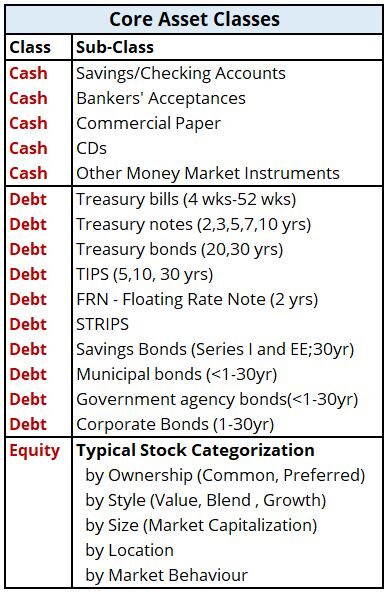

Investment Asset Classes

We can somewhat arbitrarily create four categories to describe the investment universe:

- Cash and Cash Equivalents: e.g. hard cash (bills and coins),savings accounts and money market funds.

- Debt instruments: e.g. bonds where you basically own a loan.

- Equity or stocks: where you own part of a corporation.

- Other is basically everything else. You will often hear the term Alternative Investments to describe this category. Alternatives examples would be real estate or commodities.

Graphic 1 – Investment Asset Classes

Cash is the least risky asset and by risky we mean probability of losing money on the investment.

According to the Securities and Exchange Commission (SEC)

“..risk refers to the degree of uncertainty and/or potential financial loss inherent in an investment decision. In general, as investment risks rise, investors seek higher returns to compensate themselves for taking such risks.”

Equities or stocks are riskier than Cash and Debt investments.

See this great Forbes article on the financial definition of risk: Forbes article on Risk and Volatility.

Let’s call Cash, Debt, and Equity , the Core Asset Classes (or Core Assets for short).

In addition to being able to singularly invest in each of the Core Assets, we are also able to invest in combinations of these assets through investments “pools” called Mutual Funds and Exchange Traded Funds (and others).

The “Alternatives Class” is the catch-all repository for other investment options like real estate, commodities (steel and precious metals for example) , derivatives and others. Some of these Assets can be extremely risky.

Let’s first dig deeper into some of the investment options in the Core Asset Classes

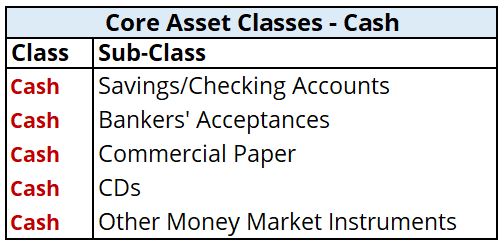

Core Assets – Cash and Equivalents

Most of us are familiar with this category.

Cash and its Equivalents is the physical cash or those financial instruments that can be converted to cash quickly.

Table 2 – Cash Types

See finra.org (bank products) for more information on these types of accounts.

Typical “Cash and Cash Equivalent” investments are:

- Savings Accounts (Interest Income producing accounts)

- Money Market Accounts (Similar to Savings Accounts)

- Certificates of Deposit (Income producing time deposits)

These types of investments are liquid by definition (i.e. finances are easily turned back to cash).

They are often federally insured as well.

Short term duration debt instruments are also considered Cash Equivalents (See Finra.org or Investopedia) .

Examples of these are:

- Bankers’ Acceptances,

- Corporate Commercial Paper,

- Short Duration government bonds and municipal bonds (see next section)

Investment instruments for Cash Equivalents are often fixed income Mutual Funds called Money Market Funds.

Mutual Funds essentially pool (i.e. gather or collect or combine) various investments together that meet some common theme or strategy.

Core Assets – Government Debt

Debt is typically in the form of a bond.

Finra defines a bond as

“… a loan an investor makes to a corporation, government, federal agency or other organization in exchange for interest payments over a specified term plus repayment of principal at the bond’s maturity date.”

The time from original issue to maturity date is called the duration.

Table 3 – Debt Types

TreasuryDirect.gov is your one-stop-shop for all things government bonds (not including municipal bonds, though).

TreasuryDirect provides the key characteristics of available bonds and allows you to directly purchase Treasuries, TIPS (see below), FRNs (see below), and Savings Bonds.

You can also purchase through a bank or broker (directly or via various investment instruments like Mutual Funds and Exchange Traded Funds (ETFs) ).

Finra is another good source for general bond information.

Government Bond Types

Here is a descriptive list of government bond types starting with the shortest duration bonds,

- Treasury Bills (4 wk to 52 wk duration)

- Treasury_Notes (2,3,5,7,10 year durations)

- Treasury Bonds (20,30 year durations)

- TIPS – Treasury Inflation Protected Securities (5,10,30 year durations)

- Floating Rate Notes (FRNs) (2 year duration)

- STRIPS – Separate Trading of Registered Interest and Principal of Securities.

- The principal component and the interest components are separated and made into standalone investments.

- Savings Bonds (30 year duration).

- There are two types of Savings Bonds; EE and I bonds.

- According to Treasury Direct, “I Bonds protect against inflation. They earn both a fixed rate of interest and a rate based on inflation.”

- Municipal bonds are issued by cities, governments, and municipalities to primarily fund infrastructure projects.

- Many of them are exempt from federal taxes (and some are exempt from state taxes as well).

- Government Agency Bonds – Bonds (e.g. Mortgage Backed Securities) issued by Federal Government Agencies like Ginnie Mae and Government Sponsored Enterprises (GSE) like Fannie Mae ,Freddie Mac, and Farmer Mac.

- Ginnie Mae: Government National Mortgage Association

- Fannie Mae: Federal National Mortgage Association

- Freddie Mac: Federal Home Loan Mortgage

- Farmer Mac: Federal Agricultural Mortgage Corporation

Core Assets – Corporate Debt

The SEC website Investor.Gov and Finra provide excellent introductory material on Corporate Bonds.

My advice is; read all the corporate bond articles on the Investor.Gov site and you will be headed in the right direction.

Corporate Bonds just like Government Bonds are debt obligations that pay periodic interest (typically) and pay back the principal (amount borrowed) at some specified time.

You can buy corporate bonds via banks or brokerages.

- For example your Schwab or Fidelity brokerage account will allow you to buy bonds in both the primary market (original issuance) or secondary market (where bonds are being re- bought and re-sold).

- You can also buy bonds via Mutual Funds or Exchange Traded Funds (which are pooled investments using a certain investment category or theme.)

Some key attributes of Corporate Bonds are:

- Unlike U.S. Government bonds, the credit quality (i.e. the ability of the company to pay interest and principal back) of Corporate Bonds covers a wide range.

- Bonds are categorized as “investment grade” or “non investment grade” according to assessments done by one or more credit rating agencies.

- The three major credit rating agencies (they are U.S. companies) are Moody’s, Standard & Poor’s, and Fitch.

- See these links for more information: SEC bulletin on Credit Rating and Investopedia on Credit Rating Agencies.

- Corporate Bond holders generally have priority over stock holders if the company has financial difficulties.

- Corporate Bond durations can be categorized as :

- short duration (<3 years),

- Medium Duration (4-10 years), and

- Long Duration (>10 years).

- Corporate_Bonds can pay periodic fixed interest or periodic floating interest(where interest is adjusted relative to a benchmark).

- Zero Coupon Bonds do not pay out interest during the duration of the bond but include the accrued interest at maturity (i.e. principal plus interest is returned).

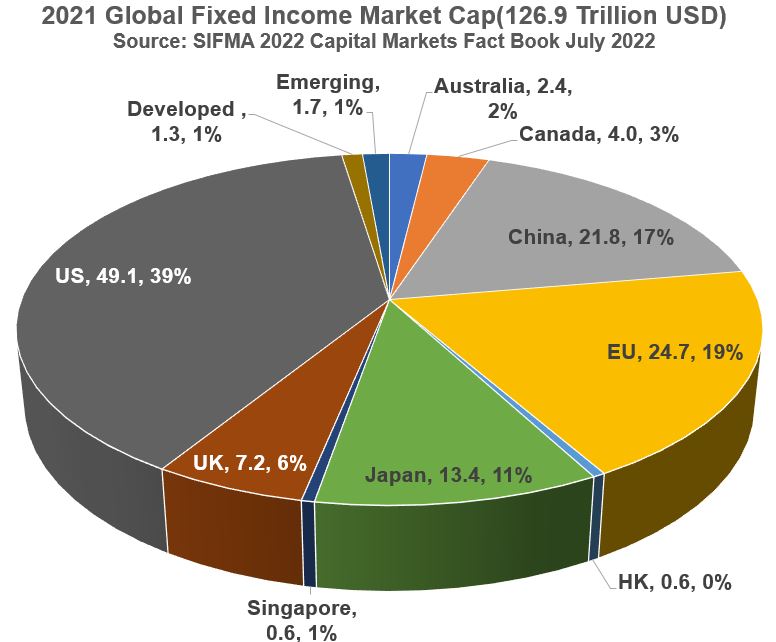

Core Assets – Bond Market Size

According to the SIFMA Capital Markets Factbook 2022, the size of the fixed income market is enormous:

- World market capitalization: 126.9 Trillion USD (i.e. 126,865.5 Billion USD).

- USA market capitalization: 49 Trillion USD (38.6% of the World capitalization)

Take note that about 79 Trillion USD of bonds are internationally based.

Graphic 2 – Market Cap. of World Fixed Income

Core Assets – Equity

Read the Finra.org or SEC (Investor.gov) sections on stocks.

Equities or equity refer/s to stocks which represent fractional ownership in publicly traded companies.

The value of the stock will fluctuate with investor demand. Some stocks return a portion of their earnings back to shareholders via periodic dividend payments.

Dividend paying stocks tend to be more mature, established companies that are no longer in a high earnings (profit) growth mode.

Etymology of the Word “Equity”

A reasonable explanation for the origin of the term “equity” can be found here (see the Kevin Beach section).

To paraphrase this source: Historically, English Common Law was often too harsh and required interpretation and judgment for the sake of fairness or “equity”.

Over many years the concepts of legal versus beneficial ownership were established.

In the original corporations of the 17th century, managers were the trustees (legal owners) of the companies and issued certificates of ownership to the investors (beneficiaries).

These investors were described as owning “equities” in the company, meaning they had fair and equitable rights as shareholders.

Today, shareholder rights would include fractional ownership, ownership transfer, voting, suing, inspecting corporate documents, and owning dividends (see this Investopedia link for more information on Shareholder rights).

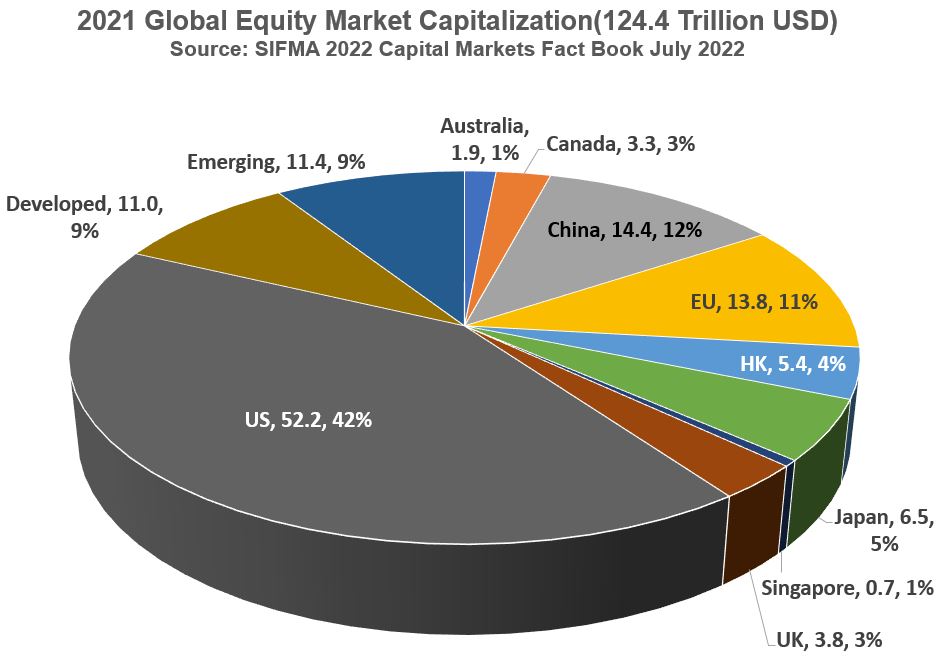

Equity Market Size

Like the global fixed income market, the global stock market is huge.

According to the SIFMA Capital Markets Factbook 2022:

- World stock market capitalization = 124.4 Trillion USD (similar to the 126.9 Trillion for the fixed income market).

- USA stock market capitalization = 52.2 Trillion USD = 42% of Total (compared to 49 Trillion = 38.6% of Total for the fixed income market).

Graphic 3 – Market Cap. of World Equities

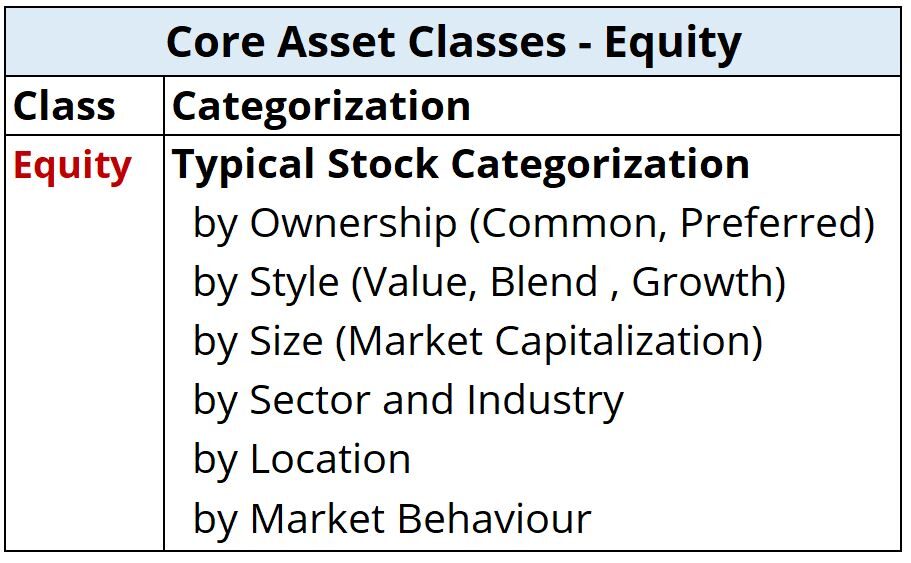

Equity Characteristics

Stocks can be described using combinations of category descriptions as described in the following sections.

Table 4 – Equity (Stocks)

Equity Characteristics – Ownership

The vast majority of stocks are Common Stocks.

- The price fluctuates and is based on buyer demand (it is not capped or limited).

- Common Stocks can pay dividends but the dividends can be adjusted up or down or ever eliminated (they are not guaranteed).

Preferred Stock usually guarantees its dividend payments.

- The dividends are fixed and are paid out before dividends on common stock.

- Price movement is also limited with Preferred Stocks.

If the company fails, the order of obligations to owners is:

- (1) Bond holders

- (2) Preferred Shareholders

- (3) Common Shareholders.

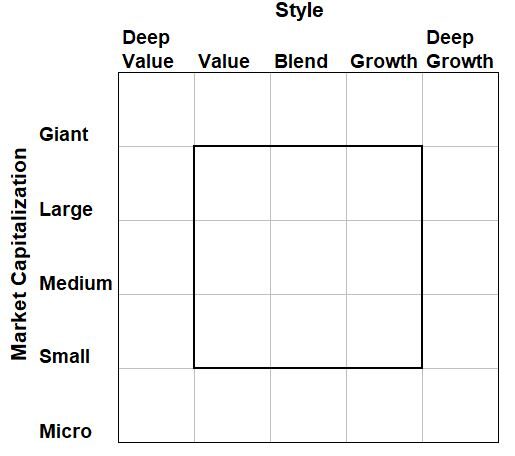

Equity Characteristics – Style and Size

Two commonly used characteristics of stocks are

- Market capitalization (number of shares outstanding x share price)

- Growth vs Value financial performance often described as the “style” of the company

Morningstar provides one of the more useful general investment information websites.

They also invented the 9 and 25 category style box shown below in Graphic 4.

The style box concept is now used almost universally to describe stocks and investment funds like Mutual Funds and Exchange Traded Funds (ETFs).

The Morningstar style box allows for 25 combinations of size and style.

- The originally constructed box had 9 categories but has recently been expanded to 25 boxes to allow for more granular representation of Mutual Funds and ETFs.

- From the Morningstar web site, if you choose a certain ETF or Mutual Fund, you can go to the “Portfolio” section to see its style box.

Graphic 4 – Morningstar Style Box

Equity Characteristics – More on Size

Morningstar provides a convenient definition for Large, Mid, and Small market cap (capitalization) stocks.

These definitions will not always be 100% consistent with firms who have created and marketed their own size definitions (e.g. S&P, FTSE Russell, etc.).

If you are trying to devise an investment mix based on market capitalization, consider sticking with a consistent set of definitions from the same firm to avoid too much overlap or redundancy.

Morningstar Definitions for Stock Size

The Morningstar definitions for stock size are based on a cumulative capitalization scale of all stocks in a particular country or geographic area (style zone).

- Giant-Cap Stocks (Top 40% of the cumulative market capitalization)

- Large-Cap Stocks (Top 70% of the cumulative market capitalization).

- Mid-Cap (70%-90% of the cumulative market capitalization).

- Small-Cap (90%-97% of the cumulative market capitalization)

- Micro-Cap (97%-100% of the cumulative market capitalization)

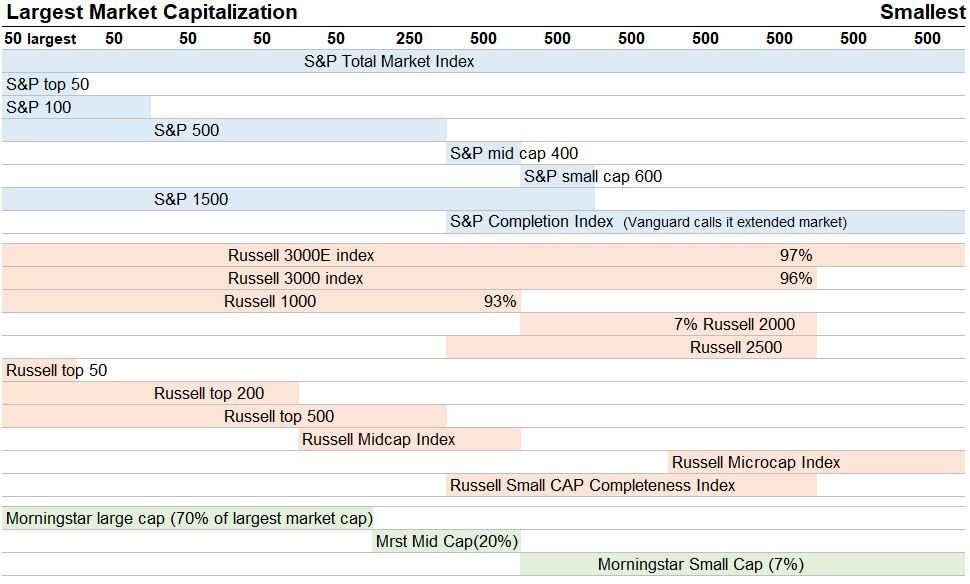

Other Stock Size Definitions

Firms like S&P Global , FTSE-Russell, and MSCI define market capitalization by number of stocks. For example:

- S&P top 50 US stocks (largest 50) are Mega-Cap stocks (Morningstar would call these Giant-Cap stocks although definitions would not exactly match).

- S&P 500 index, S&P Mid-Cap 400, and S&P Small-Cap 600 represent the largest 1500 US stocks.

- The Russell 1000 index represents the top 1000 largest cap US companies (Large-Cap + Mid-Cap) and the Russell 2000 represents the next 2000 largest cap companies (Small-Cap).

Refer to Table 5 below for examples of how S&P (S&P Global) and Russell (FTSE-Russell) define some of their market capitalization indices.

Table 5 – Example of Market Capitalization Index Definitions from S&P, Russell, and Morningstar for US Stocks.

As I noted before , if you are trying to devise an investment mix based on market capitalization, consider sticking with a consistent set of definitions from the same firm to avoid too much overlap or redundancy.

Equity Characteristics – Industries and Sectors

There is more than one industry classification system out there (of course). Some of the major ones are:

- Standard Industrial Classification (SIC) system developed by the US government in 1937. See this Investopedia article also.

- In 1997, SIC codes were further expanded to NAICS (North American Industrial Classification System)

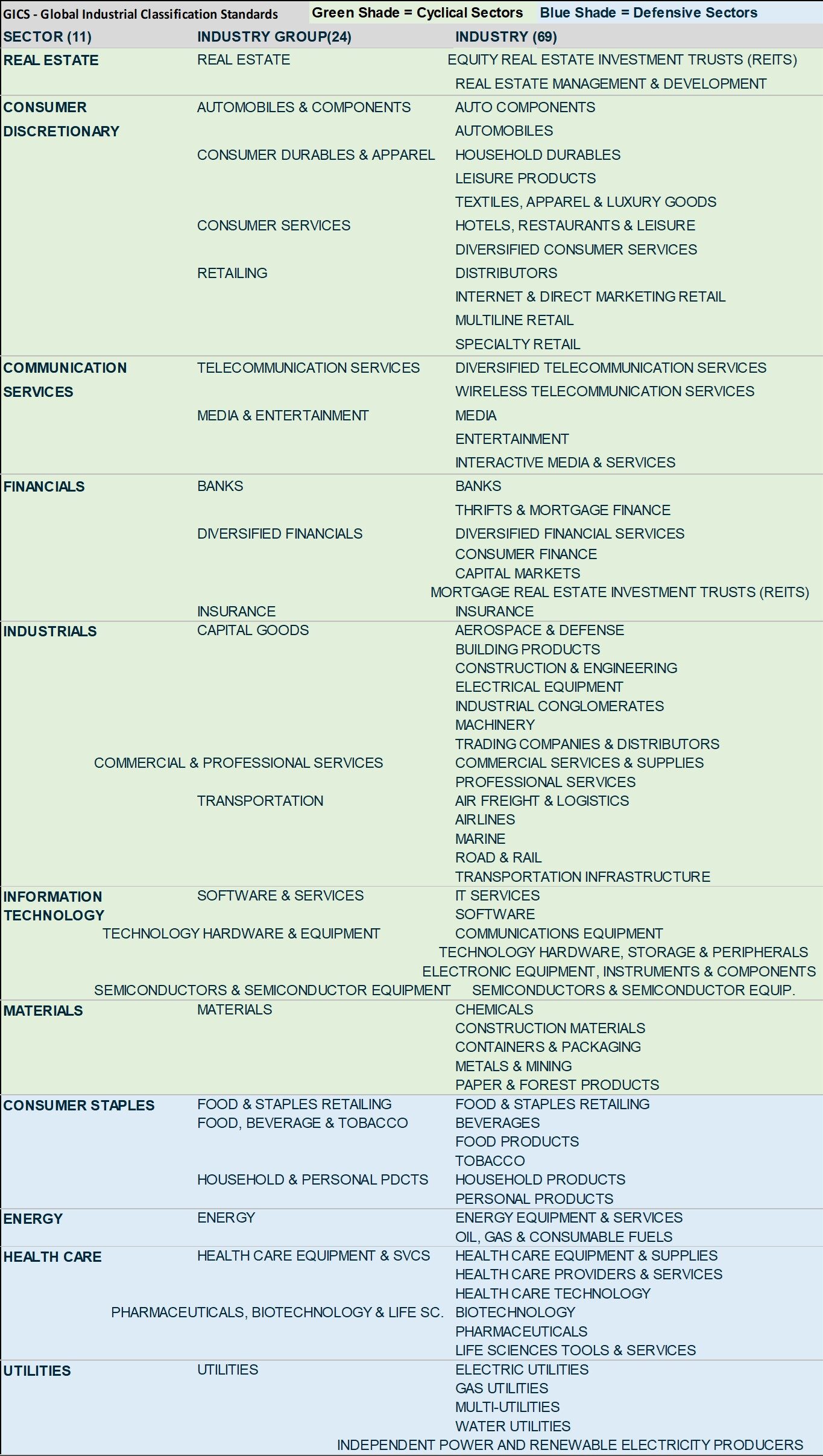

- In 1999, the investment research firm MSCI (Morgan Stanley Capital International) and S&P (Standard and Poor’s ; known as S&P Global today) developed a Global Industry Classification Standard (GICS) which is broadly used today.

- The GICS categorize the stock universe into 11 sectors, which are divided into 24 industry groups (which ,as of Oct 2022, are divided into 69 industries and 158 sub-industries).

- The FTSE-Russell developed an Industry Classification Benchmark (ICB) in 2005 which consists of a four tier structure ( as of Sept 2022; 11 industries, 20 super sectors, 45 sectors, and 173 subsectors).

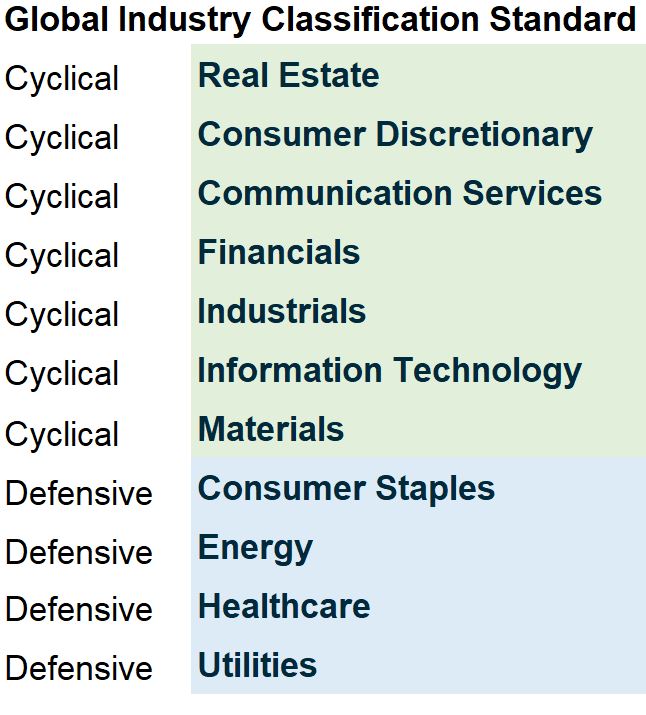

Let’s focus a little more on the MSCI/S&P GICS since they seem to be frequently used in the industry. Table 6 lists the 11 industry Sectors of the GICS.

Table 6 – Global Industry Classification Standard GICS

For example, in the Consumer Discretionary Sector, there are 4 industry groups (Autos, Consumer Durables, Consumer Services, and Retailing).

The Consumer Durables, for example, can be further broken down into 3 industries (Household Durables, Leisure Products, Textile Apparel and Luxury goods).

Refer to Appendix 1 to see the full breakdown of the 11 sectors into their respective 69 industries.

Equity Characteristics – Cyclical vs Defensive Stocks

In Table 6 above we conveniently identified each stock sector as being either Cyclical or Defensive.

This categorization is based on the sensitivity of the stock to fluctuations in the economy.

The profitability of some companies will drop in recessionary periods and rise during market booms.

We call the stocks of these kinds of companies Cyclical Stocks.

- The products and services they sell are called Discretionary Products/Services.

- A luxury goods company stock would be an example of a cyclical stock.

Other companies are not greatly affected by the economy (relative to their cyclical counterparts at least).

They provide goods and services that people need regardless of how weak or strong the economy is.

Stocks of food or energy companies would fall into this category. These kids of stocks are called Non-Cyclical or Defensive or Secular stocks.

Equity Characteristics – Geographic Location

The market value of international (outside US) stocks is more than half the total.

Recall that out of 124.4 Trillion USD of global stock, about 52.2 Trillion USD is US based (42% of total).

That leaves 72.3 Trillion USD (58% of total) of non US based equity (stock).(source: SIFMA Capital Markets Factbook 2022) .

So you definitely need to know the “lay of the land” when it comes to international stocks.

The big three index providers are MSCI, S&P Global, and FTSE-Russell. They all provide stock classifications by country or region. You can learn more about each of these via these links:

S&P Global Country Classification Website ; S&P Global Country Classification pdf Oct 2022

FTSE Russell Country Classification Website ; FTSE Russell Country Classification pdf Sept 2022

MSCI Country Classification Website ; MSCI Country Classification Accessibility pdf June 2022

All of these providers classify countries as Developed, Emerging, or Frontier countries (markets).

As the names suggest, the most developed nations would go in the Developed category whereas the less developed would fall into the Emerging or Frontier categories.

Each provider provides a broad range of criteria in order to classify countries under one of these headings.

Equity Characteristics – Developed, Emerging, Frontier

The S&P definitions for these categories found in this document (S&P Global Country Classification pdf Oct 2022) seem to be generally applicable.

The definitions below are excerpted from this document located at https://www.spglobal.com/spdji/en/landing/topic/market-classification/.

- “Developed: A developed market is the most advanced in terms of economy, financial, and capital markets and satisfies all required classification conditions.” (source S&P Global)

- “Emerging: An emerging market shares some characteristics of a developed market but does not meet the full criteria necessary for that classification.

- Emerging markets may become developed markets in the future, or they might have been in the past. ” (source S&P Global)

- “Frontier: A frontier market is a developing economy with generally lower market capitalization and liquidity and/or more restrictions than an emerging market.

- Frontier markets may become emerging markets in the future, or they might have been in the past.”(source S&P Global)

- “Standalone: A standalone market is a developing economy that does not meet the required basic conditions for frontier markets described above.”(source S&P Global)

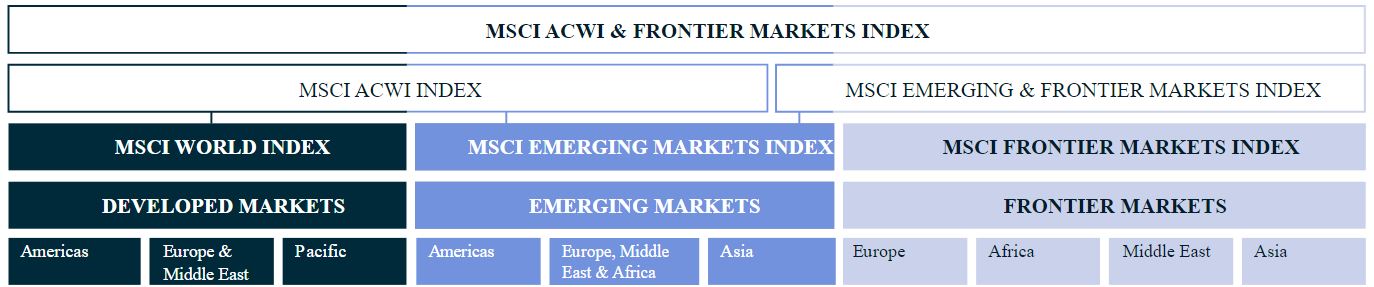

MSCI Country Classifications

MSCI provides a nice graphic for its country classifications.

The partial graphic below in Graphic 5 is copied from the MSCI website.

Note that the standalone countries portion of the graphic is not shown. (see Appendix 2 for a full rendering of the graphic).

Graphic 5 – MSCI Country Classifications (source: https://www.msci.com/our-solutions/indexes/market-classification).

ACWI in the graphic above stands for All Country World Index.

Some example countries in each category are listed below:

- Developed: Americas(USA, Canada), Europe & ME (Germany, Israel, others), Pacific (Japan, Hong Kong, others)

- Emerging: Americas(Brazil, others), Europe, Middle East & Africa(Egypt, others ), Asia(China, others)

- Frontier: Europe (Iceland, others), Africa(Nigeria, others), Middle East(Jordan, others), Asia (Pakistan, others)

- Standalone: Americas (Jamaica, others), Europe (Russia, Ukraine, others), Africa(Botswana, others), Middle East (Lebanon, others)

International Equity Risks

SEC (Investor.gov) has a nice write up on the risks of investing in international stocks (outside USA).

These risks can include (paraphrased from the SEC Investor.gov site):

- Transparency and access to information

- Costs

- Working with non registered brokers

- Changes in currency exchange rates and currency controls

- Political, economic, and social events

- Different levels of liquidity

- Lack of legal remedies

- Different market operations

Keep in mind that many large US corporations have substantial presence and sales worldwide.

So one way to invest internationally is to buy stocks of these large global corporations.

Example of Currency Risk

Let’s finish up this section with an example of currency risk when investing in foreign stocks (non US stocks).

Example_Part 1: You buy 1000 Euros of stock when the exchange rate is 1.2 Euro/1USD.

- So you paid 1000/1.2 = 833 USD

Example Part 2: Some time in the future you sell (assume your investment value in Euros didn’t change).

- If exchange rate is the same: 1.2 EU/1 USD, then you get your 833 USD back. No gain or loss.

- If exchange rate goes down: e.g. 1 EU/1 USD, then you get 1000 x 1 USD/1 EU = 1000 USD (you made money on the currency rate change)

- If exchange rate goes up: eg. 1.4 EU/1 USD, then you get 1000 x 1 USD/1.4 EU = 714 USD (you lost money on the currency rate change).

So, there is a risk of losing money if the exchange rate goes up (EU/USD).

Alternative Investments

Recall Graphic 1 below showing the various asset classes.

We’ve discussed Cash , Debt, and Equity. Now on to Alternatives.

Graphic 1 – Investment Asset Classes

We will review 6 alternative investments

- Real Estate

- Infrastructure

- Commodities

- Derivatives

- Insurance

- Collectibles

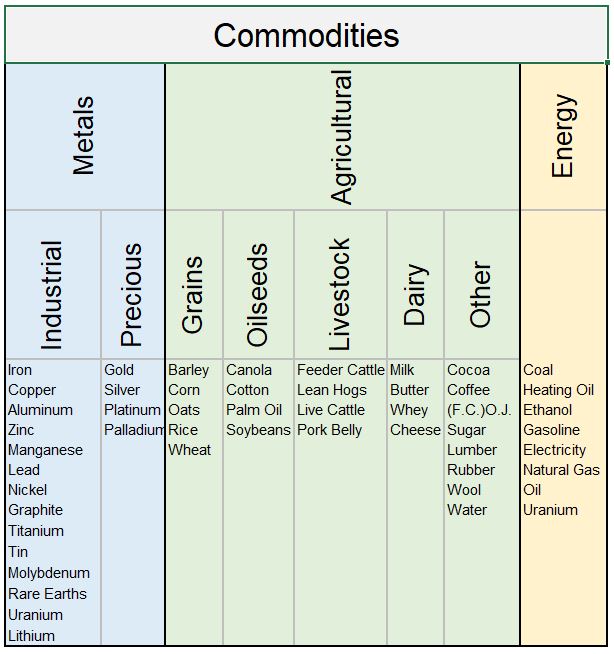

Alternative Asset Classes – Commodities

Like REITs and Infrastructure, Commodities are another type of real, tangible, physical asset.

Commodities are typically raw materials (versus finished products) that can be traded in a market.

Here is a more rigorous definition courtesy of the Library of Congress:

“A commodity is a basic good used in commerce that is essentially uniform across producers, where one unit of a specified size and weight is perfectly interchangeable with another.” Source: https://guides.loc.gov/commodities/introduction copied on 10/14/2022).

We can categorize commodities into three general types:

- Metals ,which can be further broken down into industrial (or base) metals and precious metals

- Agricultural products including livestock (meat) and dairy

- Energy products which can be subdivided further as well

See Table 7 for more detailed listings under each of the three commodity types. I used information from Commodity.com and CMEgroup.com to build the table.

Table 7 – Commodity Types

Professional Investing in Commodities

Professional investors (working for commodity businesses like agricultural companies or food producers) buy and sell futures contracts on various exchanges in to order to hedge against rising or falling prices.

We briefly covered futures in the derivatives section of this post.

- Example 1: A producer of a farm product might want to ensure that they can sell at current prices in the future.

- They can sell a futures contract at an agreed price to be delivered at a future date.

- If prices drop in the future, this hedge succeeds for the company.

- If prices increase, then they lose out at selling at higher prices (for this contract at least).

- Example 2: From the other side: A user of a farm product wants to ensure they buy at todays prices and not higher prices.

- They could buy futures contracts in this case.

- If prices go up in the future, this contract saves money and vice versa.

Some of the major commodities exchanges are:

- CME – Chicago Mercantile Exchange

- NYMEX – New York Mercantile Exchange

- CBOT – Chicago Board of Trade

- COMEX – Commodity Exchange (part of NYMEX)

- ICE – Intercontinental Exchange (digital)

- LME – London Metal Exchange

Individual Investing in Commodities

Retail (Individual) investors might consider commodities because they tend to be inflation hedges and they have a low correlation with stocks and bonds.

However, they have unique features which makes them a bit more complicated, risky, and possibly less flexible then a stock or bond investment (in general):

- They don’t generate income

- Logistics is a cost component of commodities (ships, cars, storage facilities)

- They can have volatile and unpredictable pricing due to unforeseen events in weather or geopolitics for example.

- e.g. Russia is one of the top three producers of Platinum Group Metals (namely Platinum and Palladium) and as its current war with Ukraine drags on (as of Oct 2022), there is potential for future pricing spikes.

The various ways in which individuals can invest in commodities are:

- Buy the commodity directly (practical for high cost density precious metals like gold; not so much for others).

- Buy and sell futures contracts as described in the previous section (you’ll have to meet the requirements of your brokerage if they allow you to do this).

- Invest in corporations (via stocks) that are in the commodity business.

- Looking at the GICS company sectors list (Appendix 1) you could choose stocks in the energy or materials sectors or you could choose stocks in the food, beverage, tobacco industry.

- Let professionals do the heavy lifting for you.

- You can invest in commodities or baskets of commodities via investment pools like Mutual Funds or Exchange Traded Funds (ETFs).

- You can also purchase Exchange Traded Notes (ETNs) which are basically bank notes (like bonds) that are priced based on an underlying commodity price or index.

- ETNs are backed by the banks (typically) that issue them so there is a risk of default.

Investing in Commodities – Buyer Beware

Before you invest in commodity Mutual Funds, ETFs, ETNs, read the prospectus details to understand your risks and how you will pay taxes.

If the funds invest more than a certain amount in futures, you will have to fill out and submit IRS K-1 forms which can be complicated (requiring possible advice from a tax professional).

K-1 forms are typically not submitted in time to meet the April IRS tax reporting deadline (meaning more administrative hassles for you).

ETNs are issued by banks and so you have to consider credit and default risks. See this nice article: Schwab on ETNs

Commodities Investing Sources

Some of the websites I used to write this section are listed below:

Many Investment Options

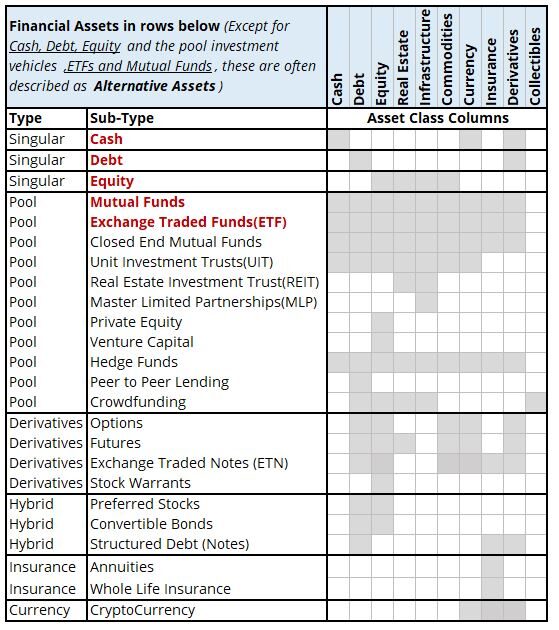

Table 8 below is my attempt to show the many different investment options that are available.

I’m sure I’ve missed some things but I think the table probably captures (at least generally) the majority of investment options available.

This table shows Financial Assets listed in the rows and Asset Classes listed in the columns.

There is duplication (redundancies) in the rows and columns but since the investment options often combine items, I thought the format of the table would be useful.

As you go down each row item, you can look across and see what Assets are (possibly) part of that Financial Asset.

Obviously if you look at the cash row, for example, you will see it aligns with the cash column (not useful) but you see that currency trading can be interpreted as a cash trade.

You also see that Cash or Cash Equivalent derivative investments exist.

Table 8 Observations

In the Financial Asset rows, I’ve made an attempt to categorize these by Type.

- Notice all the “Pool” type investments. These Financial Assets can all be generally described as investment vehicles that pool peoples money and invest in various businesses.

- Derivatives derive their values from underlying assets or price markers. This in itself is a huge category (options, futures, and combinations with other assets)

- Hybrids combine different types of Asset but remember these categories are fluid (they will overlap). e.g. Hedge Funds invest in all sorts of financial instruments.

- People are still trying to figure out how to categorize Cryptocurrencies like Bitcoin. “Digital Currency” seems reasonable.

Table 8 – Asset Class Composition Table

The big thing to take away from Table 8 is, beyond the “traditional investments” (Stocks, Bonds, Mutual Funds, Exchange Traded Funds) , there are multitudinous ways to make (and lose!) money.

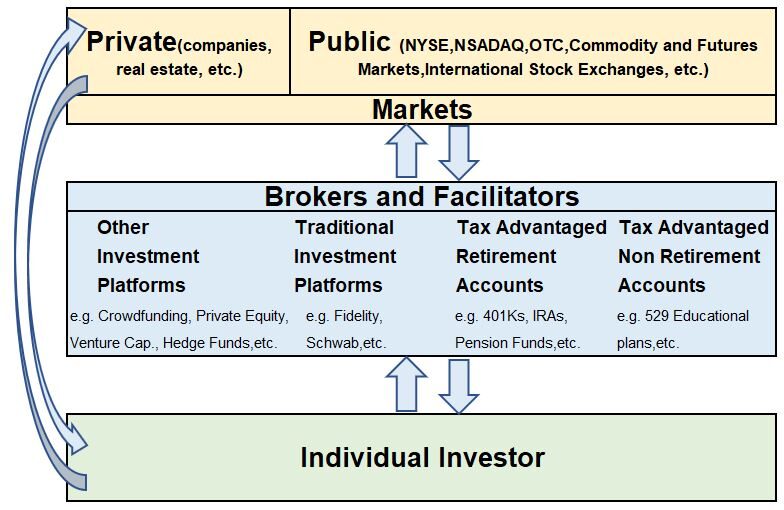

Investment Money Flow

Another way to look at investments is by how the money flows.

Graphic 6 shows that ,typically, there are three players in each investment transaction:

- the investor,

- the broker/facilitator,

- and the market or exchange.

Graphic 6 – Flow of Investment Money

Obviously , there are some investments where the investor is the broker and the transaction does not need a platform (for example , buying a rental house).

But generally, investors will work through some kind of investment platform which facilitates the buying , selling and administration of the investment.

For example, an investor might have a taxable investment platform via Schwab in which he/she can buy stocks through a brokerage system.

The markets in which the actual trades are made can be public markets (namely the large , regulated exchanges) or private markets.

An example of a private market would be private real estate which could be purchased/sold via Crowdfunding Platforms.

Notice that there are Tax Advantaged accounts which are various investments grouped together and managed separately due to their tax status (401ks, IRAs, etc.).

Notice also that there are Tax Advantaged educational investments like 529b plans (college investment plans which allow you to invest in various stock Mutual Funds for example).

Appendix 1 – GICS (Stock Sector, Industry Classifications)

- Return to Industry and Sector Section

- Return_to Infrastructure Section

- Return to Commodities Section

- Return_to Menu

MSCI , S&P Global Industry Classification Standard

Appendix 2 – MSCI Country Classifications

Source: https://www.msci.com/our-solutions/indexes/market-classification

MSCI utilizes several criteria to differentiate countries as Developing, Emerging, Frontier, or Standalone:

Categorization Criteria: (Source: https://www.msci.com/documents/1296102/8ae816b1-fa03-bae3-0bb4-1a3b2bf387bf?t=1656972645260)

- Sustainability of Economic Development

- Size and Liquidity Requirements

- Market Accessibility Criteria (openness to foreign ownership, ease of capital inflows/outflow, efficiency of operational framework, availability of investment instruments, stability of the institutional framework)