Introduction

A financial plan is only as strong as its weakest link.

To move from financial instability to long-term wealth, you need a repeatable framework that accounts for math, taxes, and human psychology.

The following four-phase roadmap provides a direct, step-by-step path:

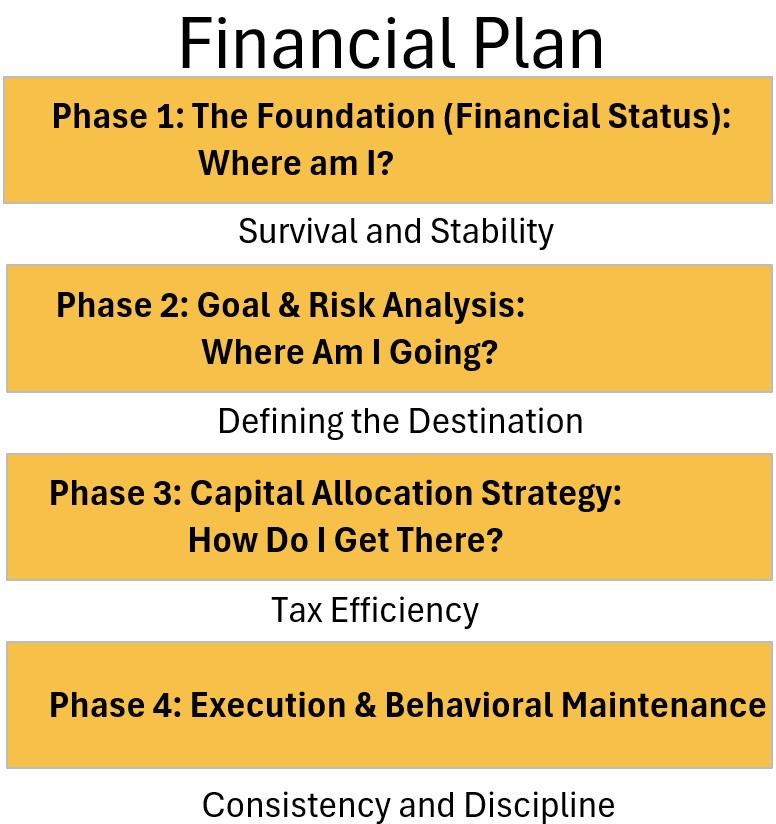

Table: Financial Plan Phases

Phase 1: The Foundation (Financial Status)

- Start with a rock-solid foundation.

- Theme: Survival and Stability

This initial stage is about stripping away ambiguity to understand your current net worth, cash flow, and immediate liabilities.

By establishing a “ground zero,” you create the security necessary to move from reactive survival—like managing high-interest debt—to proactive stability.

The focus here is on building a cash reserve that acts as a buffer against life’s unpredictability.

Phase 2: Goal & Risk Analysis

- Define your retirement target.

- Theme: Defining the Destination

Once the floor is leveled, you must determine the specific “why” behind your wealth-building, whether that is early retirement, a primary residence, or legacy planning.

This phase involves quantifying your time horizon and your emotional capacity for market volatility.

Mapping out these variables transforms vague desires into a concrete mathematical target and a risk profile that prevents panic during market downturns.

Phase 3: Capital Allocation Strategy

- “Stack” your capital into the most tax-efficient accounts

- Theme: Tax Efficiency

With a destination in mind, you select the specific vehicles—such as 401(k)s, IRAs, or brokerage accounts—that will carry your capital toward your goals.

High-level strategy focuses on optimizing “asset location” to minimize the long-term erosion caused by taxes and fees.

Choosing between tax-deferred and tax-exempt accounts, like a Roth IRA, ensures that you keep the maximum amount of your compound growth.

Phase 4: Execution & Behavioral Maintenance

- Automate the behavioral discipline required to stay the course.

- Theme: Consistency and Discipline

The final phase is the longest, requiring the automation of contributions and the emotional fortitude to ignore short-term market noise.

Success here isn’t about brilliant timing, but rather the boring, repetitive habit of staying invested through various economic cycles.

It is the bridge between a well-designed plan on paper and the actual realization of financial independence.

Before I address each phase with a little more data, the next section contains a template of the whole process that you can print out or copy.

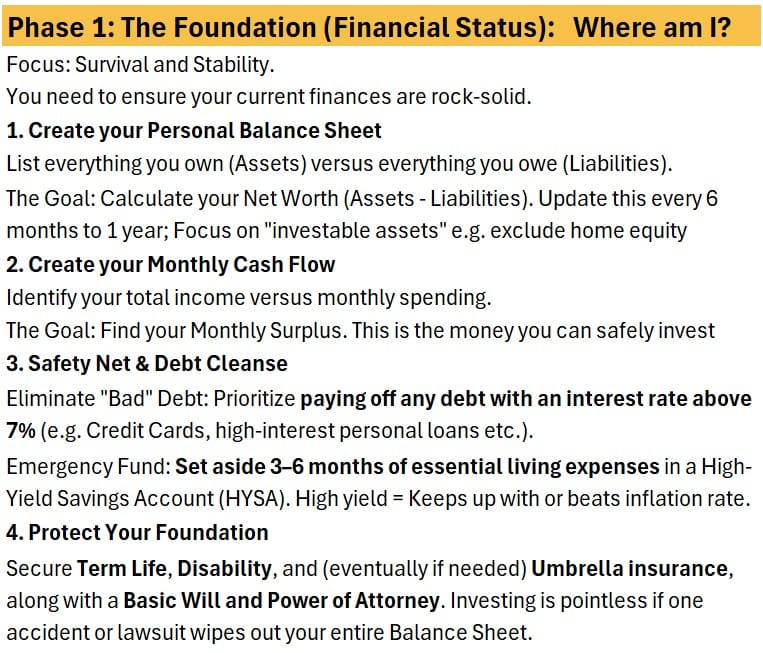

Financial Plan: Phase 1: The Foundation (Financial Status)

Goal:

Survival and Stability.

Ensure your current finances are rock-solid before moving forward.

Ensure a reliable monthly surplus.

Before investing, you must secure your current position by auditing your Personal Balance Sheet…

1. Calculate your Net Worth (Using a Personal Balance Sheet)

- List Assets (what you own) vs. Liabilities (what you owe).

- Focus: Investable assets (exclude home equity for retirement math).

- See Appendix 2 for a net worth computation template.

and calculating your Monthly Cash Flow…

2. Start Tracking your Cash Flow (Create a Budget)

- Start Tracking your cash flow (money in and money out)

- Establish a budget.

- See Appendix 1 for a budget calculation template.

A monthly cash flow analysis can probably be relaxed once you get a good understanding of your cash flows.

- Depending on your situation and your familiarity with your budget, you can adjust the update frequency as needed.

- The important thing is to get started and start getting familiar with your specific financial condition.

- You can’t change or improve what you don’t monitor.

Immediate actions include:

3. Safety Net (Liquidity) & Debt Cleanse

- Eliminate “Bad” Debt: Pay off anything with an interest rate > 7% (Credit Cards, personal loans).

- Emergency Fund: 3–6 months of essential living expenses in a High-Yield Savings Account (HYSA).

4. Protect Your Foundation (Risk Mitigation)

- Secure Term Life, Disability, and (eventually if needed) Umbrella insurance, along with a Basic Will and Power of Attorney. (See Appendix 3 for more on Insurance)

- Investing is pointless if one accident or lawsuit wipes out your entire Balance Sheet.

Table: Financial Plan Phase 1: Determine Your Financial Status

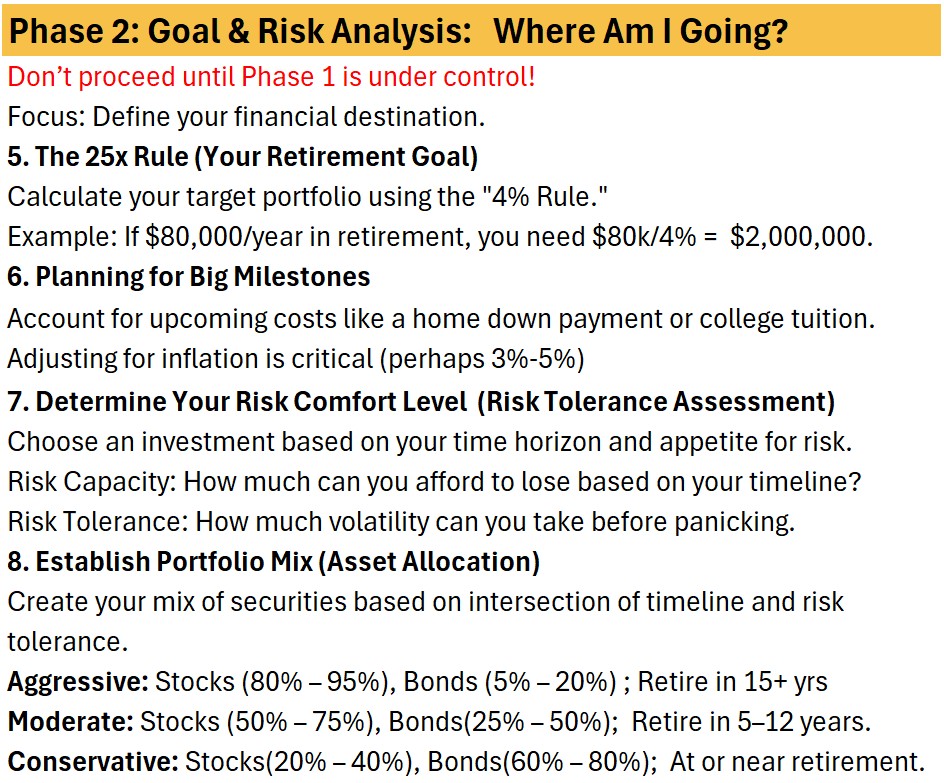

Financial Plan: Phase 2: Goals & Risk Analysis & Investment Allocation Design

Goal: Define your destination and the vehicles.

Do not proceed until Phase 1 is under control.

Once you know where you are, you can start figuring out where you want to go.

5. The 25x Rule (Retirement Target)

This step establishes your “Finish Line.” Without a specific number, investing can feel like running a race without a map.

By multiplying your desired annual income by 25, you are reverse-engineering a portfolio size that—historically—can sustain you for 30+ years without running out of money.

- Use the “4% Rule” to find your target portfolio size.

- Example: If you need $80k/year, your goal is $2,000,000 ($80,000 ÷ 0.04).

- See my post: Bang for your Bengen: The 4 Percent Rule

Doing this transforms a vague “I want to retire” into a concrete, mathematical objective.

It allows you to track progress (e.g., “I am 40% of the way to my number”).

6. Milestone Planning

Life doesn’t stop while you save for retirement.

This step prevents your long-term plans from being derailed by short-term needs.

- Account for major milestones (the ‘Whales’) like weddings, home down payments, or college tuition. Adjust for a 3–5% inflation rate.

- The Inflation Factor: Because a $50,000 tuition bill today might be $80,000 in fifteen years, you must adjust these targets upward.

- This ensures that when the milestone arrives, you aren’t forced to raid your retirement accounts or take on high-interest debt to cover the gap.

7. Risk Assessment

The Purpose: To find the “Sleep Well at Night” (SWAN) factor.

Understand your risk tolerance.

Math vs. Emotion:

Risk Capacity is about your timeline.

- How much can you afford to lose based on your timeline?

If you are 25, you have decades to recover from a market crash. You have high capacity.

Risk Tolerance is about your temperament.

- How much volatility can you take before panicking?

If a 20% drop in your account makes you want to sell everything and hide under the bed, you have low tolerance.

The Balance: Your plan must satisfy both.

There is no point in having a “mathematically perfect” aggressive plan if you abandon it the moment the market gets bumpy.

8. Asset Allocation (The Portfolio Mix)

This is the actual “engine” of your financial plan. It is the specific recipe of stocks, bonds, and cash that will get you to your 25x goal.

- It is designed to maximize returns while staying within the boundaries of the Risk Assessment you did in Step 7.

- You deploy this allocation the moment you begin moving money into your brokerage or retirement accounts.

- However, it is not “set it and forget it.”

- The Shift (Glide Path):

- Early Career: You deploy an Aggressive mix to capture growth.

- Mid-Career: You move toward Moderate to protect some of your gains.

- Near Retirement: You shift to Conservative to ensure a market crash the year before you retire doesn’t slash your “25x number” in half.

Your Asset Allocation is built at the intersection of:

- Risk Capacity: Your mathematical ability to weather losses based on time horizon.

- Risk Tolerance: Your psychological ability to handle volatility.

- Portfolio mixes should shift from aggressive (80–95% stocks) to conservative (20–40% stocks) as you approach your target retirement date.

- Aggressive (15+ yrs to retirement): 80%–95% Stocks / 5%–20% Bonds.

- Moderate (5–12 yrs to retirement): 50%–75% Stocks / 25%–50% Bonds.

- Conservative (Near/At retirement): 20%–40% Stocks / 60%–80% Bonds

Key Takeaway: Asset allocation is the bridge between your current savings and your future target.

You build it now to ensure your money is working hard enough to beat inflation, but safely enough to be there when you need it.

Table: Financial Plan Phase 2: Goal and Risk Analysis and Investment Allocation Design

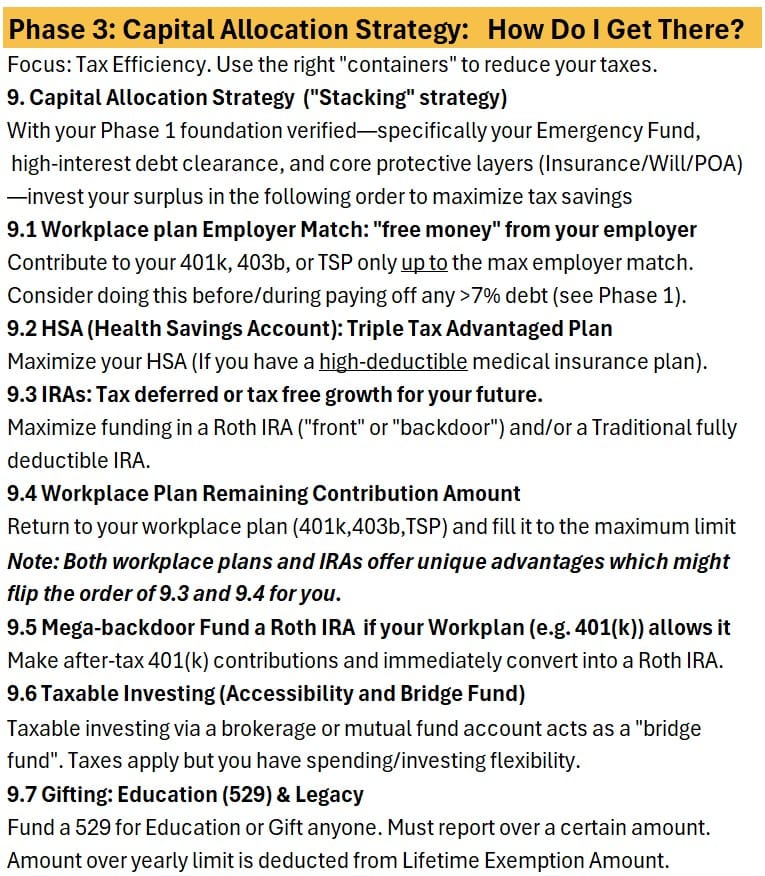

Financial Plan: Phase 3: Capital Allocation Strategy

Goal:

Tax Efficiency. Use the right “containers” to reduce your lifetime tax bill.

Maximize tax efficiency through “stacking.”

To optimize every dollar, assets should be deployed into specific “containers” starting with the order provided below.

See my post Tax Advantaged Plans and Other Capital Allocation Structures for more details on the various legal and tax related containers (wrappers, buckets, entities, vehicles) available to you.

Our focus here is Tax Efficiency. Use the right “containers” to reduce your taxes.

9. The “Stacking” Strategy (Order of Operations)

The goal here is Tax Arbitrage: paying the least amount of tax possible by choosing the right “container” for your money.

With your Phase 1 foundation verified—specifically your Emergency Fund, high-interest debt clearance, and core protective layers (Insurance/Will/POA)—invest your surplus in the following order to maximize tax savings

9.1 Employer Match

- Contribute to 401k/403b/TSP up to the match limit (Free Money).

- This is an immediate, guaranteed 100% return on your investment.

- The Logic: No other investment—and very few debts—can consistently beat “free money.”

- Even if you have a loan at 7%, the 100% gain from a match effectively “outruns” the interest you’re paying.

At this point, plan on contributing exactly what is needed to get the full match but not more (because every dollar beyond might be better spent elsewhere in the stack first)

9.2 HSA (Health Savings Account)

- Maximize your HSA (If you have a high-deductible medical insurance plan).

- The HSA is the only “Triple Tax Advantaged” account in existence.

- Tax-free going in: Contributions lower your taxable income today.

- Tax-free growth: You pay $0 in taxes on capital gains or dividends while the money grows.

- Tax-free coming out: As long as it’s used for medical expenses (now or 30 years from now), you never pay a cent in tax.

- It is effectively “super-powered” compared to a 401(k) or IRA.

9.3 IRAs (Roth and/or Traditional)

- Maximize for tax-free growth.

- The Roth is often (but not always) the superior choice over a Traditional IRA for long-term flexibility.

- Roth IRAs often offer better investment flexibility than workplace plans.

- Most workplace plans (401ks) have limited, sometimes expensive fund choices.

- An IRA at a firm like Vanguard or Fidelity lets you buy almost anything with near-zero fees.

- The “Roth” Advantage: If you expect to be in a higher tax bracket later, paying taxes now (Roth) lets you lock in a lifetime of tax-free growth.

- The “Traditional” Advantage: If you are in a high tax bracket now, a deductible IRA provides an immediate tax break to help you save more.

9.4 Workplace Plan Remainder

- Once your match and IRA are maxed, return here to shield more income from the IRS.

- Return to your 401k/TSP and fill to the IRS maximum limit.

- If you still have investable cash, the 401(k)/403b/TSP provides a massive “tax bucket” ($23,500+ limit) to lower your current tax bill or build a massive tax-free Roth nest egg.

- If your Workplan offers enough flexibility at low cost, you could flip the order of 9.3 and 9.4

9.5 Mega Backdoor Roth if your Workplan (e.g. 401(k)) Allows it

- This is an “advanced maneuver” to get massive amounts of money into a Tax-Free Roth status.

- If your plan allows “after-tax” contributions, you can

- effectively bypass the standard $7,500 (for 2006) IRA limit and

- move tens of thousands more into a Roth environment where it will never be taxed again.

9.6 Taxable Investing (The Flexibility Stack)

This is your “Accessibility & Bridge Fund.”

While the previous steps focused on tax-sheltered accounts that often restrict your money until age 59½, taxable investing provides total liquidity.

- This step is about building wealth that is available to you at any time, for any reason

- whether that’s retiring early, starting a business, or making a major lifestyle purchase before reaching retirement age.

- Unlike IRAs, you pay taxes on dividends and realized capital gains along the way.

- However, this is the “price of admission” for having no age restrictions or withdrawal penalties.

- This can be executed through a standard brokerage account, directly with mutual fund companies, or via other taxable security platforms.

- To minimize the tax drag, investors typically use “tax-efficient” assets here

- like total market index funds or municipal bonds rather than high-turnover funds that create large annual tax bills.

9.7 Gifting & Legacy

Now you are ready to move wealth to the next generation without the IRS taking a cut.

- Education (529): Money grows tax-free specifically for school.

- It’s like an IRA, but for tuition.

- Estate Planning:

- By gifting money now, you reduce the size of your future taxable estate.

- The “Lifetime Exemption” is massive, but reporting gifts over the annual limit (e.g., $18,000) ensures the IRS tracks your total “wealth transfer” over time.

Summary

We follow this order because we want to

- capture guaranteed gains (Match) first,

- perfect tax efficiency (HSA) second,

- low-cost flexibility (IRA) third, and

- long-term volume (401k) fourth.

Only after those “tax shelters” are full (or optimized) do we move to the “Taxable Investing” or “Gifting and Legacy” steps.

See my article Tax Advantaged Plans and Other Capital Allocation Structures for much more on the various types of containers available.

Table: Financial Plan Phase 3: Capital Allocation Strategy

Financial Plan: Phase 4: Execution & Maintenance

Objective:

Disciplined execution and automation.

Strategy fails without a repeatable process.

Utilize low-cost Index Funds (targeting expense ratios near 0.05%) to achieve instant diversification.

- Automation: Set recurring transfers of your monthly surplus to trigger on payday.

- Inflation Scaling: Increase contributions by 3% annually to maintain purchasing power.

- Behavioral Governance: Establish a “Behavioral Contract” to prevent emotional selling during market volatility and restrict portfolio reviews to a quarterly basis.

10. The Engine (Index Funds)

Buy low-cost Index Funds/ETFs (like the S&P 500 or Total Stock Market).

You shouldn’t pick your investments until you know where they are going and what they are for.

Phases 2 and 3 established your goals and your tax strategy.

Step 10 is the tactical execution.

- It’s the difference between choosing a destination (Phase 2), picking the right car for the terrain (Phase 3), and finally choosing the fuel (Step 10) to make it move.

- By choosing broad Index Funds/ETFs, you eliminate the need for complex stock picking.

- Index funds allow you to simply buy the entire haystack.

- Instead of betting on one company, you own hundreds or thousands.

- If one fails, the others carry the weight.

- Now that you’ve opened your Roth IRA or 401(k), the Index Fund is the “set it and forget it” tool that actually generates the growth required to hit your 25x target.

- High-quality index funds are the most efficient way to capture the “market return” discussed in your Risk Assessment (Step 7) without the overhead of high fees or the risk of individual company failure.

- High fees are “silent killers” of wealth.

- A 0.50 % fee might sound small, but over 30 years, it can eat hundreds of thousands of dollars in potential growth.

- Low-cost funds ensure the market’s returns stay in your pocket, not the fund manager’s.

11. Automate Everything

Automate everything you can to remove decision fatigue and human error from your wealth building.

- The Discipline Gap: If you have to manually move money every month, you eventually won’t. Automation turns “saving” from a choice into a default.

- The Inflation Adjustment: Because $1,000 today won’t buy $1,000 worth of goods in a decade, increasing your contributions by 3%–5% annually ensures your savings rate keeps pace with the rising cost of living.

- Rebalancing: Over time, “winners” in your portfolio (like stocks) will grow faster than “safer” assets (like bonds), making your portfolio riskier than you intended. Rebalancing forces you to “sell high and buy low,” resetting your risk to its proper level.

12. The Behavioral Contract (Panic Rules)

Step 12 is about insuring your plan against your emotions, creating a written set of rules that prevents you from making impulsive, reactive decisions during market volatility.

- Your greatest enemy isn’t the market; it’s your own brain.

- The Psychology: In a crash, your survival instinct screams “Sell!” to stop the pain.

- A written contract acts as a “circuit breaker” for your emotions.

- Quarterly Checking: The market is “noisy” daily but “signal-heavy” yearly.

- Checking too often leads to tinkering, and tinkering usually leads to lower returns.

- The Commitment: By signing a contract with yourself, you move from being a “speculator” reacting to news to a “systematic investor” executing a long-term plan.

- Write down your “Rules of Engagement”:

- “I will not sell during a market drop.”

- “I will only check my balance sheet quarterly.”

- “I will stick to my 25x goal.”

- etc.

I may have browsed over the following comment, but I thought it important to mention that term life insurance should be considered when others depend on you for financial reasons and/or stability vs a single person. Hopefully this is self explanatory. Additional details could be mentioned as to the amount of term life insurance you need, but for now, simply research this topic and customize accordingly. Overall article is a solid basis or guideline.

Thanks man. I added a linked appendix 3 describing the basics of term life and also umbrella policies.