but the market actually dropped about 34% from Feb 19, 2020 to March 23, 2020. It recovered quickly though; in about a month.

- Between the Dotcom (2000) crash and the Housing Bubble Crash (2008), the market took about 13 years to recover and experienced a price peak drawdown of -50.8%.

- It took 7 years to recover from the recession caused partly by the 1973 Oil Crisis.

- But, look at what happened after the 1929 U.S. Stock Market crash. The market lost about -84% from its peak and took 25 years to recover!

- Looking back to earlier periods you can see we have a few more long recovery period events.

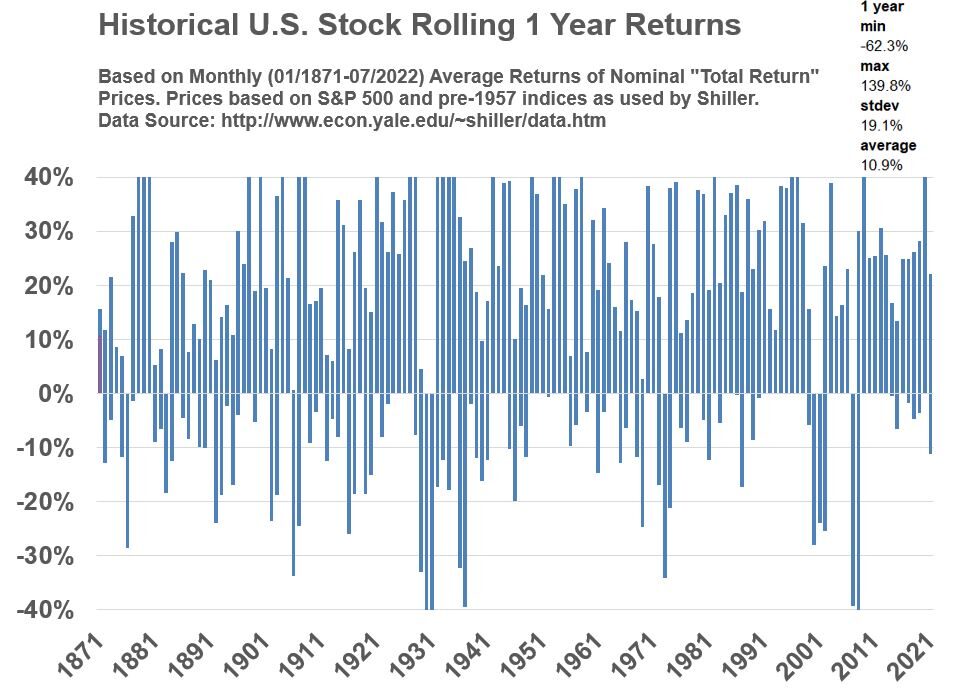

Historical Stock Price Returns (Nominal Rolling 1 Year Basis)

Graph 3 below shows how scattered (volatile) yearly returns are on a 1 year basis. I’ve fixed the Y axis range to +/- 40% but just be aware that about 5.2% of the data points are > 40% and about .6% of the data points are less than -40%.

Graph 3‘s statistical summary notes that the standard deviation is 19.1%.

This means that, if the data is normally distributed, we can expect about 68% of the returns to be within +/- 19% of the average.

However, be aware that this only holds true if the data is normally distributed.

More on this later when we discuss Graph 5 and the other histogram style distribution charts.

The standard deviation is larger than the average, so I would say that the movements are quite volatile.

In Graph 3 and later graphs, the term “rolling” means that the calculations are being done month by month where the data set is the same size but the oldest number drops off as the newest number is added.

Graph_3

Yearly returns are very volatile!

During the 1929 crash recession the minimum and maximum values were -62.3% and 139.8% respectively.

The values in Graph 3 represent rolling yearly averages (Jan to Jan, Feb to Feb, etc.).

Often you will see yearly return data expressed on a calendar year basis (approximately Jan to Jan on our graphs).

Does the yearly data look different if we look at non-calendar year periods? Check out Graph 4 to see the answer.

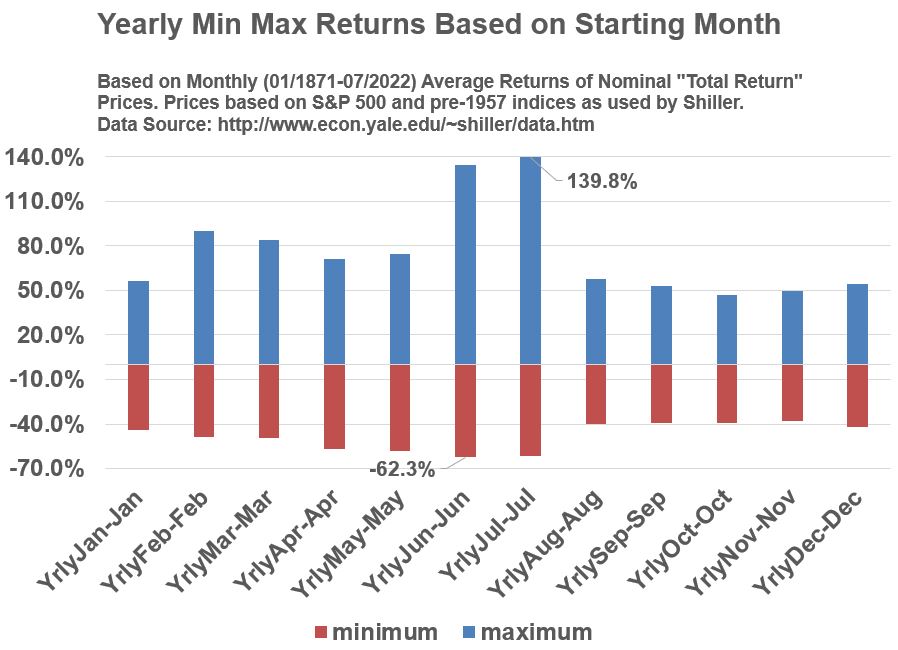

Various 12 Month Periods Compared

Graph 4 below plots the minimum and maximum values for all the potential 12 month periods. Interesting.

Clearly, there are other non-calendar year 12 month periods that are more volatile (sometimes much more volatile) than the Jan-Jan yearly periods.

So, just be aware of this the next time someone gives you a calendar year based statistic.

It might not be representative of some of the other 12 month periods.

Graph_4

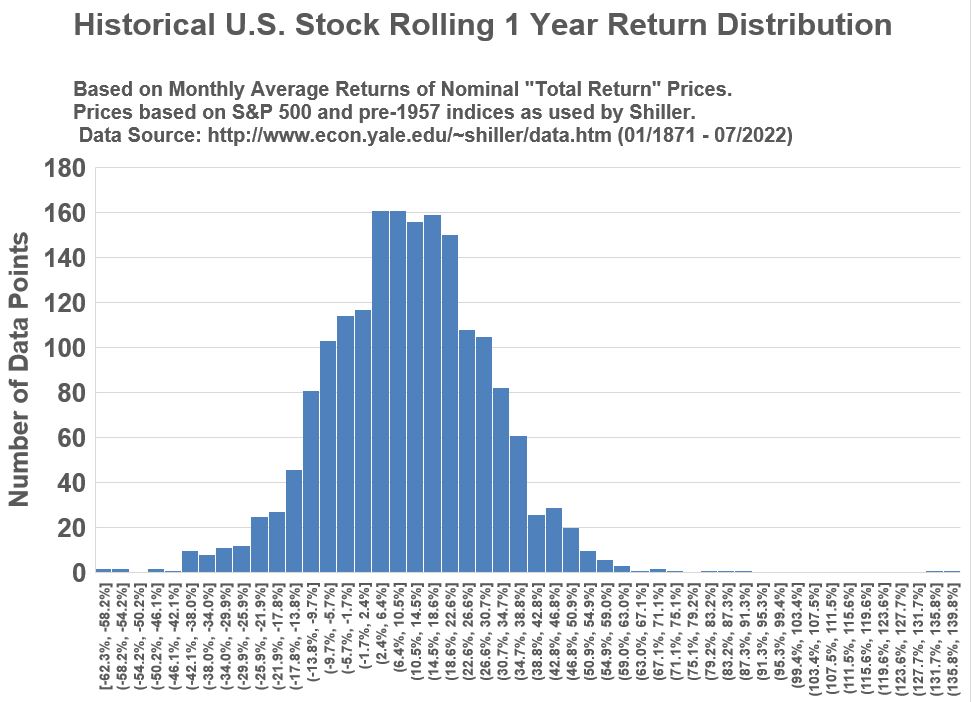

Histogram (Distribution Frequency) of Yearly Returns

Graph 5 below is a histogram that shows the frequency of the various yearly returns.

The shape is roughly “bell” shaped, meaning we can apply some general rules of thumb about the average and the spread from the average (the standard deviation).

Namely, we can apply the 68%/95%/99.7% rule : the average +/- 1 or 2 or 3 standard deviations will represent 68% or 95% or 99.7% of all the data points.

Graph_5

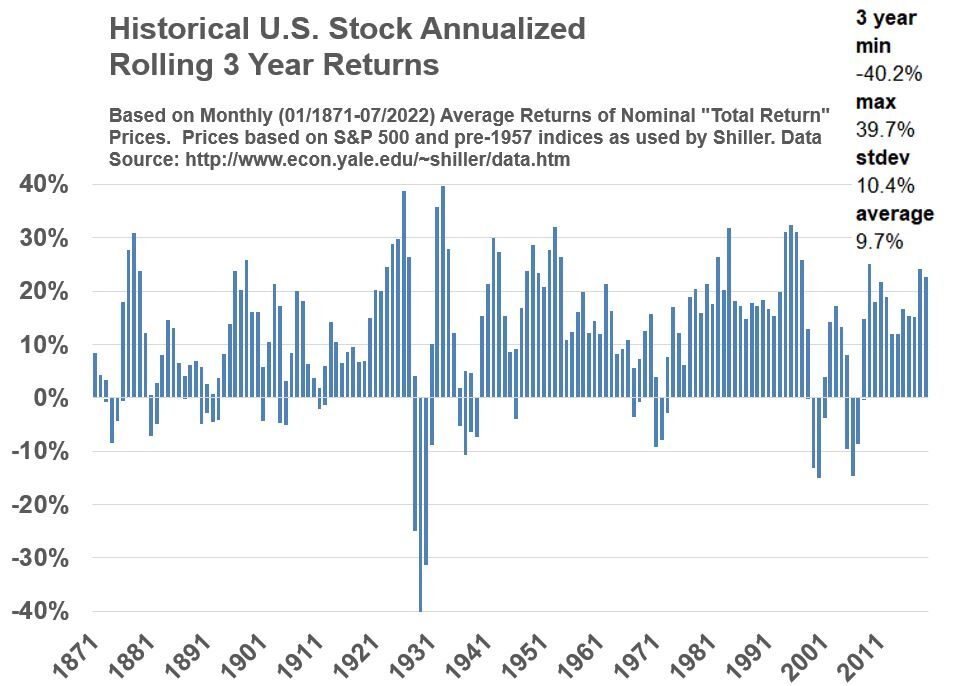

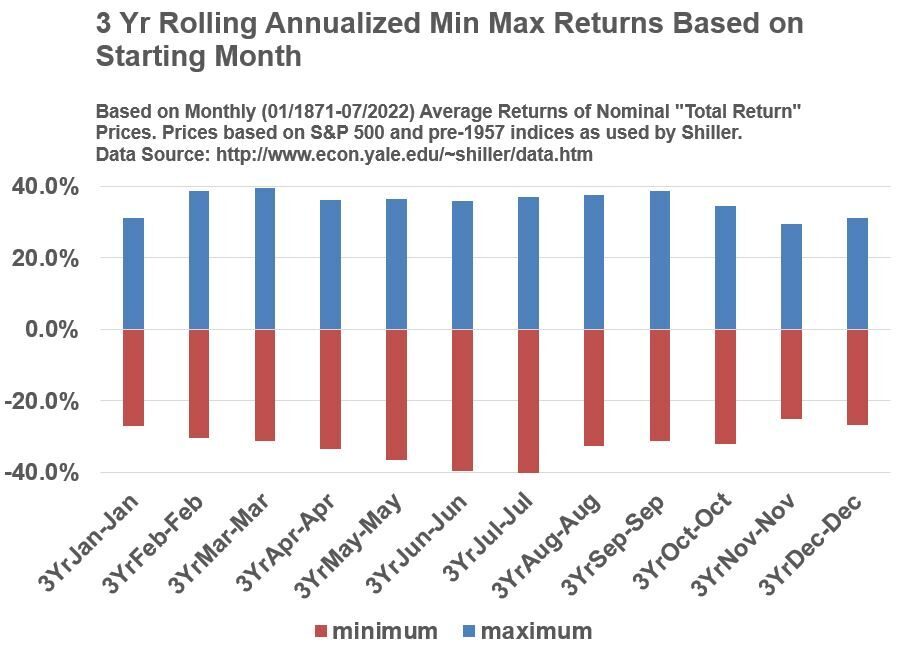

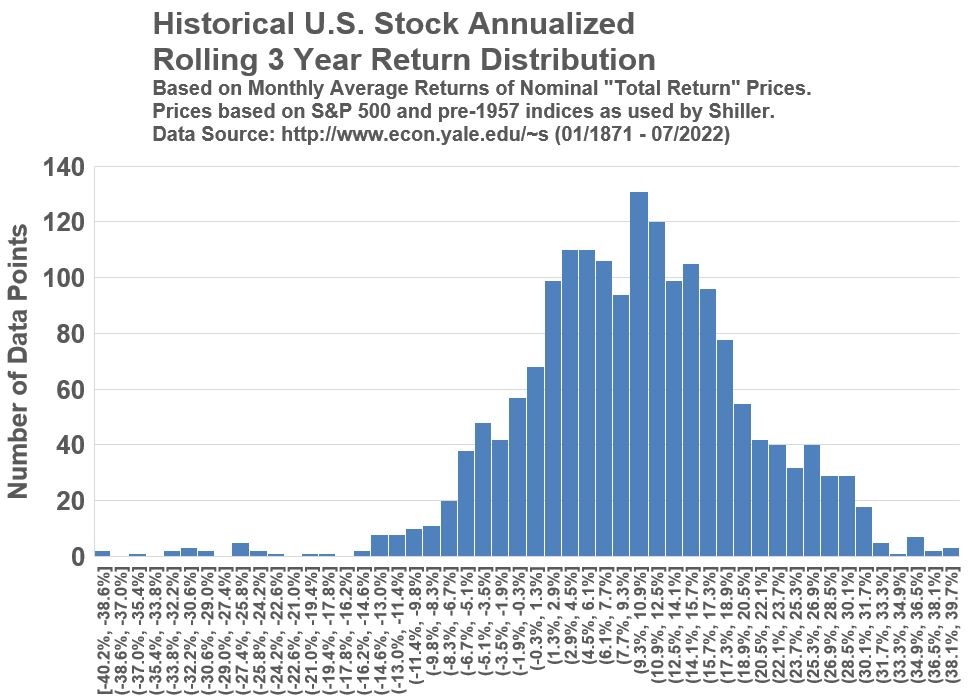

Historical Stock Price Returns (Nominal Annualized Rolling 3 Year Basis)

What happens to the data if we look at rolling 3 year periods and annualize the returns?

Graphs 6, 7 and 8 below are structured the same as Graphs 3, 4 and 5 above except that the annualization is computed across every three year period.

Be aware that the annualization is being computed using the CAGR (Compound Annual Growth Rate) formula.

The CAGR = (End Price/Start Price)(1/#of years) – 1.

When you compare the shapes of Graphs 6,7,8 with Graphs 3,4,5, you’ll see that the data becomes less scattered and the distribution ranges lessen.

Graph_6

You can see that Graph 6 has been smoothed out quite a bit compared to Graph 3.

The three year period shows less volatility (standard deviation of 10.4% versus 19.1%).

Graph 7 below shows that the calendar and non-calendar years are looking more alike compared to Graph 4.

Graph_7

Both Graph 8 below and Graph 5 show a roughly Normal Distribution although Graph 8 looks like it has two peak areas developing.

Notice the range in Graph 8 is about -40.2% to 39.7% whereas the range in Graph 5 is -62.3% to 139.8%.

Graph_8

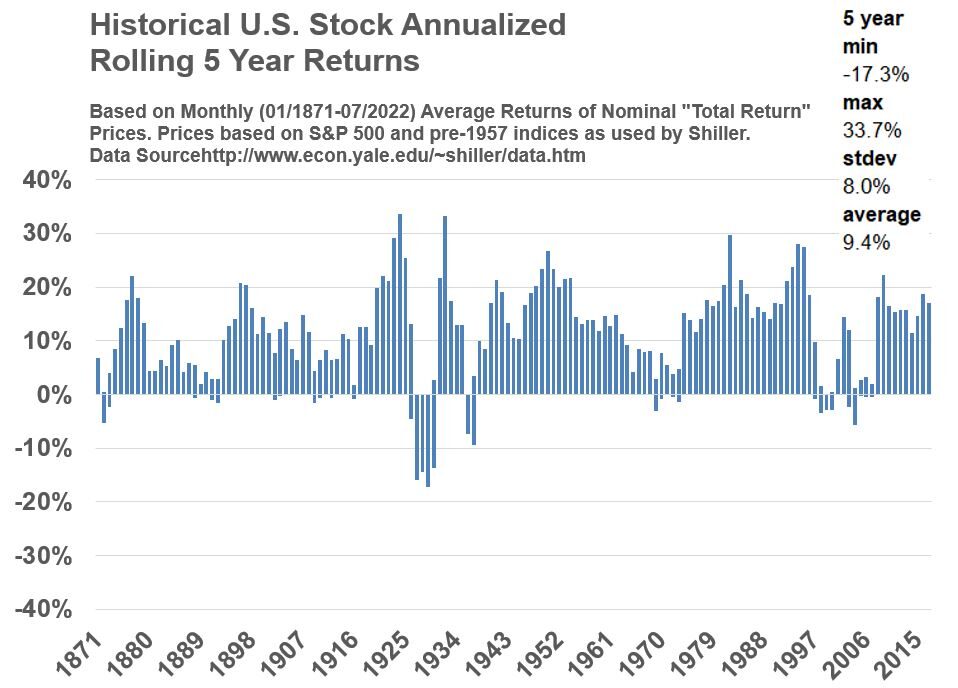

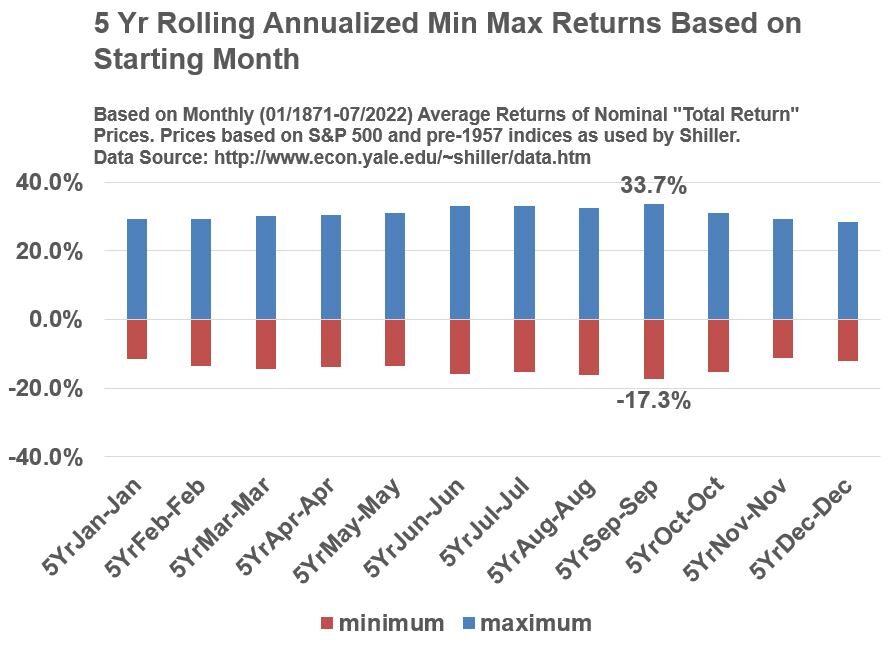

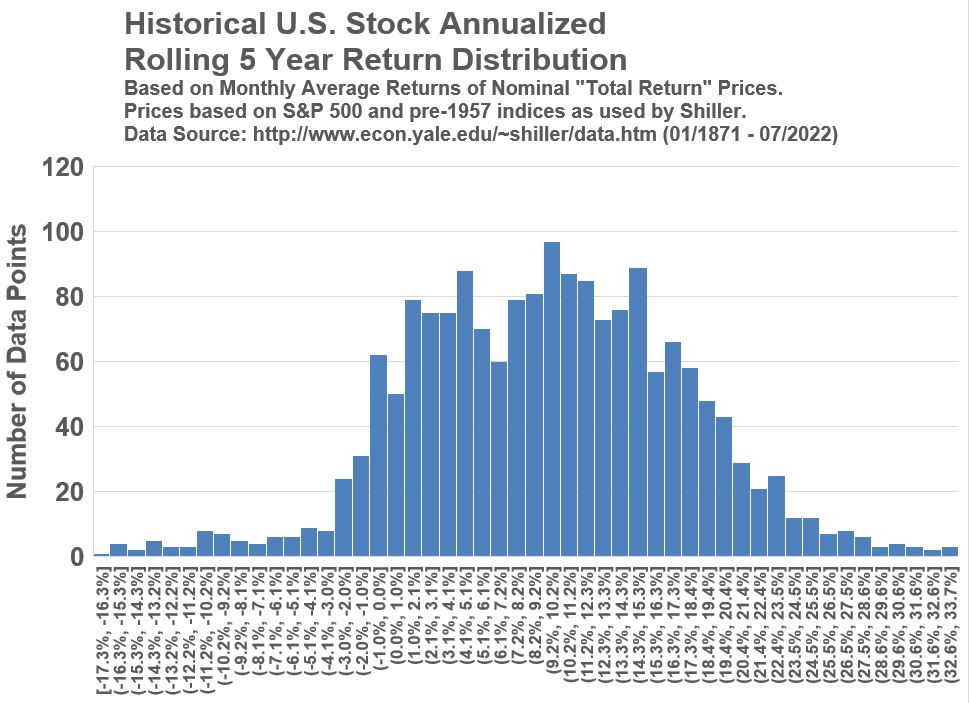

Historical Stock Price Returns (Nominal Annualized Rolling 5 Year Basis)

What do you think happens if we extend the rolling period to 5 years?

Scroll down through Graphs 9,10, and 11 to confirm what you are probably guessing.

Graph_9

Graph_10

Graph_11

Comparing the 5 year period Graphs 9,10,11 against the 3 year period Graphs 6,7,8 shows that scatter of the data continues to narrow.

The average returns drop a little but the standard deviations (the volatility) drop a lot.

Through 1 to 3 to 5 year annualized return periods,

- the average return has dropped from 10.9% to 9.7% to 9.4% but

- the standard deviation has dropped from 19.1% to 10.4% to 8%.

Key Observations/Learnings

- In the long run, stocks provide the most competitive returns against other assets.

- I didn’t prove it in this post since you’re better off studying this in the works of Jeremy J. Siegel, John C. Bogle , Charles D. Ellis, and Warren Buffet (among others).

- In the long run (using the 150+ year Shiller data set), there can be very long periods before stocks recover from losses.

- Stock returns are very volatile (to the positive and negative side) in the short term.

- Also very few days (which are probably impossible to always predict) contribute disproportionately to the market upside movements. See this post for more on this.

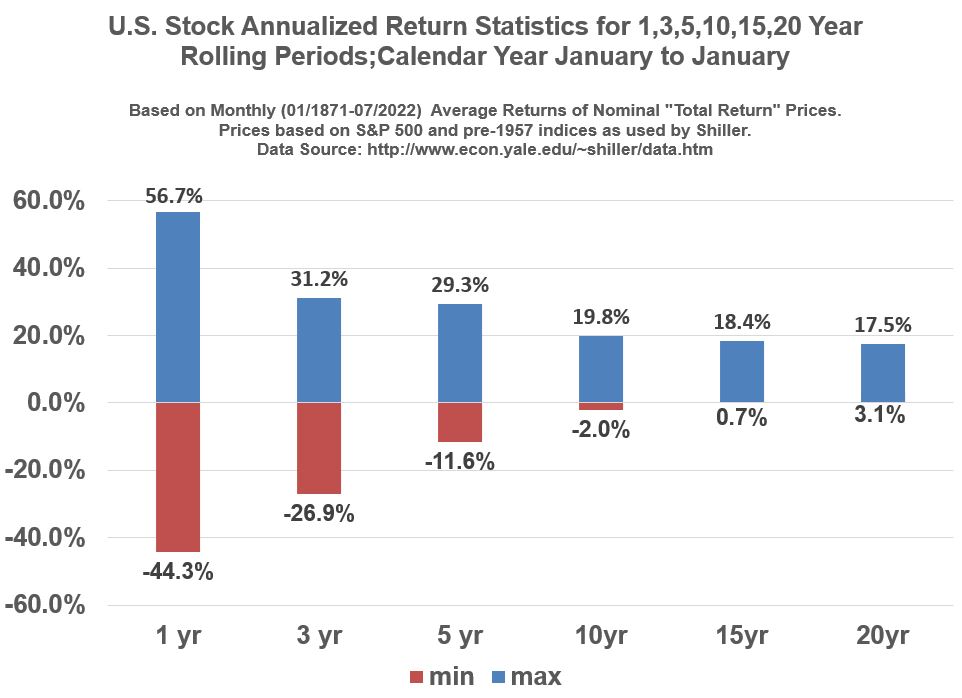

- See Graph 12 below.

- Over longer durations, the range of annualized returns narrow, with a tilt towards fewer negative returns.

- For example, from Graph 12, annualized calendar year returns over rolling 10 year periods show a maximum loss of about -2%.

- For 15 and 20 year rolling periods, there are no negative annualized returns.

- Maybe I tricked you a little bit with the previous bullet.

- Graph 12 is only true for the Jan to Jan periods.

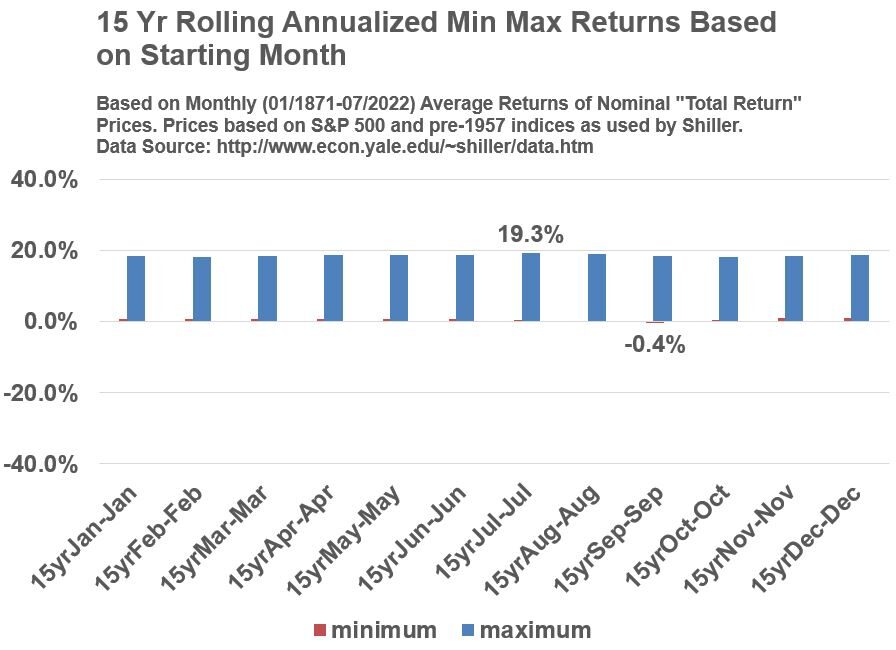

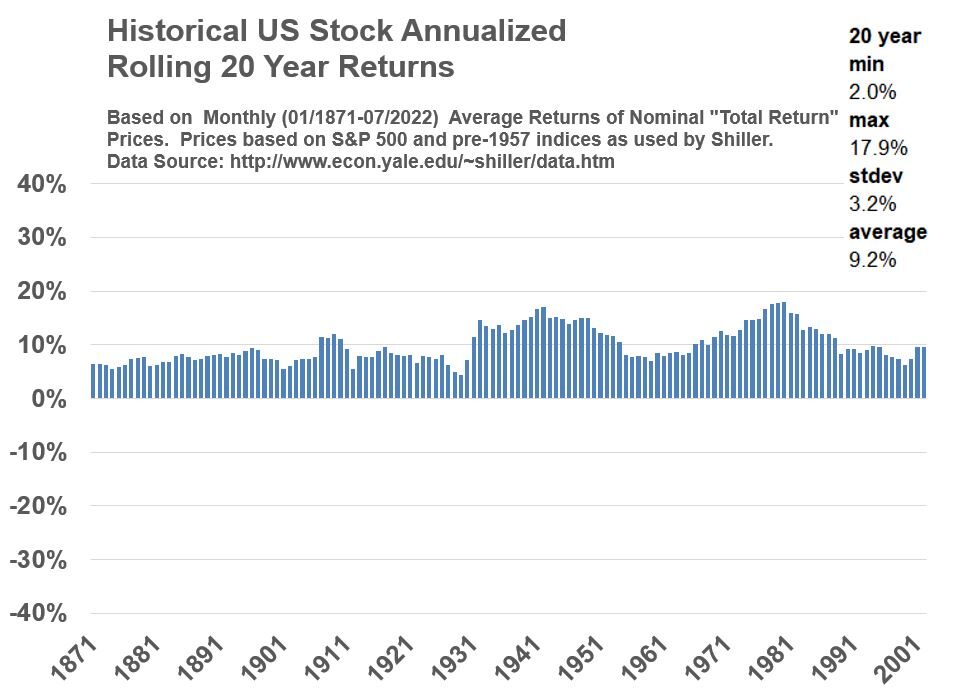

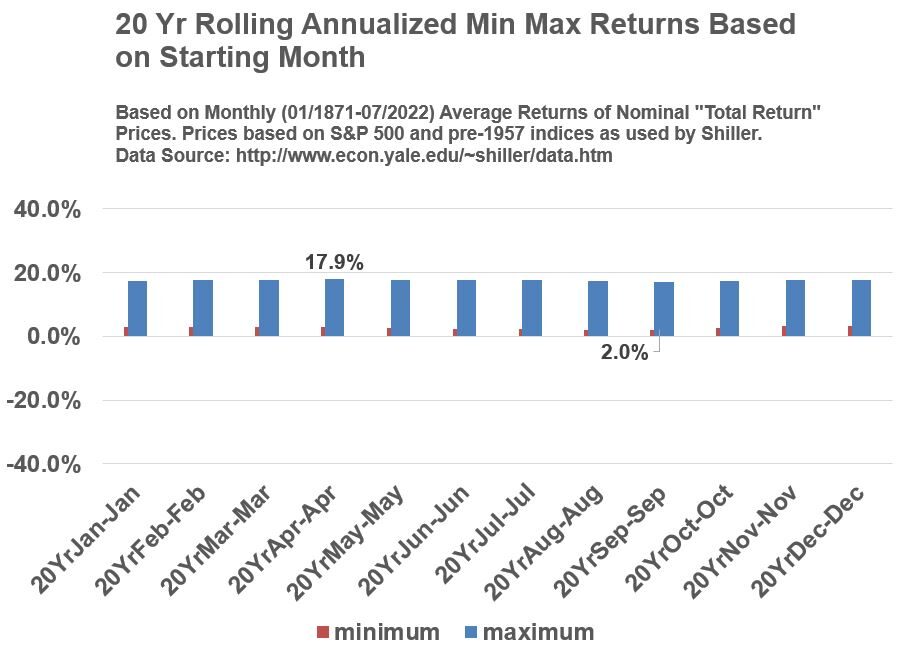

- If we look at all rolling periods in Graphs 13,16, and 19 we see that the max losses are actually -4%, -.4%, and +2% for all rolling 10,15, and 20 year periods.

- My advice to you is, if someone states performance numbers, you should ask as many context related questions as you can think of..like,

- How was the data calculated?

- What is the source date?

- Are the performance values based on calendar year ?

- Are there worse performing non-calendar year periods?

- Is the data expressed in Nominal terms or Real terms? etc.

Graph_12

Appendix 3

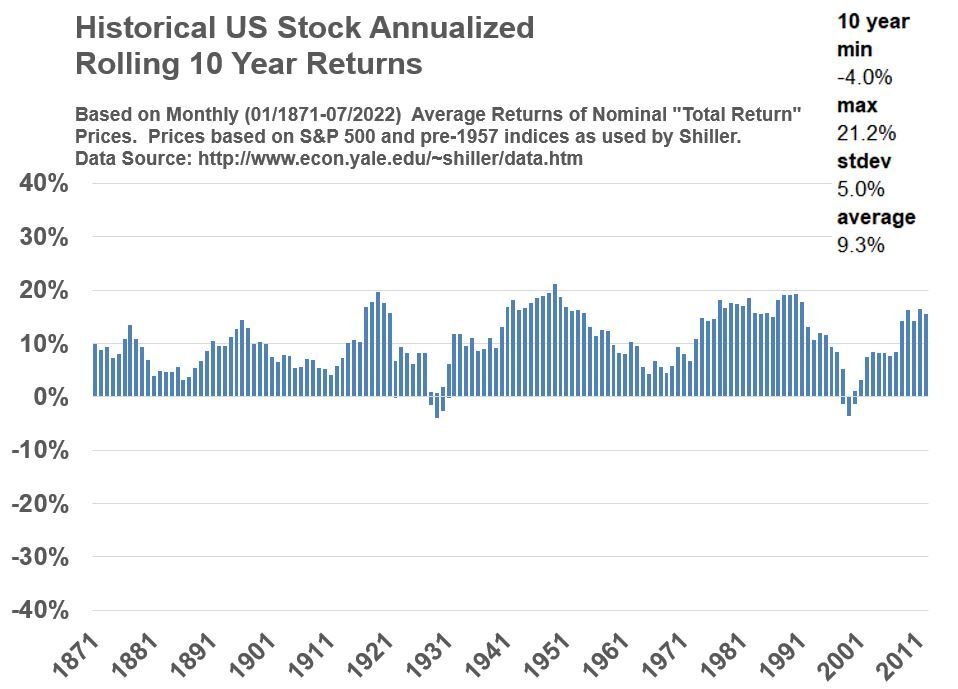

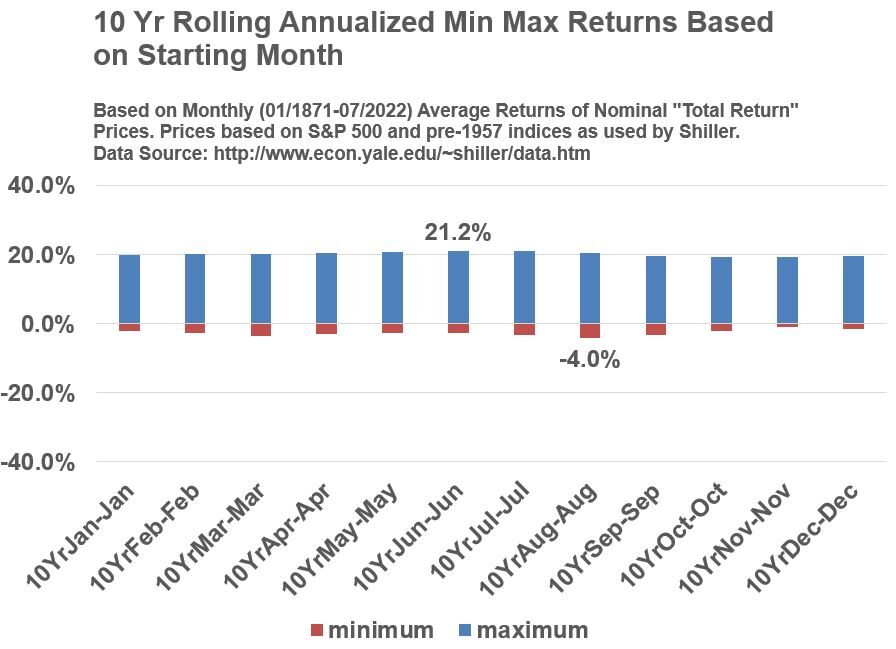

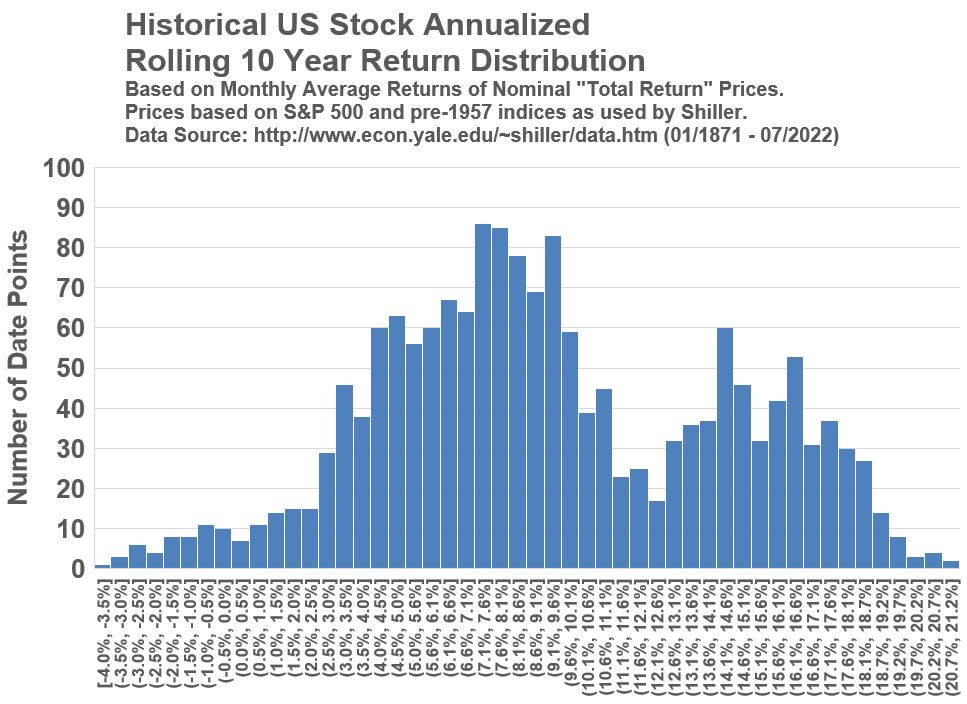

Historical Stock Price Returns (Nominal Annualized Rolling 10 Year Basis)

Graph_13

Graph_14

Graph_15

Appendix 4

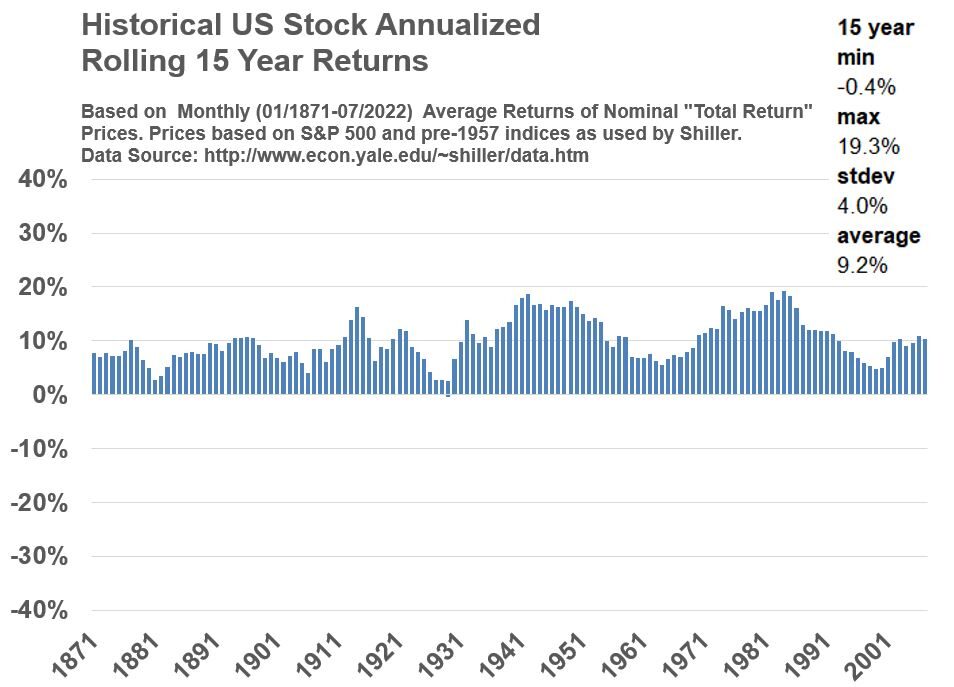

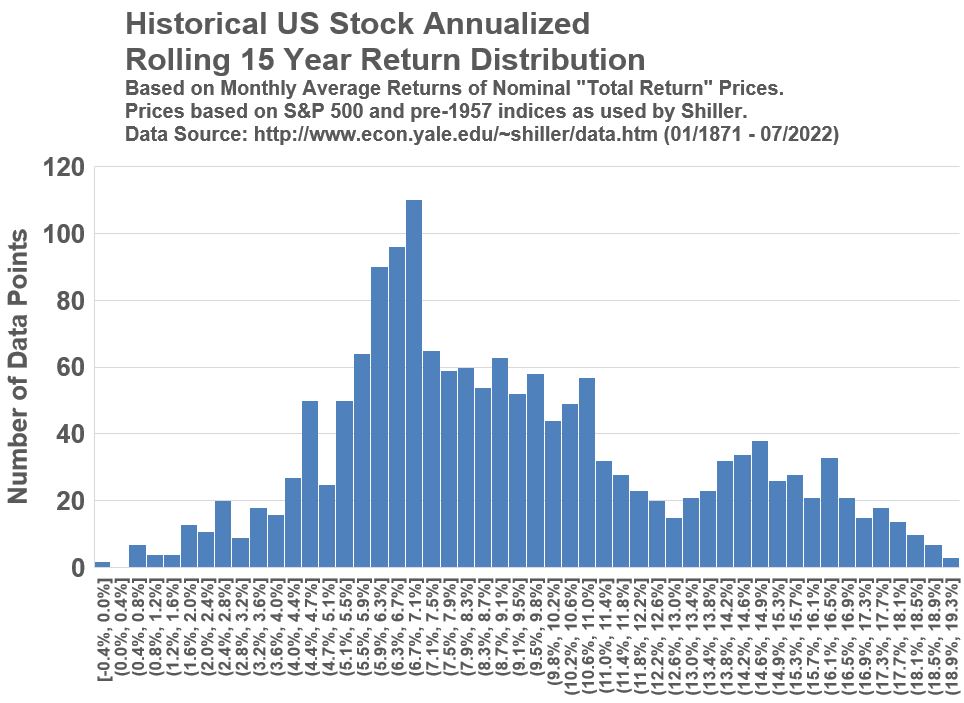

Historical Stock Price Returns (Nominal Annualized Rolling 15 Year Basis)

Graph_16

Graph_17

Graph_18

Appendix 5

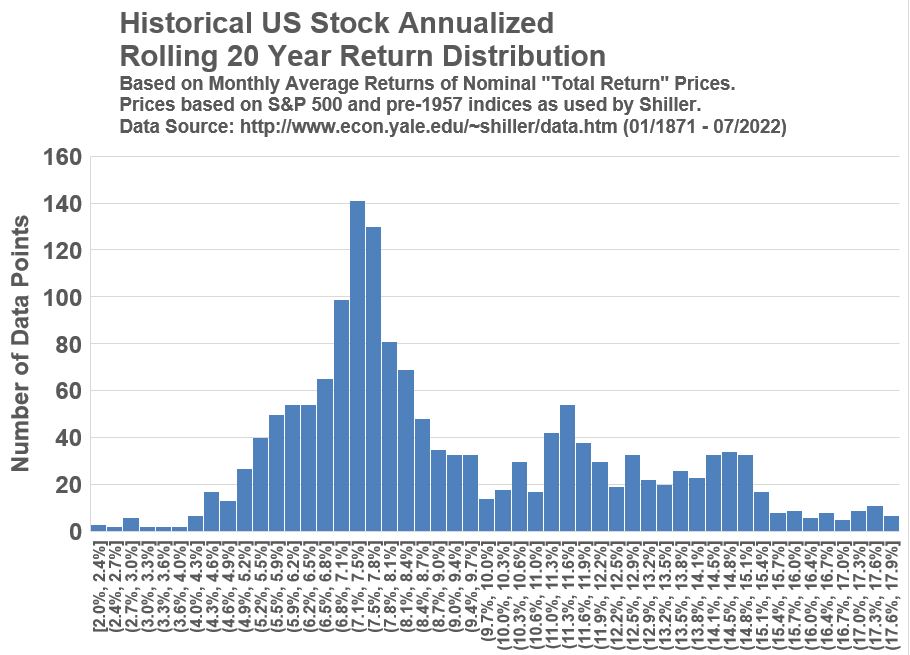

Historical Stock Price Returns (Nominal Annualized Rolling 20 Year Basis)

Graph_19

Graph_20

Graph_21