The Strategic Hierarchy of Retirement Funding

Choosing between a Traditional and a Roth IRA is a decision between Theoretical Optimization and Functional Control.

While a spreadsheet might suggest a Traditional IRA “wins” through tax-bracket arbitrage, those mathematical victories rely on two assumptions that rarely survive real life:

- that you will meticulously reinvest every penny of your current tax savings, and that

- future tax laws, Social Security rules, and Medicare surcharges will remain static.

Because your total IRA contribution limit is a combined $7,500 ($8,600 if age 50+), you cannot “do it all.”

To navigate this effectively, we follow a specific Universal Sequential Strategy designed to capture every available benefit in the correct order:

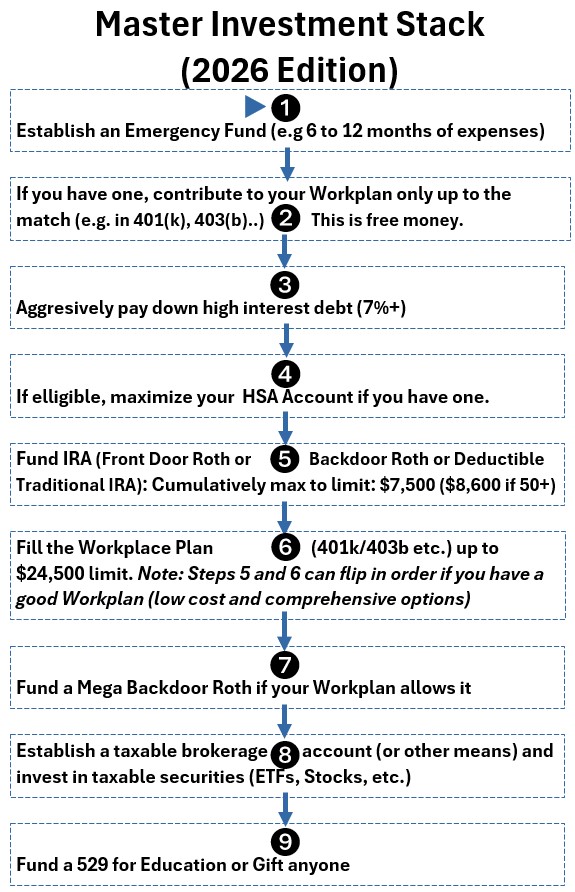

The Master Investment Stack (2026 Edition)

Before you start thinking about how to allocate your assets (i.e. invest etc.), you need to make sure you are following some kind of orderly , sequential financial plan.

You should read my post: Your Wealth Plan: 4 Steps to Financial Freedom to help you with this.

Before you start thinking about how to invest in IRAs (or any other type of investment) you really should have established Phase 1 and Phase 2 which require you to fully understand your financial status, define your tolerance for risk, and establish you short and long term financial goals.

As part of phase 1 for example, you should have already established or begun to develop plans for the following

- A 6 month to 1 year emergency fund

- Paying down high interest debt

- Protecting your foundation with the proper Insurance, Will, and Power/s of Attorney.

After you have completed phase 1 and phase 2 of your financial plan you can start on phase 3: Capital Allocation Strategy (AKA Master Investment Stack or Order of Operations).

Chart: Master Investment Stack (Order of Operations)

I cover this more in my post: Master Investment Stack (Order of Operations)

- Establish an Emergency Fund:

- We should have this set up already from Phase 1 of your financial plan.

- Secure 6 to 12 months of living expenses in a high-yield savings account before proceeding with any investments.

- Capture the Employer Match

- Contribute to your 401(k), 403(b), or TSP exactly up to the match limit to secure an immediate, guaranteed 100% return.

- Eliminate High-Interest Debt:

- You should have already starting thinking about this in Phase 1 of your financial plan

- but I am intentionally placing here after you capture your employers free money match

- Aggressively pay down any debt with an interest rate of 7% or higher to secure a guaranteed return equal to the interest saved.

- You should have already starting thinking about this in Phase 1 of your financial plan

- Maximize Health Savings Account (HSA):

- Fully fund your HSA to take advantage of the only “triple tax-advantaged” vehicle, offering tax-free contributions, growth, and withdrawals for medical costs.

- Fund an IRA (Roth and/or Traditional):

- Maximize your annual IRA contributions to access better investment flexibility and lower fees than most workplace plans.

- Fill the Workplace Plan:

- Return to your employer-sponsored plan (401(k)/403(b)) to shield more income from taxes once your IRA and match are fully utilized.

- Steps 5 and 6 could be flipped depending on the quality (flexibility, cost, etc.) of your 401(k) or other workplace plan

- Execute the Mega Backdoor Roth:

- If your employer plan allows after-tax contributions, use this advanced strategy to move significantly more capital into tax-free Roth status.

- Invest in Taxable Accounts:

- Utilize a standard brokerage account for “overflow” capital to build a liquid bridge fund accessible at any age without withdrawal penalties.

- Legacy and Low-Interest Debt:

- Direct remaining funds toward 529 education plans, estate gifting, or paying down low-interest liabilities like a mortgage.

The Step 5 Decision: Traditional vs. Roth

When you reach Step 5, your move is determined by whether you (or your spouse) are covered by a plan at work.

This is where the decision trees become your tactical guide:

Scenario A:

- No Workplace Plan.

- You are eligible for a Full Traditional Deduction regardless of income.

- You must decide if you want the immediate refund or if you prefer the tax-free growth of a Roth.

Scenario B:

- You ARE Covered by a Plan.

- You must use the 2026 MAGI Limits to determine your move.

- If your income is above $81,000 (Single) or $129,000 (Joint), the Traditional deduction begins to vanish.

In these cases, the Roth IRA (or Backdoor Roth for high earners) becomes the mathematically superior choice to avoid the “tax trap” of non-deductible contributions.

Step 7 Decision (Mega Backdoor Roth)

If you have remaining funds to invest and you have a workplace plan, consider the Mega Backdoor Roth.

We provide a decision tree for this option as well.

Critical Reminders Before Using the Trees

As you navigate the tactical trees below, keep these three “Hidden Drivers” in mind:

The Behavioral Reality:

- Traditional IRAs only “win” if the tax refund is reinvested.

- If it’s spent on lifestyle, the Roth IRA wins by default.

The Benefit Poisoning:

- Traditional IRA withdrawals are “loud” income—

- they can trigger taxes on your Social Security and

- hike your Medicare (IRMAA) premiums.

- Roth withdrawals are “silent.”

Administrative Cleanliness:

- The Roth IRA is the ultimate tool for simplicity.

- It eliminates the Pro-Rata rule landmine,

- bypasses Required Minimum Distributions (RMDs), and

- protects surviving spouses from the “Widow’s Penalty” (bracket squeeze).

Use the Decision Trees in this Post for Step 5 and Step 7 of the Master Stack

In the following sections we’ll take a closer look at IRAs and present detailed decision trees to determine your Steps 5 and 7.

They will help you decide your options

- under the $7500 (2006) max contribution limit Standard IRAs and/or Frontdoor/Backdoor Roths and

- under a much larger max contribution limit for the Mega Backdoor Roth.

We’ll start with a little history first.

Traditional IRAs and Roth IRAs

First rolled out in 1974, IRAs (Individual Retirement Accounts) were designed to give individuals personal control over their retirement security.

Today, they remain the two most popular tools for independent saving, distinguished primarily by their tax structure.

Traditional IRA

- You contribute dollars that may be tax-deductible depending on your income and whether you have a workplace retirement plan.

- If eligible, it lowers your taxable income today;

- if not, you are making “non-deductible” contributions.

- Your investments grow tax-deferred, but

- you will pay ordinary income tax on all withdrawals during retirement.

- You contribute dollars that may be tax-deductible depending on your income and whether you have a workplace retirement plan.

Roth IRA

- You contribute after-tax dollars, so there is no immediate tax break (no deductions).

- In exchange, your investments grow tax-free, and

- qualified withdrawals in retirement are completely exempt from federal taxes.

The IRA: History

The Individual Retirement Account (IRA) was born out of a crisis of confidence.

In the early 1970s, high-profile corporate pension failures—most notably the collapse of the Studebaker-Packard motor company—left thousands of workers with nothing after decades of service.

In response, Congress passed the Employee Retirement Income Security Act (ERISA) of 1974.

Signed into law on Labor Day by President Gerald Ford, ERISA created the “Traditional IRA” to give workers a way to save for retirement independently of their employers.

The Evolution of the “Bucket”

For fifty years, the IRA has evolved from a simple safety net into a sophisticated wealth-building tool.

- 1974 (The Beginning): The Traditional IRA is created.

- The official legal name used by the IRS and the 1974 legislation (ERISA) is Individual Retirement Arrangement.

- The term “Arrangement” was chosen to be broad enough to cover both bank-style accounts and insurance-style annuities.

- However, because the vast majority of people open their IRAs at banks or brokerages, “Account” became the common shorthand

- 1981 (Expansion): The Economic Recovery Tax Act makes IRAs available to all working Americans, regardless of whether they have a pension at work.

- 1997 (The Roth Revolution): Named after Senator William Roth, the Roth IRA is introduced.

![]()

- It flips the script: you pay taxes today, but the money grows and is withdrawn tax-free in the future.

- 2026 (The SECURE Era): Following the landmark SECURE 2.0 Act, the IRA has become more flexible than ever.

- There is no longer an age limit for contributions, and

- the “catch-up” limits for those over 50 are now adjusted annually for inflation to protect your purchasing power.

At its core, the IRA is your personal tax-sheltered “container.”

While 401(k)s and other workplace plans are tied to your job, the IRA is tied to you.

It is the most accessible way for any individual with earned income to take control of their financial destiny.

IRA First Principles

Before diving into the “logic” of which IRA to choose, we need to establish some “first principles”.

These are the non-negotiables that the IRS applies regardless of which path (Traditional or Roth) the investor takes.

Here are the essential IRA “truths”.

1. IRAs are Individual only (No “Joint” IRAs exist)

Unlike a standard bank account or a taxable brokerage account, an IRA cannot be held as “Joint Tenants with Rights of Survivorship” or “Community Property.

- Every IRA is tied to a single Social Security number.

- You cannot add a spouse or child as a co-owner.

- The Spousal Exception (Contribution, not Ownership):

- A common point of confusion is the Spousal IRA.

- While a working spouse can fund an IRA for a non-working spouse, the account itself is still opened in only one person’s name.

- The non-working spouse is the sole legal owner of that account.

- How Couples “Jointly” Manage Them

- Since they can’t be jointly owned, couples typically use two strategies to treat them as joint assets:

- Beneficiary Designations: You name your spouse as the primary beneficiary.

- In many states (and under federal law for some plans), a spouse has an automatic right to the account unless they waive it in writing.

- Coordinated Strategy: Couples often view their separate IRAs as one “household” portfolio, balancing the investments across both accounts to hit their target asset allocation.

2. The “Single Bucket” Rule (Aggregate Limits)

Traditional IRAs and Roth IRAs DO NOT have separate limits.

- You can have several different IRA accounts at several different banks, but your total combined contribution for the year is capped at one number.

- For example, for 2026, the limits are:

- $7,500 ($8,600 if age 50+).

- You can split this $4,000/$3,500, or put it all in one, but you cannot exceed the total.

3. The “Earned Income” Floor

You cannot contribute “passive” money to an IRA. It has to be “earned income”.

- The Rule: Your contribution cannot exceed your Taxable Compensation (wages, tips, bonuses, or self-employment income).

- If you had a bad year in business and your net profit was only $3,000, your IRA contribution is capped at $3,000, even if you have $1 million sitting in a savings account.

- The Spousal IRA.

- If one spouse works and the other doesn’t, the working spouse’s income can “fund” an IRA for the non-working spouse (provided they file jointly).

4. The “Tax Year” Overlap (The April Window)

The IRA calendar doesn’t end on December 31.

- The Window: You can contribute for a tax year starting January 1 of that year all the way until the April Tax Deadline of the following year.

- Why it matters:

- From January 1 to April 15, you are in the “Overlap Zone” where you can choose which year your contribution counts toward.

- You must explicitly tell your custodian which year you are choosing.

5. The “Pro-Rata” Aggregation (The Backdoor Trap)

When the IRS looks at your IRAs for tax purposes (especially during a Roth Conversion or “Backdoor” move which we will discuss later), they don’t see separate accounts.

- The Reality:

- They see one giant “IRA Bucket.”

- If you have $90,000 in a Traditional IRA from an old 401k rollover and you try to do a $7,500 “Backdoor Roth” with new after-tax money, the IRS will tax you on ~92% of that conversion because of the existing pre-tax money.

- The Fix:

- This is why “Reverse Rollovers” (moving IRA money back into a 401k) are a prerequisite for many high-income strategies.

6. Age is No Longer a Barrier

A legacy rule used to stop people from contributing to Traditional IRAs after age 70.5.

Current Status:

- As of the SECURE Act (and confirmed in 2026), there is no upper age limit for contributions.

- As long as you have earned income, you can contribute at age 100.

9. Catch up money

You can usually add more money if you are over a certain age barrier.

- For 2026: Contribution limit = $7,500 (under 50) or $8,600 (50+)

10. Custody

To maintain the tax-advantaged status, the IRA assets must be held by a qualified trustee or custodian.

The Legal “Gatekeeper”

The IRS requires a neutral third party to act as the official record-keeper, asset safekeeper, and rule enforcer.

Who Qualifies?

These are the custodians (hold the assets and execute your trades but do not provide investment advice):

- Banks and Credit Unions

- Brokerage Firms (like Fidelity, Schwab, or Vanguard)

- Trust Companies (often used for “Self-Directed” IRAs that hold real estate or private equity)

Rules and Requirements for Funding IRAs

Navigating IRA contributions requires balancing income limits, workplace retirement plans, and tax-deductibility rules.

The following decision trees provide a step-by-step path to determine your eligibility, starting with

- Traditional IRAs,

- moving through “Front Door” Roth options, and

- concluding with “Backdoor” Roth strategies for high-income earners

Let’s start with the Traditional IRA: Check out its decision tree graphic below.

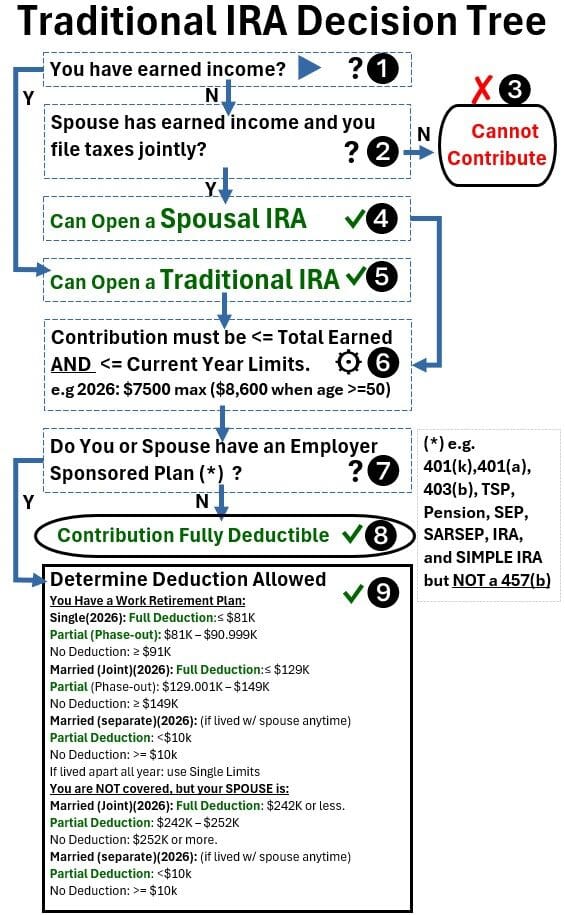

2026 Traditional IRA Decision Tree

Chart: Traditional IRA Decision Tree

2026 Traditional IRA Decision Tree

Phase 1: Eligibility & Setup

1. Do you have earned income? (Wages, tips, bonuses, self-employment)

Before looking at limits or deductions, you must pass the income test.

- The Rule: You (or your spouse, if filing jointly) must have taxable compensation.

- This includes wages, salaries, tips, and self-employment income.

- What Doesn’t Count: Passive income (dividends, interest, rental property) or Social Security benefits.

- The Spousal Loophole: If you have $0 in earned income but your spouse works, you can open a “Spousal IRA” based on their earnings, provided you file a joint return.

Yes: Go to 5.

No: Go to 2.

2. Does your spouse have earned income AND do you file taxes jointly?

- Yes: Go to 4.

- No: Go to 3.

3. Result: You cannot contribute to an IRA. (End)

4. Result: You can open a Spousal IRA (based on spouse’s income): Go to 6.

5. Result: You can open a Traditional IRA : Go to 6.

Phase 2: Contribution Limits

6. Calculate Max Contribution:

- Total must be <= Total Earned Income.

- Under Age 50: $7,500 max (2026).

- Age 50 or Older: $8,600 max (2026):

- You are eligible for the entire year if you turn 50 anytime during the year

- Note: These limits apply to the total across all your IRAs (Traditional + Roth). (see *)

Go to 7.

Phase 3: Tax Deduction Eligibility

Unlike a Roth IRA (where anyone under an income cap. can contribute), anyone with earned income can contribute to a Traditional IRA.

The “decision” in the flow chart is whether that contribution is tax-deductible.

7. Do you or your spouse have an Employer-Sponsored Plan? (see *)

- No (Neither): Go to 8.

- Yes: Go to 9.

8. Result: Contribution is Fully Deductible regardless of income. (End)

9. Determine Deduction based on Filing Status & MAGI(see *):

- The term “Partial (Phase-out)” used below means the deduction is usually reduced by $10 for every $50 (or $100 for joint) you are over the lower limit.

- If you land right in the middle of a phase-out range, you generally get roughly 50% of the deduction.

9a. YOU Have a Work Retirement Plan:

9a1. Single / Head of Household (2026):

- Full Deduction: <= $81,000

- Partial (Phase-out): $81,001 – $90,999

- No Deduction: >= $91,000

9a2. Married (Joint Filing) (2026):

- Full Deduction: <= $129,000

- Partial (Phase-out): $129,001 – $148,999

- No Deduction: >= $149,000

9a3. Married (Separate)(2026):

- If lived w/ spouse anytime: Partial < $10,000; No Deduction >= $10,000.

- If lived apart all year: Use Single Limits ($81,000 – $91,000).

9b. You are NOT covered, but your SPOUSE is:

9b1. Married (Joint)(2026):

- Full Deduction: <= $242,000

- Partial (Phase-out): $242,001 – $251,999

- No Deduction: >= $252,000

9b2. Married (Separate)(2026):

- If lived w/ spouse anytime: Partial < $10,000; No Deduction >= $10,000.

- If lived apart all year: Full Deduction (No income limit).

End of Decision Tree

The “Double-Dip” Window

The “IRA Season”

- Eligibility for any tax year runs from January 1 of that year until the tax filing deadline (typically April 15) of the following year.

The Opportunity

- From January 1 to April 15, you are in the “Double-Dip” window.

- During this time, you can make a contribution for the previous tax year and a separate contribution for the current tax year simultaneously.

Critical Step

- When contributing during this window, you must specify to your broker which tax year the money is for, or they will default it to the current calendar year.

(*) Definitions & Fine Print

Employer Plans: Includes 401(k), 403(b), SEP-IRA, SIMPLE IRA, and Pension plans.

The 457(b) Exception

- Participation in a 457(b) plan does not count as being “covered” by a retirement plan for these deduction limits.

MAGI

- This stands for Modified Adjusted Gross Income. It is your AGI with certain deductions (like student loan interest) added back in.

Even if you get “No Deduction” in Step 9, you can still contribute to a Traditional IRA (up to the limits in Step 6); you just don’t get the tax break today.

In that case, many people look into the “Backdoor Roth” strategy.

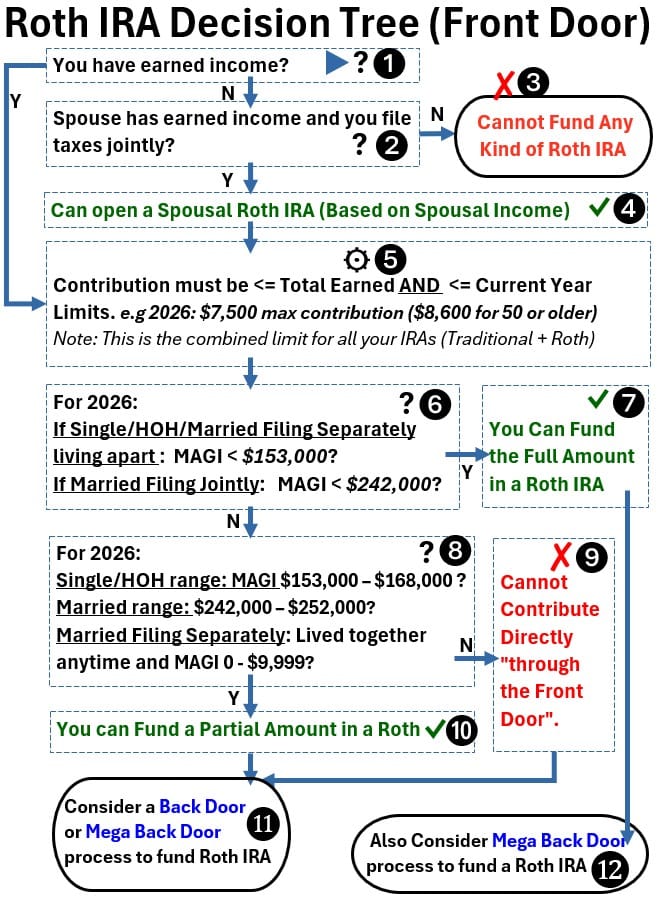

Front Door Roth IRA Decision Tree (2026)

The primary hurdle for a Traditional IRA decision tree is the “deductibility wall,” where high earners covered by a workplace plan quickly lose the ability to write off contributions.

Conversely, a Roth IRA decision tree operates with much wider income gates, making it a more accessible “front-door” option for those who have already been phased out of traditional tax deductions.

So let’s run through a Roth front door decision tree.

Front Door Roth IRA decision Tree (2026)

Phase 1: Eligibility & Setup

1. Do you have earned income? (Wages, tips, bonuses, self-employment)

Before looking at limits or deductions, you must pass the income test.

- The Rule: You (or your spouse, if filing jointly) must have taxable compensation.

- This includes wages, salaries, tips, and self-employment income.

- What Doesn’t Count: Passive income (dividends, interest, rental property) or Social Security benefits.

- The Spousal Loophole: If you have $0 in earned income but your spouse works, you can open a “Spousal IRA” based on their earnings, provided you file a joint return.

No: Go to 2.

Yes: Go to 5.

2. Does your spouse have earned income AND do you file taxes jointly?

No: Go to 3.

Yes: Go to 4.

3. Result: You cannot contribute to an IRA. (End)

4. Result: You can open a Spousal Roth IRA (based on spouse’s income). Go to 5.

5. Check Contribution Limits:

This is the “ceiling” for how much cash can actually enter the account.

- Total must be <= Total Earned Income.

- Under Age 50: $7,500 max.

- Age 50 or Older: $8,600 max ($7,500 + $1,100 catch-up).

- Note: This is the combined limit for all your personal IRAs (Traditional + Roth).

Go to 6.

Phase 2: The “Front Door” Income Test (2026 MAGI)

6. Are you eligible for a FULL Front Door contribution?

- Single / Head of Household / MFS (Lived APART all year): Is MAGI < $153,000?

- Married Filing Jointly: Is MAGI < $242,000?

If YES to either: Go to 7.

If NO to either: Go to 8.

7. Result: Front Door. You can fund the full amount directly into a Roth IRA. Go to 12.

Phase 3: The Phase-Out Test

8. Are you in the Partial Contribution range?

- Single / HOH: $153,000 – $167,999?

- Married Filing Jointly: $242,000 – $251,999?

- Married Filing Separately (Lived together anytime): $0 – $9,999?

Yes: Go to 10.

No: Go to 9.

9. Result: You cannot contribute through the “Front Door.” Go to 11.

10. Result: You can fund a Partial Amount directly. Go to 11 for the remaining balance.

Phase 4: Strategy & Advanced Funding

11. Strategy

- Consider a Backdoor Roth IRA (non-deductible Traditional contribution → Roth conversion) or

- a Mega Backdoor Roth (if your 401k allows after-tax contributions).

(End)

12. The “Stacking” Rule:

- Even if you use the “Front Door” for your $7,500 (or $8,600) IRA limit, you should also consider the Mega Backdoor process via your employer plan if you have additional savings goals.

- These are separate buckets and can be utilized simultaneously.

(End)

End of Decision Tree

Go to Menu

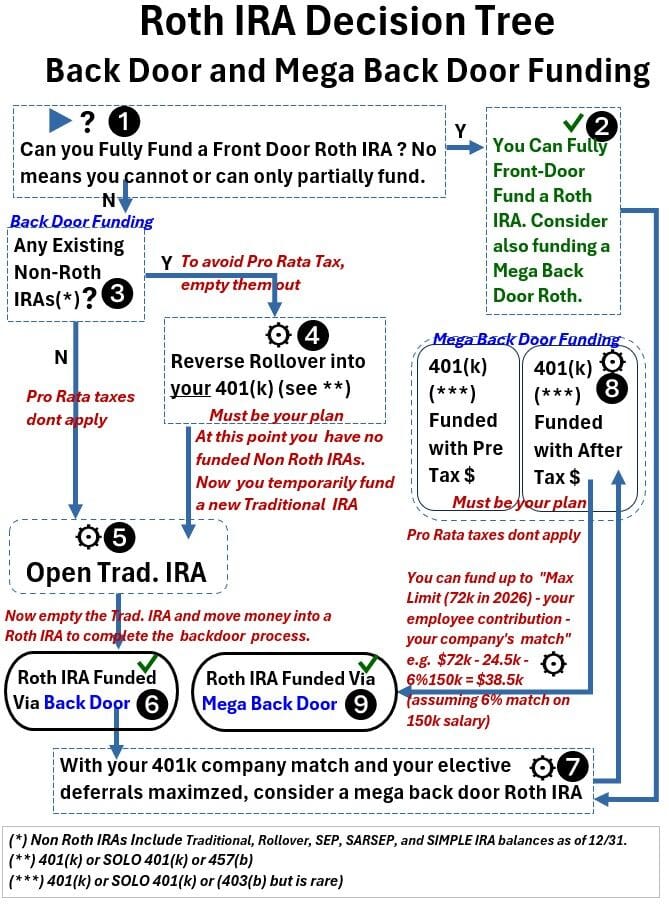

Back Door and Mega Back Door Roth IRA Decision Tree

When the “front door” closes due to rising income, the decision tree doesn’t stop—it just shifts to the Backdoor Roth IRA.

This is a simple two-step maneuver where you bypass income limits by making a non-deductible contribution to a Traditional IRA and immediately converting it to a Roth.

However, if you are looking to move “mega” amounts of capital—far beyond the standard $7,500 limit—the tree branches toward the Mega Backdoor Roth.

This strategy relies on your employer’s 401(k) plan specifically allowing after-tax contributions and in-service distributions, potentially unlocking an additional $40,000+ in annual Roth savings

Chart: Roth IRA Decision Tree (Back Door and Mega Back Door Process)

The 2026 Backdoor & Mega Backdoor Decision Tree

1. Regarding a Front Door Roth (FDR): Can you fund it fully?

Yes: Go to 2.

No (or Partial): Go to 3.

2. Direct Path: You can fully fund a Roth IRA via the “Front Door.”

Action: Deposit up to $7,500 ($8,600 if 50+).

Next: Consider additional tax-free growth.

Go to 7.

3. Check for “Pro-Rata” Obstacles: Do you have any existing pre-tax (Non-Roth) IRAs? (see (*))

No: Go to 5. (Backdoor will be 100% tax-free).

Yes: Go to 4.

4. The “Cleanup” Step: Can you perform a Reverse Rollover? (see (**))

Action: Move pre-tax IRA balances into your current 401(k) to “hide” them from the IRS Pro-Rata calculation.

Note: This must be completed by 12/31 of the contribution year.

Go to 5.

5. Start the Backdoor Process: Open a Traditional IRA.

Action: Make a non-deductible contribution ($7,500 / $8,600).

Go to 6.

6. Complete the Backdoor: “Convert” or “Empty” the Traditional IRA into your Roth IRA.

Result: Since you have no pre-tax IRA balance (Step 3 or 4), this conversion is tax-free.

Go to 7.

7. Shift to the Employer Bucket: Are your 401(k) elective deferrals ($24,500) and company match maximized?

Yes: Go to 8.

No: Maximize these first, then Go to 8.

8. The Mega Backdoor (MBDR): Check if your 401(k) allows After-Tax contributions and In-Service Distributions/Conversions.

Yes: Use the “After-Tax” feature to fund your Roth IRA/401(k).

Rule: Pro-Rata taxes do not apply here (401k buckets are isolated from IRA buckets).

Go to 9.

9. Calculate the Remaining MBDR Space:

Formula: $72,000 (2026 Limit) — [Your Elective Deferral] — [Company Match] = Your MBDR Space.

Example: $72,000 — $24,500 — $9,000 (6% of 150k) = $38,500 available for MBDR.

End of Decision Tree

Reference Legend

(*) Non-Roth IRAs: Includes Traditional, Rollover, SEP, SARSEP, and SIMPLE IRA balances as of 12/31. (Does not include 401k/403b).

(**) Reverse Rollover: Moving IRA money into a 401(k), Solo 401(k), or 457(b).

Age 50+ Note: If you are 50 or older, your IRA cap is $8,600 and your Total 401(k) cap is $80,000 ($72,000 + $8,000 catch-up).