Taxes and Post Tax Deductions

Now we describe how your income gets reduced by taxation.

Remember that we will not discuss the impact of state and local taxes on your taxes. For example if you live and get paid in New York, you pay city, state, and Federal taxes! Different states employ different tax rules and sometimes your state and local tax payments affect your Federal tax payment.

The goal is to convey key taxation concepts without overwhelming you with the many potential nuances and complexities that might apply to your situation.

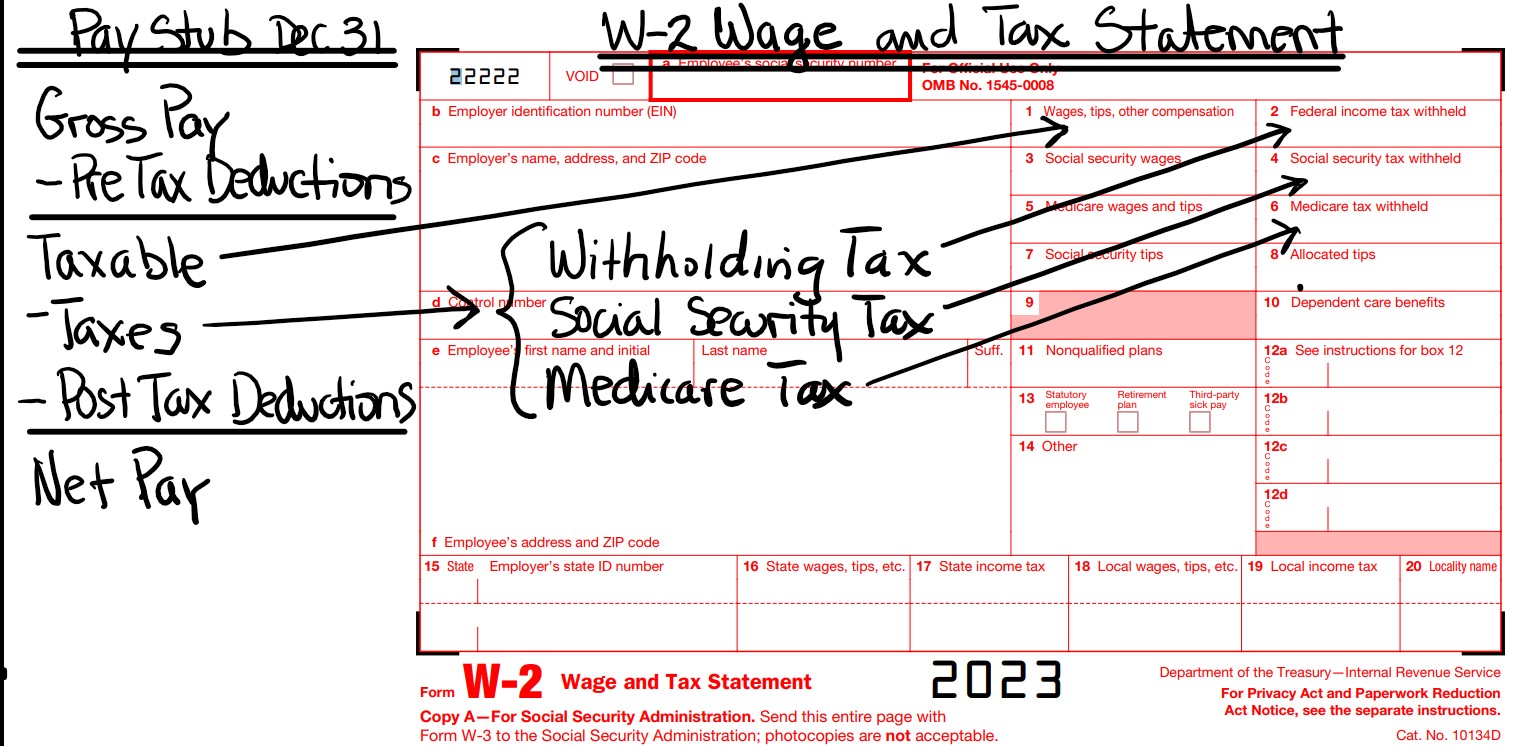

So, back to business; Let’s start with your Taxable Pay. Your total Taxable Pay for the year is shown as the cumulative value in your last Pay Stub of the year. The same exact number should be shown in Box 1 of your W-2 Form.

The W-2 form is sent to you by your employer early in the following year, so you have sufficient time to file your previous year tax paper work in April (typically).

Generally, income is automatically taxed in two general ways:

- FICA (Federal Insurance Contribution Act) Taxes (AKA Payroll taxes)

- Withholding Tax

FICA Taxes

FICA Taxes are also known as Payroll Taxes or Social Insurance Taxes. The Federal Insurance Contribution Act, FICA, mandates that taxes that fund Social Security and Medicare be levied from your Gross Income. There are two tax components to FICA.

- Social Security Tax (Up to a certain threshold limit on income shown in W-2 Box 3, you and your employer each pay a social security tax (e.g. in 2023 it was 6.2% and 6.2% respectively). W-2 Box 4 shows the amount of SS tax paid.

- Medicare. In 2023, you pay 1.45% on your income but you pay an extra .9%(in 2023) if your income exceeds a certain income threshold (depends on your tax filing status). Your employer also pays the same amount (1.45% in 2022). W-2 Box 5 shows the wages subject to Medicare taxes and W-2 Box 6 shows how much was paid through the year.

Note that your W-2 Box 5 might not match your W-2 Box 1 Wages (it can be higher for example). This is because wages subject to Medicare taxes will be your Gross Pay minus all of your pre-tax benefits except for any deferred contribution deductions (401(k) plans for example).

Note! Elective Deferral Amounts (e.g. 401k and other deferrals) Are Taxed for Social Security and Medicare

I mentioned this in a previous section but it’s good to review again.

FICA or Payroll Taxes are applied to Gross Income after some adjustments are made. Before FICA taxes, your Gross Income is adjusted down (reduced) by medical/dental insurance payments and accident insurance payments (for example) but not by any money you elected to defer into your tax free 401k account (for example).

What did you say? Yes, your “tax- free” elective deferral (401(k) or 403(b) or 457(b)) is (typically) not really fully tax free. It’s free from the graduated income tax brackets for ordinary income, but it still flat-taxed at the Medicare and Social Security tax rates.

See IRS publication 15 to understand what portion of your Gross Pay is taxed for Social Security and Medicare ( see section in publication 15 titled “Special Rules for Various Types of Services and Payments”).

This is why, on your W-2, you actually have three tax basis numbers provided:

- Box_1 matches your Taxable Pay on your Pay Stub and is the basis for the ordinary income tax tax brackets.

- Box_3 is the basis for your Social Security taxes (same basis definition as Medicare but it is capped).

- Box_5 is the basis for your Medicare taxes (not capped and adds an additional tax if you make more then a certain threshold).

Withholding Taxes

The amount of taxes already paid (withheld) for the year is shown in form W-2 box 2. Your cumulative end of year Pay Stub shows this value as well.

Withholding taxes are supposed to cover all taxes owed (except the FICA taxes which are paid separately using flat tax rates). Examples of types of taxable income would be:

- Pay: taxed as Ordinary Income

- Stock Dividends from stocks owned for less than 60 or 90 days (for preferred stocks): taxed as Ordinary Income

- Asset short term capital gains (owned less than one year): taxed as Ordinary Income

- Asset long term capital gains (owned more than one year): taxed as Long Term Capital Gains

- Stocks dividends from stocks owned at least 60 or 90 days (for preferred stocks): taxed as Qualified Dividends

- Others

We’ll cover the tax implications for Ordinary Income vs Long Term Capital Gains and Qualified Dividends when we run through our example in a later section.

Your employer, with information provided by you via an IRS form W-4 , automatically takes out a certain percent of your taxable pay based on guidance from the Internal Revenue Service (see IRS publications 505 and 15-T).

From one year to the next you have the ability to adjust for additional withholding amounts (through your employer) if you significantly underpaid the amount owed.

Estimated Tax Payments

Remember that your Federal income tax is a pay-as-you-go tax, so you are supposed to pay when you receive the income.

The IRS also allows you to submit periodic Estimated payments if you have non periodic income, hard to predict income, and/or very large income streams.

For example, the income you make from stock or other investments each year might produce hard to predict income or you might have received a windfall amount of income. In this case, you might have to make estimated tax payments to ensure you don’t get late payment penalties.

Post-Tax Deductions

There are additional post-tax deductions that your Pay Stub accounts for. These might be items like company insurance benefits or stock purchase benefits among other things.

Net Pay

Your net pay is what remains after all the adjustments are made. It is what is sent to you as your “take-home” pay.

Net Pay = (Gross Pay) – (Taxes Paid) – (Post and Pre Tax Deductions)

Summary

Schematic_1 shows you the interconnectivity of your Pay Stub and your IRS form W-2.

Schematic 1: Pay Stub and IRS Form W-2

So, in summary, given that (1) US Federal income taxes are a pay-as-you-go system and (2) a potentially big component of what you paid is based on an estimated withholding amount, the US government expects you to reconcile what you have already paid with what you owe.

Filing your taxes essentially is the process of reconciling what you’ve already paid with what is actually due.

You might get a refund back if you overpaid or you might owe additional monies. The IRS wants you to stick to the rules of pay-as-you-go which means, if you underpay by too much (less than 90% of what you owe), you will pay a penalty on top of what you owe.

Example Tax Filing

(Tax Example) 1. Setup

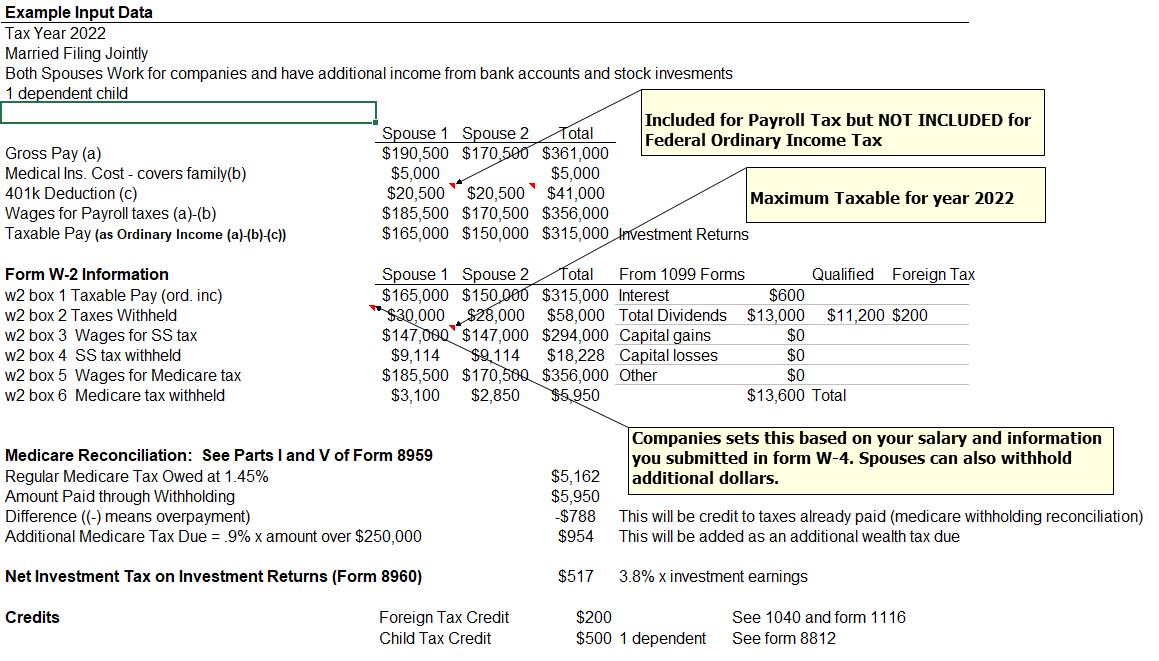

For our example, we have a middle aged couple, with one dependent child, who will file their taxes jointly. There is no State Income Tax.

Assume the following:

- Gross Pay (a) $361,000

- Medical/Dental Ins. Cost (b) $5,000

- 401k Deductions (c) $41,000

- Wages for Payroll taxes (a)-(b) $356,000

- Taxable Pay (as Ordinary Income (a)-(b)-(c)) $315,000

- W-2_box 1 Taxable Pay (ord. inc) $315,000

- W-2_box 2 Taxes Withheld $58,000

- W-2_box 3 Wages for SS tax $294,000

- W-2_box 4 SS tax withheld $18,228

- W-2_box 5 Wages for Medicare tax $356,000

- W-2_box 6 Medicare tax withheld $5,950

- Interest $600

- Total Dividends $13,000; $11,200 (Qualified); $200 (foreign taxes paid)

- Capital gains $0; Capital losses $0; Other $0

If you download the calculator spreadsheet , you can see more details on the input data in the “Example Input” tab. I’ll take you through the example step-by-step in the following sections of this post ,so you don’t really need this to understand the example.

Example Input Summary

(Tax Example) 3. Update Tax Brackets and Filing Status

Embedded Calculator Sections 1, 2, and 3

We now want to start going through and updating the Federal Tax Estimator Tool (embedded above in this post or you may want to download it here).

Start at the top and work down sequentially. All Blue Fonted cells have to be updated (or at least reviewed to ensure they are up to date).

⇒ Enter the tax year (this will be 2022 in our example)

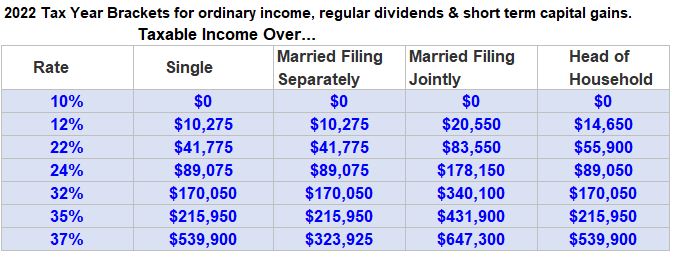

⇒ Update the Tax Year Tax Brackets ( find via the web. Try IRS.gov or Turbo Tax or H&R Block web sites to get these). The numbers for 2022 are shown in Table 1.

⇒ Enter your Filing Status from the lookup list. In our example, we have a married couple that is filing jointly.

Table 1: 2022 US Federal Ordinary Income Tax Brackets

Tax Bracket Observations

- They don’t apply to longer held investment income (Qualified Dividends and Long Term Capital Gains)

- Tax Brackets apply to Ordinary Income (like your pay), Short term Dividends (from investments held less than 60 or 90 {for preferred stocks] days), and short term Capital Gains (from assets held less than 1 year).

- They are graduated or progressive, meaning, your income is broken into sequential amounts (or tranches) that are taxed at higher and higher tax rates.

- As you make more money you are taxed more. I’m guessing that for most people, the perceived fairness of this system is inversely proportional to the amount of money the perceiver is making!

- There are 7 progressive tax rates today (10%, 12%, 22%, 24%, 32%, 35%, and 37%). When you hear the term Marginal Tax Rate, it is referring to one of the above tax rates.

- Note that if you are in the highest tax rate of 37% for example, that does not mean that you are paying 37% taxes on all your money. The 37% would only apply to the tranche of money in that 37% tax bracket.

- So, if you’re a single filer and you make $150,000/year, you’re in the 24% marginal tax bracket and you’ll pay 24% taxes on $60,925 ($150,000 – $89,075 = $60,925).

- Your Effective Tax Rate (Tax Paid/Taxable Amount) might be a more valid way of quantifying the amount of taxes you actually paid (in total).

- The basis for this Effective Tax Rate should always be defined (e.g. is it based on Taxable Income or Adjusted Gross Income?).

(Tax Example) 4. Update FICA Taxes

Embedded Calculator Section 4

Recall that, the Federal Insurance Contribution Act, FICA, mandates that taxes that fund Social Security and Medicare be levied from your Gross Income. There are two tax components to FICA: Social Security and Medicare.

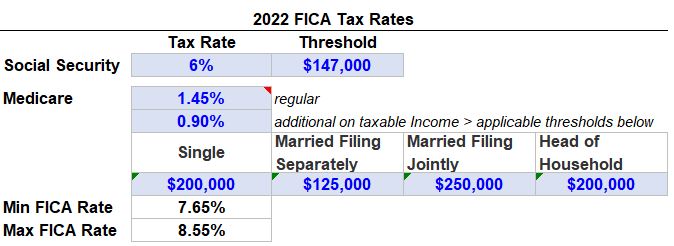

⇒ Update the FICA (SS and Medicare tax) rates from the web.

I obtained this information from a web site called benefitsattorney.com but you can find several others online (e.g. in ssa.gov , search for Social Security and Medicare taxes).

Notice the additional tax of .9% on income over a filing status threshold.

For 2022, the FICA taxes are shown in Table 2 below.

Table 2: 2022 FICA Tax Rates

Note that the embedded Tax Calculator doesn’t use these tables to do any FICA tax calculations.

But it’s useful information you can use to check against your Pay Stub and your W-2 form to understand how your FICA taxes were calculated.

The calculator does, however, reconcile Medicare taxes you have paid and we’ll discuss this more in later steps.

⇒ Enter your total W-2 box 4 (Social Security tax withheld) and box 6 (Medicare tax withheld).

We’ll use these to compute the total true tax rate you are paying in Section 12 of the calculator.

Please note that elective employee contributions and deferrals (like amounts you put in your 401(k) or equivalent plan) ARE TAXED for Social Security and Medicare.

You often hear these described as pre-tax deductions but this is only true when referring to the Federal ordinary income graduated tax rates (based on Taxable Pay which does not include deferred contributions).

(Tax Example) 6. Qualified Dividends and Long Term Capital Gains

Embedded Calculator Sections 6 and 7

Let’s define two useful terms here.

Earned Income: Your Paycheck income is considered Earned Income. It’s Taxed as Ordinary Income (i.e. the Federal tax brackets apply).

Unearned Income: Almost all other forms of income including pensions, retirement income, social security payments, and investment income (interest, dividends, capital gains).

Depending on what type of Unearned Income it is, these could be taxed as Ordinary Income, Qualified Dividends, or Long Term Capital Gains.

- Pensions, Social Security, and other Retirement Income – Taxed as Ordinary Income

- Short Term Investments Income – Taxed as Ordinary Income. Recall that short term investments are based on how long the underlying investment was held.

- For Dividends, short term refers to less than 60 or 90 days depending on the type of stock. For Capital Gains, short term refers to less than one year.

- Long Term Investment Income – Taxed as Qualified Dividends (held > than 60 or 90 days) or Long Term Capital Gains (held > 1 year). The same tax rates apply to both.

Note: There could be other forms of income from real estate or other investments that might require special treatment.

Calculate Long Term Capital Gain and Qualified Dividend Taxes

⇒ Update the LTCG and QD Tax Rate table in section 6b of the Tax Calculator.

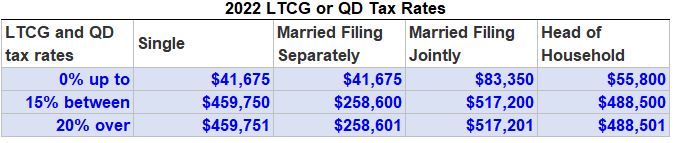

You could use hrblock.com among many on-line sources to obtain this information. See Table 3 below for 2022 tax rates for Long Term Capital Gains (LTCG) and Qualified Dividends (QD).

Table 3 – 2022 LTCG and QD Tax Rates

In our example , the income for Married Filing Jointly is between $83,350 and $517,000 so a 15% percent tax rate will apply for Qualified Dividends and Long Term Capital Gains.

⇒ Update the Qualified Dividend amount in section 7a. A lookup calculation should select 15% from the table above.

We’ll assume that from form 1090-Div 1b, that the Qualified Dividends are $11,200. So the couple in our example will owe taxes of $1,680 on their Qualified Dividend earnings.

⇒ We’ll assume no Long Term Capital Gains for our example, so section 7c input is 0.

The calculator can now compute the portion of the Taxable Income that is going to be taxed via the Federal ordinary tax brackets.

Taxable Incomenot including QD or LTCG = Taxable Income – QD – LTCG = $302,700-$11,200-$0 = $291,500.

(Tax Example) 7. Ordinary Income Tax

Embedded Calculator Section 8

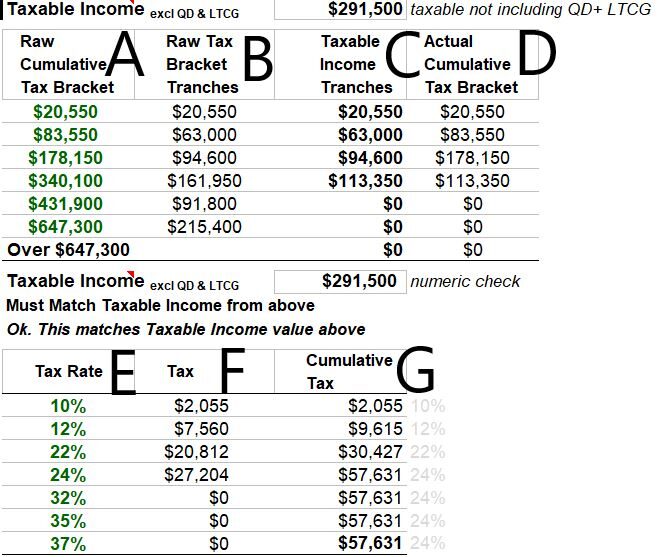

So the Ordinary Income in our example is $291,500. The calculator will use the Federal graduated income tax brackets to compute the taxes owed on this amount. Refer to Table 4 below.

Table 4 – Income Tax Calculation Table for Ordinary Income

Column C in Table 4 is computed from data in Columns A, B, and D. In column C, the total taxable amount of 291,500 is broken up into sequential tranches (groups) of income.

If you sum all the numbers in Column C you will get $291,500. Now each tranche is taxed at its marginal tax (see Column F). So,

- The first $20,550 is taxed at 10% = $2,055

- The second $63,000 is taxed at 12% = $7,560

- $94,600, the third tranche, is taxed at 22% = %20,812

- The Fourth and final $98,350 is taxed at 24% = $27,204

The total tax (on Ordinary Income) owed will be the sum of these taxes (see Column G) which is $57,631. 24% was the highest marginal tax rate used.

Note that only a portion of the income was taxed at this highest rate. For this reason this kind of taxation is called a progressive or graduated.

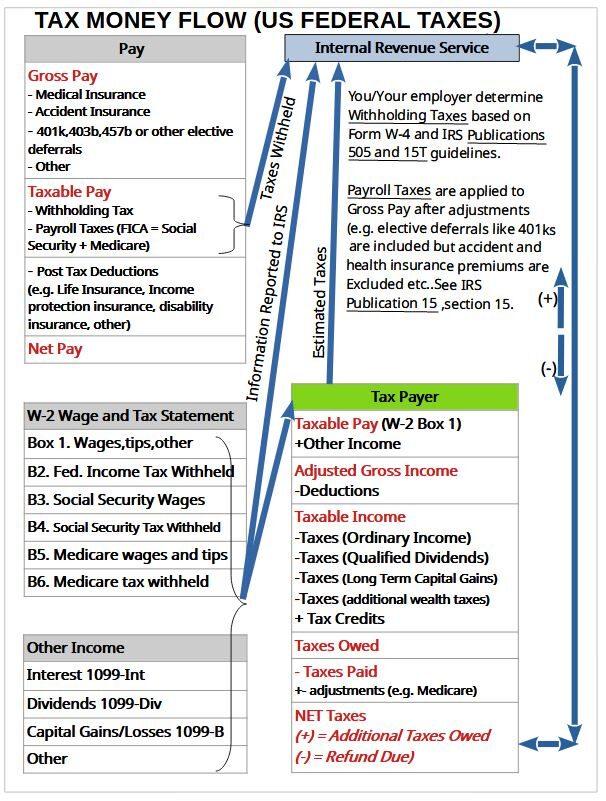

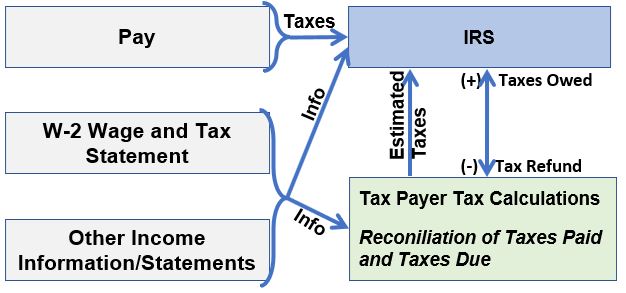

Tax Reconciliation Process Flow Diagram

The diagram below gives you a picture of the various aspects of a tax filing (reconciliation) process that we walked through in our example.

It shows the relationships among sources of information , tax payer calculations, and the IRS.

Schematic 2: Tax Reconciliation Process Flows

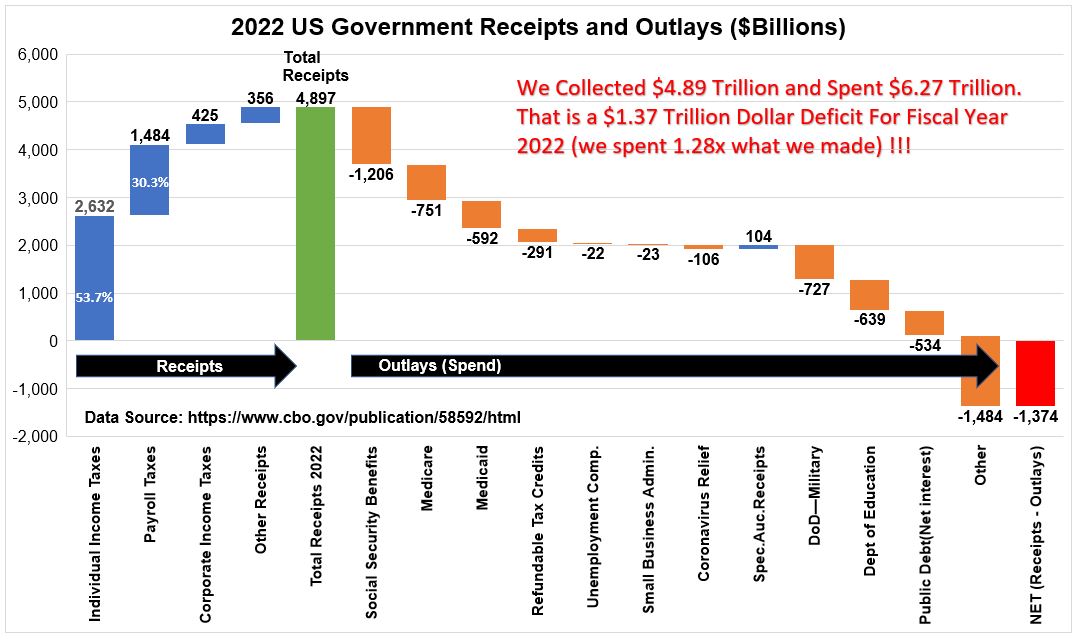

2022 US Tax Receipts and Outlays

In this section we’ll show how your tax contributions figure into total US Government receipts (taxes) and outlays (spend).

If we assume that Payroll taxes are split evenly between corporations and individuals, individuals contribute to about 68.9% of total government receipts.

See Graph 1 below for a detailed breakdown of what the US Government brings in versus what it spends. Does anything about this chart give you any concerns?

You can see that in 2022 the US Government ran a deficit (they spent more than they made). You wouldn’t want to run a budget deficit personally because you wouldn’t want to go broke and run out of money.

The government’s budgeting tasks are obviously way more complicated than your budget (they ) but on a fundamental level does this feel right to you?

Well, I think the answer to my somewhat rhetorical question is…it will depend.

Your answer and your point of view will probably depend on your personal financial condition, your educational background, your family background and history, your wealth, and myriad other variables.

Graph 1: 2022 US Government Receipts and Outlays.

Are you curious about how common it is for our Federal Government to run a deficit? Answer: The US Government has run yearly deficits since 2001.

See Graph 2 below, which is a copy from fiscaldata.treasury.gov. According to fiscaldata.treasury.gov, “From FY 2019 to FY 2021, Federal spending increased by about 50 percent in response to the COVID-19 pandemic.”

Note: the $1.38 Trillion from Graph 2 and $1.374 Trillion from Graph 1 are meant to represent the same number (assume the difference is due to round-off error).

Graph 2: US Government Yearly Federal Deficits Since 2001

Conclusion

Hopefully you’ve gained a deeper understanding of how a typical US Federal income tax filing is done. Remember that your yearly tax filing is the reconciliation component of a pay-as-you-go tax system.

See Schematic 3 for a high level schematic of the relationships and flows among the data sources, the tax payer, and the IRS.

Schematic 3: Generalized Tax Process Flow Blocks

Caveat Emptor Regarding Use of this Post and the Embedded Tool

Summary of Key Concepts and Methods Related to Tax Filing

Process Learnings

- The IRS (Internal Revenue Service) employs a pay-as-you-go tax system. That is, taxes are expected to be paid at the time you receive your taxable income.

- If you underpay by more than 10%, you will have to pay a penalty fee.

- There are two primary means of tax payments to the IRS: Automatic Withholdings from your paycheck and Estimated Tax payments.

- Withholdings are determined by your company, your W-4 information, and your adjustments for additional withholdings.

- Once a year (typically due on Tuesday of 3rd week in April) ,you must reconcile your taxes-paid with taxes-owed.

- You will either send the IRS the additional taxes owed or receive from the IRS your refund.

- The IRS levies a Flat Payroll Tax on your company pay. This funds the Federal Social Security and Medicare programs.

- The_Payroll_tax_basis will be your Gross Pay adjusted down by some health and accident insurance benefits (but not by your elective 401(k) deferrals).

- The IRS levies a Graduated (Progressive) Tax on ordinary income (e.g. pay and investment income from short term holdings).

- The_ordinary_income_tax basis will be Gross Pay adjusted down by health and accident insurance but also any elective deferral payments (e.g. 401(k)s).

- The IRS levies Capital Gains (Qualified Dividend) Taxes on dividends or capital gains from investments held for longer durations.

- How you quantify how much tax you paid relative to your pay depends on the definition you use.

- The Marginal Tax Rate is the highest applicable tax rate, but it’s only applied to the tranche of taxable income that is in that bracket.

Your Actual Tax Filing

- Your actual tax income streams, the amount of money you make, your age, your health, where you lived and worked, the types of company benefits you receive and myriad other details that only apply to you could render the embedded tax tool very inaccurate.

- Use the embedded tool and information provided in this post , therefore, for educational purposes only.

- I do my taxes using easy to use Tax Software. You can do your own research on the top software packages to use.I’ve used H&R Block and Intuit Turbo Tax before and they both seem to work fine for me.

- Your tax situation might be much more complicated than mine so you might be using third parties to help you complete/submit your taxes.