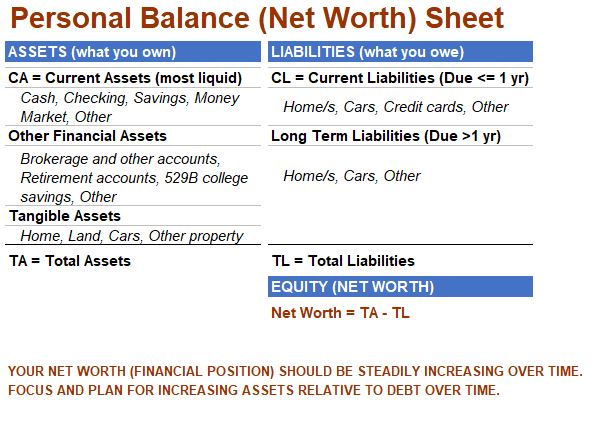

The Personal Balance Sheet

You need to create a personal Balance Sheet tool that you can update on some frequency.

Recall from my Accounting Primer that the Balance Sheet is defined by the Accounting Equation:

Assets – Liabilities = Equity = Net Worth

Graphic 1: Personal Balance (Net Worth) Sheet

Your personal Balance Sheet will show your Net Worth (your financial position) at a specific time.

If your Net Worth is negative or not substantial, then you need to figure out how to increase assets and/or reduce liabilities.

By tracking this on some frequency you can make the adjustments and future plans needed to ensure your Net Worth continues to grow.

It’s very important that you provide as much detail as possible.

This will allow you to do a more thorough analysis of the data (see later section on Personal Financial Ratios).

Create Your Personal Balance Sheet

So, create a detailed and periodically updatable Net Worth template or sheet so you can track your Net Worth growth over time (perhaps quarterly or yearly).

Follow the general design of Graphic 1.

Make a discrete and descriptive listing of everything of value that your family owns.

You can do this manually on a sheet of paper but I’d recommend you do this electronically so you can easily manipulate, analyze, and update the numbers.

The listing should include

- all financial accounts including retirement accounts,

- all hard assets (e.g. home, cars, other property),

- all insurance policies with cash value

- all liabilities (credit, loans, other debt)

- a computation of Net Worth = Sum (assets) – Sum (liabilities)

If you want to save time and effort, download a free template from the internet and then you can modify and adjust it as needed over time.

For example, Vertex offers free downloadable templates (see note below).

Note:

- You can use free internet software tools to do this.

- My favorites are Google (Google Sheets, Google Docs) and LibreOffice (Writer Document, Calc Spreadsheet).

- It will cost you to use Microsoft, but their Word and Excel programs are the most widely used today.

- I strongly recommend you learn how to use Google Sheets or Microsoft Excel since you will then have access to powerful financial calculations that will come in handy for financial planning.

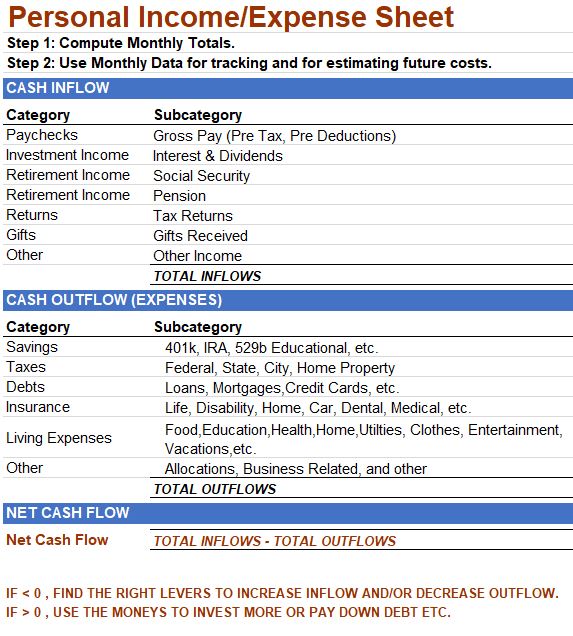

Personal Income/Expense Sheet

Whereas your Balance Sheet will give you a snapshot in time of your Net Worth, your Budget (Income/Expense Sheet) will allow you to track and adjust your saving and spending behavior.

So, you need to build a Budget template or sheet that you can update periodically. This is very important. The structure of the Budget will look like Graphic 2 below.

Graphic 2: Personal Income/Expense Sheet

How to Use Your Budget

How to Use your Budget:

- Record all cash inflows (income) on some frequency (I would recommend monthly to begin with, and then perhaps quarterly or every 6 months after you get a good understanding of your typical monthly numbers).

- Record all cash outflows (expenses).

- Notice that savings are considered expenses.

- Compute your Net Cash Flow = Income – Expenses. The number should be usually positive. The higher the better.

- Make adjustments where possible to income and expenses to ensure that you are typically positive Net Cash Flow.

- Since you will probably have non-monthly income and/or expenses, it’s good to review the budget on a quarterly or semi-annual basis as well.

It’s very important that you provide as much detail as possible.

The details will allow you to do a more thorough analysis of the data (see section on Personal Financial Ratios) and will keep in front of you all the possible levers for adjustment or improvement.

The internet has several free templates you can download. A few of many online resources are listed below: