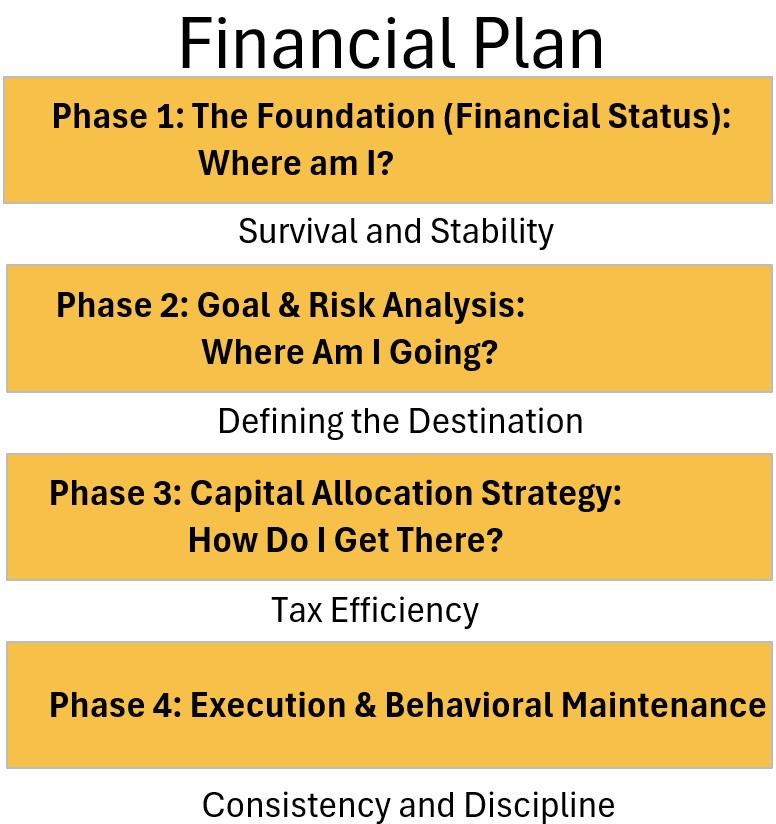

The Master Investment Stack (2026 Edition) – Descriptive Outline

Goal:

Capture every tax advantage and guaranteed return in the most efficient order (by sequential stacking).

Tax Efficiency. Use the right “containers” to reduce your lifetime tax bill.

To optimize every dollar, assets should be deployed into specific “containers” starting with the order provided below.

See my post Tax Advantaged Plans and Other Capital Allocation Structures for more details on the various legal and tax related containers (wrappers, buckets, entities, vehicles) available to you.

Our focus here is Tax Efficiency. Use the right “containers” to reduce your taxes.

And remember (in Phase 1 of your Financial Plan), you should have already addressed and established your Emergency Fund, your high-interest debt clearance plan, and your core protective layers (Insurance/Will/Power of Attorney).

The Essentials (Foundation)

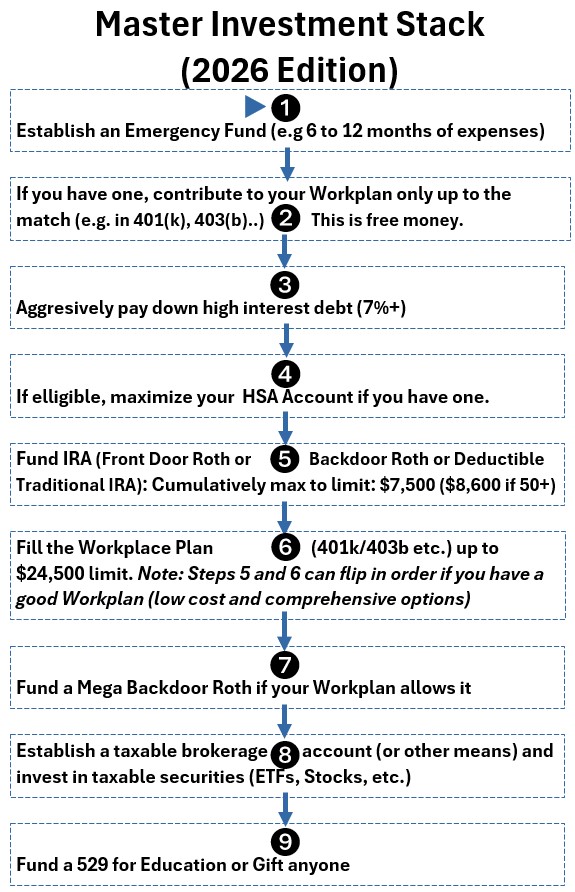

1. Establish an Emergency Fund: Target for 6 – 12 months of expenses in high-yield savings.

We mentioned this in phase 1 of the Financial Plan as well, but it makes sense to include it here as well as a thing you need in place before you proceed with “investing”.

2. The Employer Match: Contribute to your 401(k)/403(b) only up to the match. This is a guaranteed 100% return.

- Contribute to 401k/403b/TSP up to the match limit (Free Money).

- This is an immediate, guaranteed 100% return on your investment.

- The Logic: No other investment—and very few debts—can consistently beat “free money.”

- Even if you have a loan at 7%, the 100% gain from a match effectively “outruns” the interest you’re paying.

At this point, plan on contributing exactly what is needed to get the full match but not more (because every dollar beyond might be better spent elsewhere in the stack first)

The Toxic Waste & Triple-Tax Wins

3. High-Interest Debt (7%+): Drastically reduce or eliminate. This is a guaranteed return equal to the interest rate.

We described this as an action in phase 1 of the Financial Plan but we can make a strong argument that you ought to immediately do the employer match to get that free money first.

4. HSA (Health Savings Account)

- Maximize your HSA (If you have a high-deductible medical insurance plan).

- Max out ($4,400 Individual / $8,750 Family). Invest in stocks/ETFs inside the account for triple tax-free growth.

- The HSA is the only “Triple Tax Advantaged” account in existence.

- Tax-free going in: Contributions lower your taxable income today.

- Tax-free growth: You pay $0 in taxes on capital gains or dividends while the money grows.

- Tax-free coming out: As long as it’s used for medical expenses (now or 30 years from now), you never pay a cent in tax.

- It is effectively “super-powered” compared to a 401(k) or IRA.

The “Quality Control” Fork (IRA vs. Workplan)

Note: The order of 5 and 6 below is interchangeable depending on the quality of your employer’s plan.

- If your workplan (e.g. 401k) has high administrative fees (>0.50%) or poor fund choices, do the IRA first.

- If your workplan offers low-cost institutional index funds, you can fund it first for simplicity.

5. IRA (Roth and/or Deductible Traditional)

- Maximize for tax-free growth.

- Max out your $7,500 ($8,600 if 50+).

- The Roth is often (but not always) the superior choice over a Traditional IRA for long-term flexibility.

- Roth IRAs often offer better investment flexibility than workplace plans.

- Most workplace plans (401ks) have limited, sometimes expensive fund choices.

- An IRA at a firm like Vanguard or Fidelity lets you buy almost anything with near-zero fees.

- The “Roth” Advantage: If you expect to be in a higher tax bracket later, paying taxes now (Roth) lets you lock in a lifetime of tax-free growth.

- The “Traditional” Advantage: If you are in a high tax bracket now, a deductible IRA provides an immediate tax break to help you save more.

6. Fill the Workplace Plan

- If you still have investable cash, the 401(k)/403b/TSP provides a massive “tax bucket” ($23,500+ limit) to lower your current tax bill or build a massive tax-free Roth nest egg.

- Once your match and IRA are maxed, return here to shield more income from the IRS.

- Finish the remaining $24,500 limit (total employee contribution) in your 401(k)/403(b).

- If your Workplan offers enough flexibility at low cost, you could flip the order of 5 and 6.

7. Mega Backdoor Roth

- This is an “advanced maneuver” to get massive amounts of money into a Tax-Free Roth status.

- If your plan allows “after-tax” contributions, you can

- effectively bypass the standard $7,500 (for 2006) IRA limit and

- move tens of thousands more into a Roth environment where it will never be taxed again.

The Taxable “Overflow”

8. Taxable Investments

This is your “Accessibility & Bridge Fund.”

While the previous steps focused on tax-sheltered accounts that often restrict your money until age 59½, taxable investing provides total liquidity.

- This step is about building wealth that is available to you at any time, for any reason

- whether that’s retiring early, starting a business, or making a major lifestyle purchase before reaching retirement age.

- Unlike IRAs, you pay taxes on dividends and realized capital gains along the way.

- However, this is the “price of admission” for having no age restrictions or withdrawal penalties.

- This can be executed through a standard brokerage account, directly with mutual fund companies, or via other taxable security platforms.

- To minimize the tax drag, investors typically use “tax-efficient” assets here

- like total market index funds or municipal bonds rather than high-turnover funds that create large annual tax bills.

- Why here? No limits or age restrictions, but you have “tax drag” (yearly taxes on dividends and capital gains).

Legacy/Gifting/Other (e.g. Low Interest Debt)

9. Legacy/Pay down low interest debt

Now you are ready to move wealth to the next generation without the IRS taking a cut.

- Education (529)

- Money grows tax-free specifically for school.

- It’s like an IRA, but for tuition.

- Estate Planning

- By gifting money now, you reduce the size of your future taxable estate.

- The “Lifetime Exemption” is massive, but reporting gifts over the annual limit (e.g., $18,000) ensures the IRS tracks your total “wealth transfer” over time.

- Other

- Pay off lower interest debt (e.g. sub 5% mortgages)

2026 Contribution Limit Cheat Sheet (Quick Reference)

- Account: Workplan (401k/403b)

- Contribution Limit: $24,500 (+$8,000 if 50+)

- Account: IRA (Roth/Trad)

- Contribution Limit: $7,500 (+$1,100 if 50+)

- Account: HSA (Self/Family)

- Contribution Limit: $4,400 / $8,750 (+$1,000 if 55+)

Go to Menu