Introduction

You might be focusing on what you are investing in—like a specific stock, bond, rental property, etc.

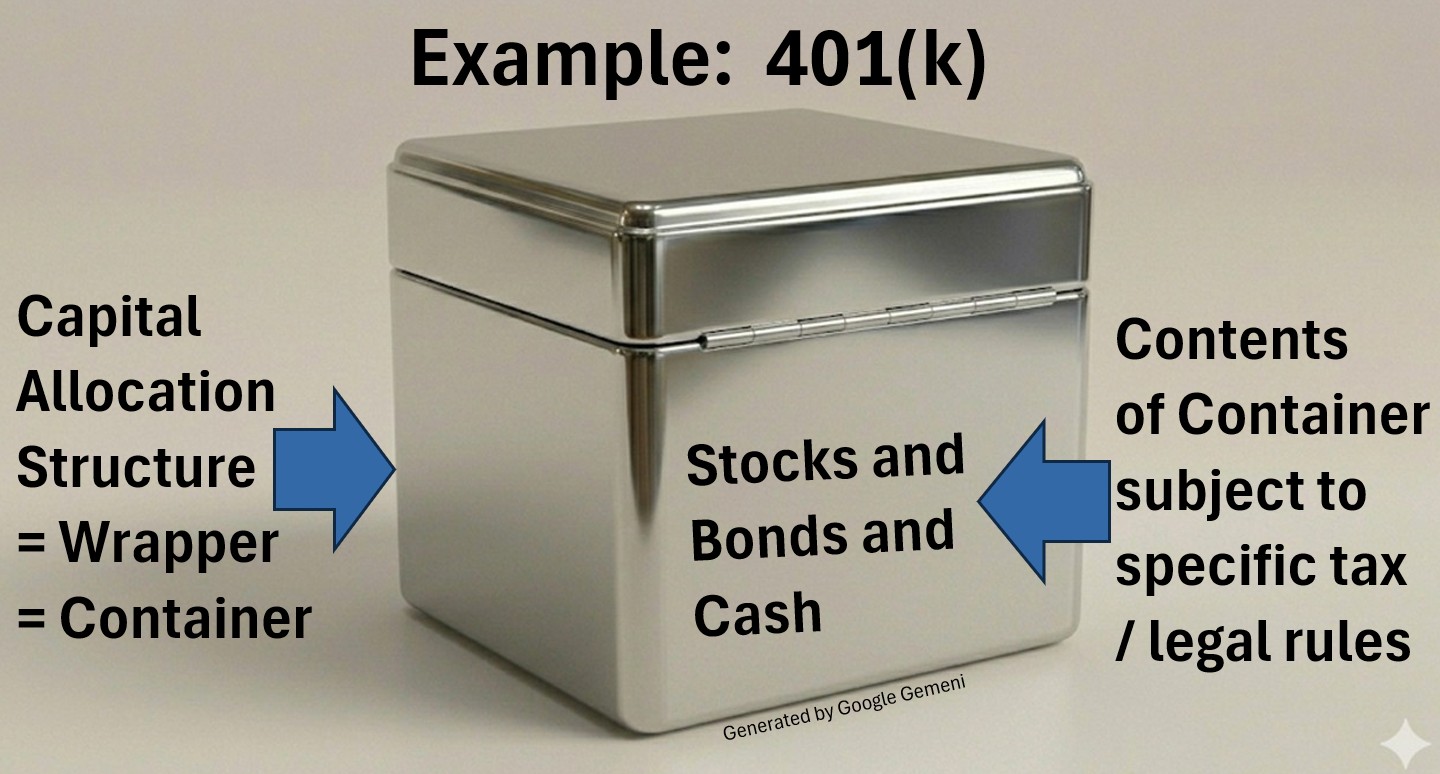

But, the “container” you put that investment in is often more important than the investment itself.

Capital Allocation Structures

A capital allocation structure is the legal and tax framework—often called a wrapper, container, or bucket—that houses an asset.

While the asset itself (like a stock or property or business) generates the return, the structure defines the “rules of engagement” for that asset.

Specifically, it dictates three things:

- Taxation: When and how the government takes a cut (e.g., tax-deferred, tax-free, or taxable).

- Asset Protection: Whether the money is shielded from creditors, lawsuits, or the bankruptcy of your employer.

- Governance: Who owns the asset, who controls it, and the legal process for moving or withdrawing the funds.

So, think of your assets as the “stuff” and the “capital allocation structures” as the containers you pack the stuff into (and which now dictate their tax and legal treatment).

Picture: The Capital Allocation Structure is the Legal/Tax Defined Container which holds your Capital

The Inventory of Containers

We will categorize the primary legal and tax frameworks available today, including:

- Qualified Containers: Assets held in a trust, 100% separate from your employer’s balance sheet (e.g. 401(k), TSP).

- Statutory Containers: Accounts governed by specific IRS laws, like IRAs and 403(b)s.

- Non-Qualified Containers: “Unsecured promises” where the money stays on the company’s books, meaning you are a creditor if they go under.

- Benefit & Entity Containers: Specialized shells for healthcare (HSA), education (529), or business liability (LLC, S-Corp).

The Filling (Stacking) Order (Scenarios)

Not all containers should be filled at the same time.

We will run through scenarios for individuals and couples to show maximum funding capacities and most efficient order of operations—identifying which containers to fill first to maximize tax breaks and employer matches.

Nesting the Containers

The most effective strategies often involve “nesting”—placing one container inside another.

For example, you might place a business defined as an LLC “inside” a Trust (i.e. the trust wraps around the LLC).

This layering creates a “corporate veil” for asset protection (and privacy) while optimizing how money flows to your personal bottom line.

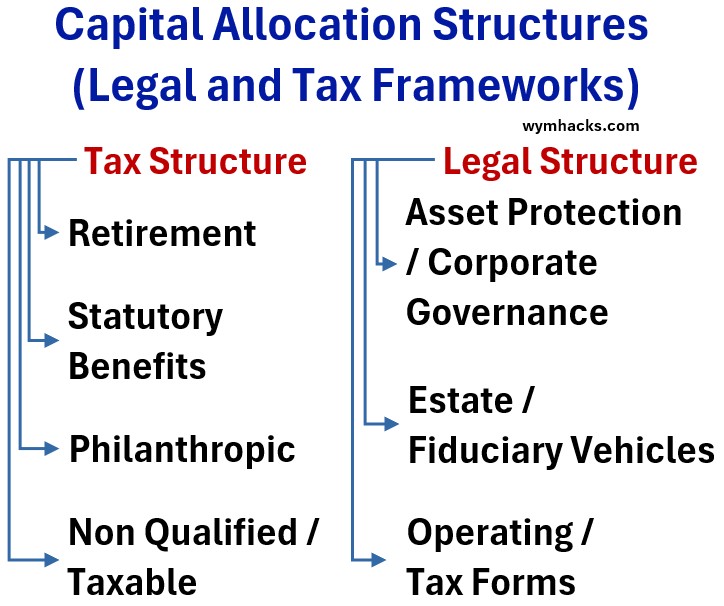

Capital Allocation Structure (Containers, Wrappers) Organization Charts

- the Tax Environment (how the IRS views your money) and

- the Legal Environment (how the law views your ownership).

Chart_1 is a high level sketch and Chart_2 provides a little more detail under each category.

Chart_1 Capital Allocation Structures (Legal And Tax Frameworks)

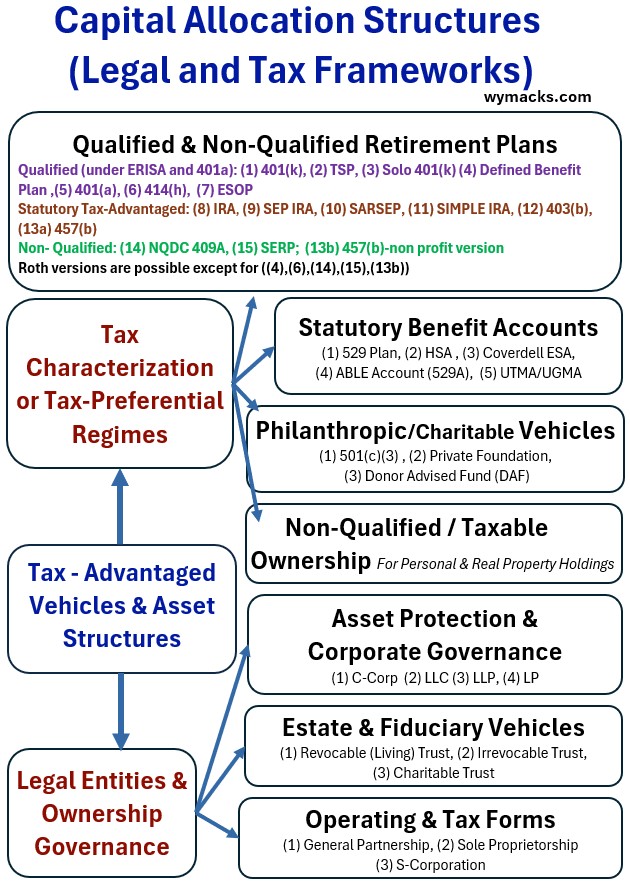

Chart_2 Capital Allocation Structures (Legal And Tax Frameworks) – Detailed

Pillar_1: Tax Characterization or Tax-Preferential Regimes

This section of the chart identifies the “tax DNA” of your money.

It categorizes containers based on their specific relationship with the IRS, moving from

- highly regulated Qualified and Statutory plans—which offer the most aggressive tax breaks—to

- Non-Qualified and Taxable ownership, which offer fewer incentives but significantly more flexibility and liquidity.

- By separating these into regimes (Retirement, Benefit, and Philanthropic), the chart helps you identify which tax “shield” is best suited for a specific dollar of income.

Pillar_2: Legal Entities & Ownership Governance

While the first pillar deals with taxes, this pillar deals with Asset Protection and Control.

It defines the legal “skeleton” that supports your tax containers.

This section moves from

- Corporate Governance (shielding your personal life from business liabilities) to

- Estate and Fiduciary Vehicles (managing how control shifts over time or through generations).

The inclusion of Operating & Tax Forms serves as the vital link between these two pillars, dictating how income legally flows from a business entity into a specific tax container.

Let’s analyze each section a little closer.

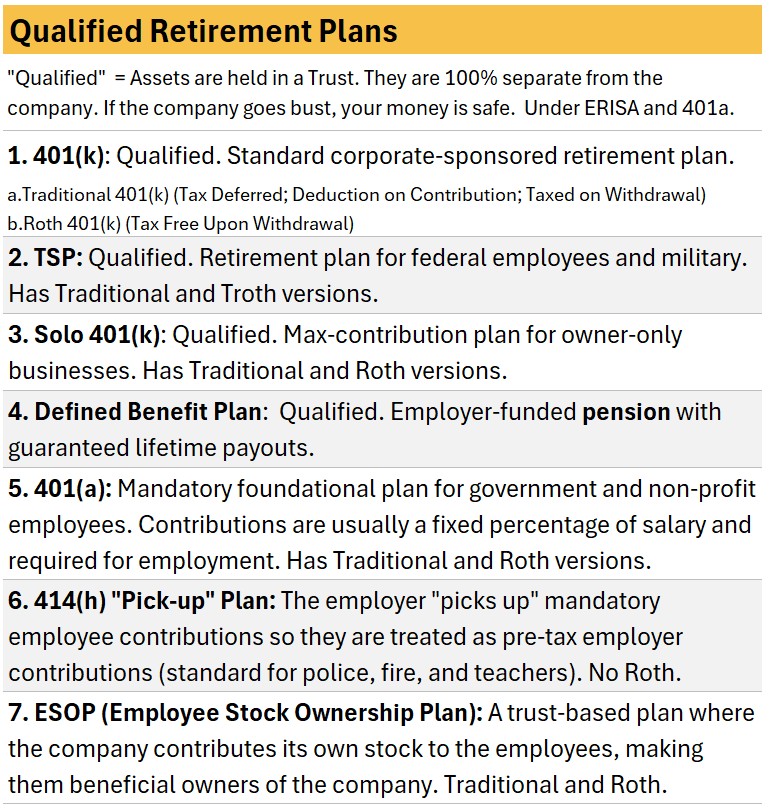

Capital Allocation Structures: Qualified and Statutory Retirement Plans

Qualified Retirement Plans

These “Qualified” plans are governed by ERISA and Section 401(a) if the IRS code.

- ERISA stands for the Employee Retirement Income Security Act of 1974.

Assets are held in a third-party trust, legally separating them from the employer’s balance sheet.

This structure provides the highest level of federal asset protection;

- if the sponsoring company fails, the plan assets remain shielded from corporate creditors.

Table_1 Qualified Retirement Plans

1. 401 (k)

- The standard corporate retirement vehicle.

- Offers Traditional (pre-tax) or Roth (after-tax) contribution paths.

- I’ll provide a little more information on “Traditional” vs Roth in the next section

2. TSP

- TSP stands for Thrift Savings Plan.

- The federal government and military version of a 401(k),

- providing identical Traditional and Roth options.

3. Solo 401(k)

- A high-capacity plan designed for owner-only businesses or 1099 contractors with no employees.

- Supports both Traditional and Roth deferrals.

4. Defined Benefit Plan

- A traditional pension model.

- It is employer-funded and provides a formulaic, guaranteed lifetime payout to the participant.

5. 401(a)

- Mandatory foundational plan for government and non-profit employees.

- Contributions are usually a fixed percentage of salary and required for employment.

6. 414(h)

- “Pick-up” Plan

- The employer “picks up” mandatory employee contributions so they are treated as pre-tax employer contributions (standard for police, fire, and teachers).

7. ESOP

- ESOP = Employee Stock Ownership Plan

- A trust-based plan where the company contributes its own stock to the employees, making them beneficial owners of the company.

Traditional vs Roth

The plans described above have Traditional and Roth versions.

Let’s explore what these mean.

The Traditional Label (Tax-Deferred)

The “Traditional” label is built on the concept of tax deferral.

How it works:

- You receive an immediate tax deduction today, which lowers your current taxable income.

- If you contribute $10,000 to a Traditional 401(k), the IRS acts as if you never earned that money this year.

The Trade-off:

- You are essentially “kicking the tax can down the road.”

- While the money grows without being taxed annually, the IRS becomes a silent partner in your account.

- When you eventually withdraw the funds in retirement, the entire amount (both your original contribution and all the growth) is taxed as ordinary income at whatever the tax rates are at that time.

The Roth Label (Tax-Free)

Roth is not an acronym.

It is named after Senator William Roth of Delaware, the legislative sponsor who created the Roth IRA in 1997 to provide a “tax-free” alternative for middle-class savers.

How it works:

- You pay your taxes upfront.

- There is no immediate tax deduction; you contribute “after-tax” dollars.

The Benefit:

- Because you have already “settled up” with the IRS, the money grows entirely tax-free.

- When you reach retirement, every dollar you withdraw—including decades of compounded investment gains—is 100% tax-free.

The Strategic Edge:

- By choosing the Roth label, you are essentially “buying out” the IRS’s future ownership of your wealth.

Ok , let’s continue with statutory retirement plans.

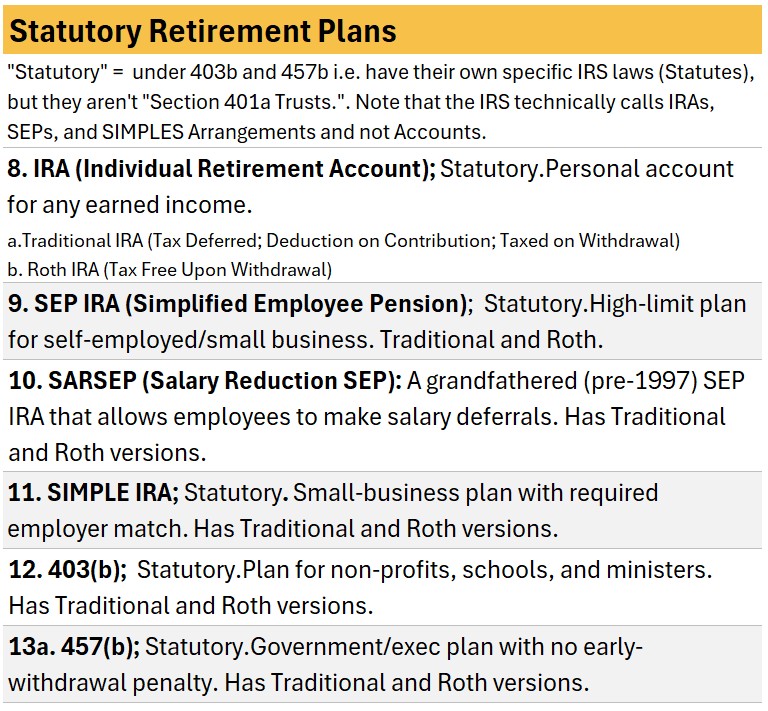

Statutory Retirement Plans

“Statutory” plans are created by specific IRS statutes (such as 408, 403(b) or 457(b)) rather than the 401(a) trust framework.

While they offer robust tax advantages, they are legally classified as “arrangements” rather than trust-held accounts.

Table_2 Statutory Retirement Plans

8. IRA (Individual Retirement Account)

- An individual arrangement for anyone with earned income.

- Available in Traditional (deductible) or Roth (tax-free withdrawal) formats.

9. SEP IRA

- This is an employer-sponsored workplace plan.

- It functions as a 401(k) “light” version rather than like personal savings account (Traditional or Roth IRA).

- SEP stands for Simplified Employee Pension

- A simplified plan for the self-employed or small business owners.

- Contributions are employer-funded and can be made to Traditional or Roth SEP accounts.

10. SARSEP

- This is an employer-sponsored workplace plan.

- It functions as a 401(k) “light” version rather than like personal savings account (Traditional or Roth IRA).

- SARSEP = Salary Reduction SEP

- A grandfathered (pre-1997) SEP IRA that allows employees to make salary deferrals.

11. SIMPLE IRA

- This is an employer-sponsored workplace plan.

- It functions as a 401(k) “light” version rather than like personal savings account (Traditional or Roth IRA).

- SIMPLE stands for Savings Incentive Match Plan for Employees

- Designed for small businesses (typically <100 employees).

- Requires an employer match and offers Traditional and Roth options.

12. 403(b)

- The statutory equivalent of a 401(k) for employees of

- Public elementary and secondary schools, state colleges, and universities.

- Charities, museums, research institutes, private libraries, and many private foundations.

- Churches, conventions of churches, and associated organizations (like religious hospitals or schools).

- Joint-venture hospital organizations that provide shared services

- Includes Traditional and Roth tracks.

13a. 457(b)

- A deferred compensation plan for

- state and local government employees (police, firefighters, city workers)

- high-level executives or “highly compensated” employees at non-profits (like hospital administrators or charity directors) – see 13b. below for more on this.

- A key feature is the lack of a 10% early-withdrawal penalty once employment ends.

- Available in Traditional and Roth formats.

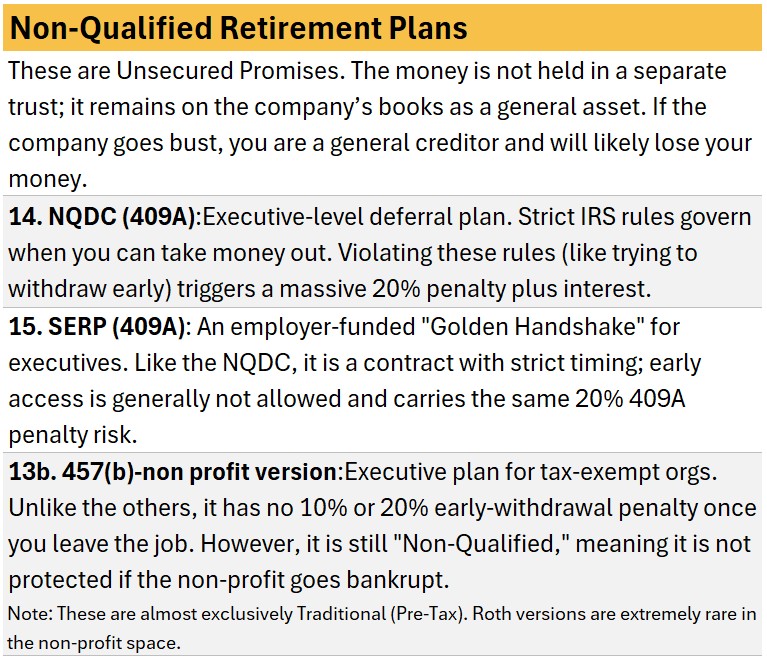

Capital Allocation Structures: Non-Qualified Retirement Plans

These containers are mostly governed by IRS Code Section 409A (NQDC and SERP).

Because the assets remain on the company’s general balance sheet, they are not protected by ERISA.

This means if the company goes bankrupt, you are considered an “unsecured creditor”—meaning your retirement savings could be lost to the company’s other debtholders.

Despite this risk, they are powerful tools for high-earners because they often have no contribution limits and allow for specialized tax deferral.

Table_3 Non Qualified Retirement Plans

14. NQDC (409A)

- Non-Qualified Deferred Compensation

- A common private-sector executive plan.

- It allows you to defer a portion of your salary or bonus to a future date, postponing taxes until the money is actually paid out.

15. SERP (409A)

- Supplemental Executive Retirement Plan

- Often called a “Golden Handshake,”

- this is an employer-funded container used to provide additional benefits to key executives above and beyond what a standard 401(k) allows.

13b. 457(b) (Non-Profit Version)

- While governmental 457(b) plans are protected in trusts, the non-profit version is non-qualified.

- It is an agreement where the executive defers compensation,

- but the money stays with the non-profit organization,

- making it subject to the same “unsecured promise” risks as 409A plans.

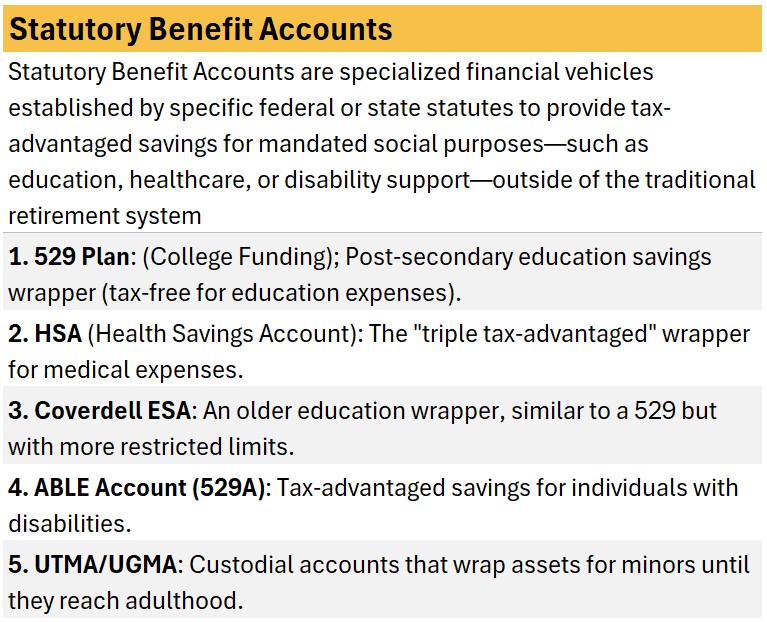

Capital Allocation Structures: Statutory Benefit Accounts

Statutory Benefit Accounts are specialized financial vehicles established by specific federal or state statutes to provide tax-advantaged savings for mandated social purposes—such as

- education,

- healthcare, or

- disability support

outside of the traditional retirement system.

Table_4 Statutory Benefit Accounts

1. 529 Plan (Education Funding)

- You can fund education at almost any level.

- Money grows tax-free and withdrawals are tax-free for tuition, books, and room/board.

- The 2026 “One Big Beautiful Bill Act” has expanded its flexibility and use. (for K-12 tuition and unused funds management)

2. HSA (Health Savings Account)

- The Mission: To cover healthcare costs for those with High-Deductible Health Plans (HDHPs).

- A High Deductible Health Plan is a health insurance plan with a higher deductible than a traditional plan (like a PPO or HMO).

- However, because you are taking on more of the initial cost, these plans typically have lower monthly premiums.

- The Perk: The only Triple Tax-Advantaged account:

- Contributions are tax-deductible (or pre-tax via payroll).

- Growth is tax-free.

- Withdrawals are tax-free for medical expenses.

- If you pay medical bills out-of-pocket and save the receipts, you can reimburse yourself from the HSA years later, effectively using it as a stealth retirement account.

- To be “HSA-compatible,” the IRS sets specific limits each year.

- For 2026, a plan generally must meet these criteria:

- Minimum Deductible: At least $1,650 for individuals or $3,300 for families.

- Out-of-Pocket Maximum: No more than $8,300 for individuals or $16,600 for families.

3. Coverdell ESA (Education Savings Account)

- Named after the late Senator Paul Coverdell

- This is a smaller, more flexible education bucket for families.

- Unlike the 529, Coverdell funds can be used for a wider range of K-12 expenses beyond just tuition (like tutoring, uniforms, and home computers).

- Contribution limits are low ($2,000/year) and there are income limits to participate.

- Most people favor the 529 in 2026 due to the higher limits, but the Coverdell remains a great tool for specific K-12 needs.

4. ABLE Account / 529A (For Individuals with Disabilities)

- ABLE stands for Achieving a Better Life Experience.

- Allows individuals with disabilities to save without losing government benefits (SSI/Medicaid).

- In 2026 eligibility has expanded significantly.

- You can now open an account if the disability began before age 46 (previously age 26).

- The first $100,000 in an ABLE account is generally ignored by Social Security when determining asset limits for benefits.

5. UTMA/UGMA (Custodial Accounts for Minors)

- UGMA stands for: Uniform Gifts to Minors Act

- UTMA stands for: Uniform Transfers to Minors Act

- Holds assets (stocks, property, cash) for a minor without the complexity of a formal Trust.

- The “Kiddie Tax” allows a portion of the earnings (up to $1,350 in 2026) to be tax-free, and another portion to be taxed at the child’s lower rate.

- The Caution:

- These gifts are irrevocable.

- Once the child hits the “age of majority” (18–25 depending on the state), the money is theirs to spend however they want—the parent (custodian) loses all control.

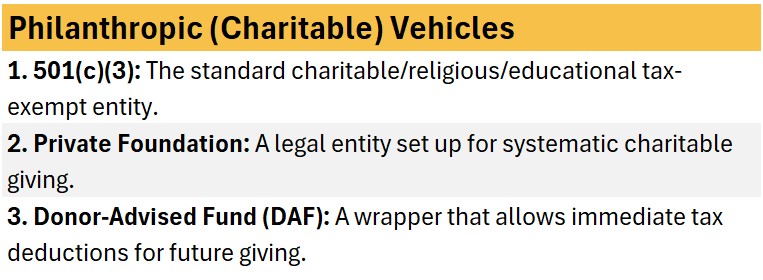

Capital Allocation Structures: Philanthropic (Charitable) Vehicles

These vehicles allow you to transform wealth into a lasting legacy.

By moving assets into these “charitable wrappers,” you receive an immediate tax break today while ensuring the funds are used for the social causes you care about most.

Table_5 Philanthropic (Charitable) Vehicles

1. 501(c)(3): The “Standard Charity”

- The Mission: A standalone nonprofit organization dedicated to religious, educational, or charitable purposes.

- The Advantage: This is the most common status for public charities.

- It allows the organization to operate tax-free and allows donors to claim a tax deduction for their gifts.

- The 2026 Reality: These are often the “recipients” of the money from the other two vehicles below.

2. Private Foundation: The “Family Legacy Vault”

- The Mission: A private 501(c)(3) entity established and controlled by an individual or family to manage their systematic giving.

- The Advantage: Total Control. You can hire family members, run your own programs, and even make grants directly to individuals (like scholarships) under specific rules.

- The Catch: It is expensive to set up (requires legal/accounting) and public.

- In 2026, foundations must still pay a small 1.39% excise tax on their investment income and file public reports (Form 990-PF) disclosing all board members and grants.

3. Donor-Advised Fund (DAF): The “Charitable Checking Account”

- The Mission: A specialized account maintained by a “sponsoring” public charity (like Fidelity Charitable or a local Community Foundation).

- The Advantage: Simplicity and Speed. You get an immediate tax deduction when you put money in, but you can wait years to decide which charities to give it to.

- The 2026 Edge: DAFs generally offer higher tax deduction limits than private foundations (60% of AGI for cash gifts vs. 30% for foundations). Plus, grants from a DAF can be made anonymously, whereas foundation grants are public record.

Note:

- If you want to give away less than $2 million and value simplicity and privacy, a Donor-Advised Fund is almost always the winner.

- If you have over $5–$10 million and want to build a formal family office with paid staff and unique programs, a Private Foundation is the gold standard.

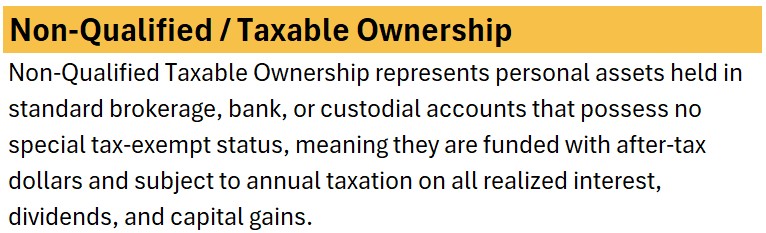

Capital Allocation Structures: Non-Qualified Taxable Accounts

“The Flexibility Bucket”: These are your standard “everyday” investment accounts.

Unlike retirement accounts, they have no locks, no penalties for early access, and no contribution limits.

They are your primary tool for goals occurring before age 59.5, such as buying a home, starting a business, or retiring early.

So, think of your Taxable Brokerage as your ‘Freedom Fund’.

While 401ks and IRAs are for ‘Future You’ (age 60+), this account is for ‘Current You.’

Use it to build the bridge between your working years and your retirement years.

Table_6 Non-Qualified Taxable Ownership

1. Standard Brokerage Account

- The Mission: A retail account (at firms like Vanguard, Fidelity, or Schwab) used to buy stocks, bonds, and ETFs with money that has already been taxed.

- The Advantage:

- Total Liquidity.

- You can withdraw your money at any time for any reason.

- In 2026, these are the “bridge” accounts that allow you to fund your lifestyle before your retirement accounts become available.

- The Tax Treatment: You pay taxes “as you go.”

- You are taxed annually on interest and dividends, and

- you pay Capital Gains Tax only when you sell an asset for a profit.

2. Cash & Cash Equivalents (Bank/HYSA):

- The Mission:

- High-Yield Savings Accounts (HYSA),

- Money Market Funds, and

- CDs.

- The Advantage:

- Principal Preservation.

- These are the safest “containers” for your Emergency Fund.

Advanced Strategies for This Category

Long-Term Capital Gains (The 1-Year Rule)

In 2026, if you hold an investment for more than one year, your tax rate on the profit drops significantly—often to 15% or even 0% depending on your income—compared to your much higher ordinary income tax rate.

- Tax-Loss Harvesting:

- If an investment loses value, you can sell it to “harvest” the loss.

- This loss can be used to cancel out taxes on your winning investments or even reduce your taxable salary by up to $3,000 per year.

- The “Step-Up in Basis” (The Legacy Perk):

- Under the One Big Beautiful Bill Act of 2026, the “Step-Up” rule remains intact.

- This means if you hold highly appreciated stocks in a taxable account until you pass away,

- your heirs inherit them at the current market value,

- effectively wiping out years of capital gains taxes for the next generation.

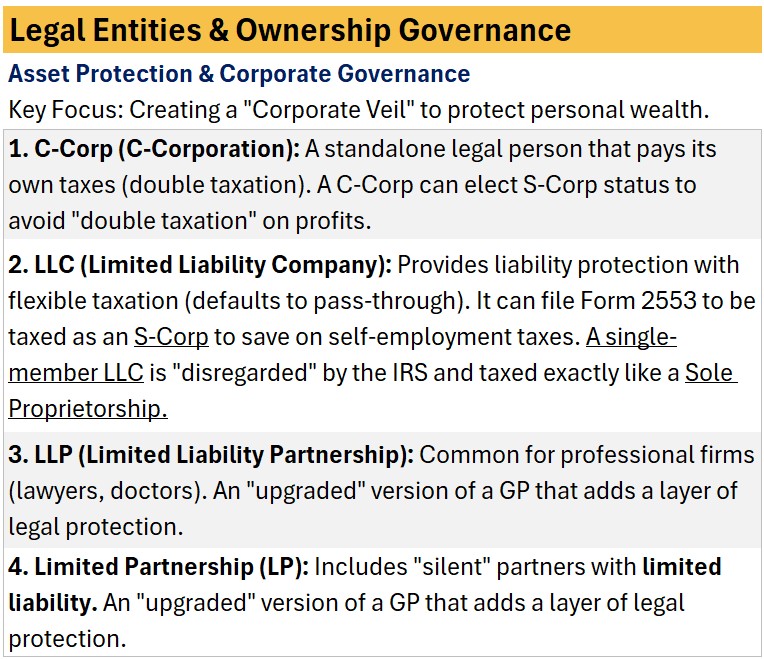

Capital Allocation Structures: Legal Entities and Ownership Governance

Category_1 : Asset Protection and Corporate Governance

This category defines how you separate your human self from your business self.

In the eyes of the law, these entities act as a “shield” so that if the business is sued or goes bankrupt, your personal house and retirement accounts remain untouched.

Table_7 Legal Entities and Ownership Governance

1. C-Corp (C-Corporation)

- The “Standard Fortress.”

- It is a completely independent legal person.

- It pays its own 21% flat tax, but if it pays you a dividend, you are taxed again (Double Taxation).

2. LLC (Limited Liability Company)

- The “Hybrid Shield.”

- It offers the same legal protection as a corporation but with the simplicity of a partnership.

- It is the gold standard for small businesses and real estate investors.

3. LLP (Limited Liability Partnership)

- The “Professional Shield.”

- Specifically designed for licensed professionals (doctors, lawyers, CPAs) so that one partner isn’t personally liable for another partner’s malpractice.

4. Limited Partnership (LP)

- The “Investor’s Wrapper.”

- One general partner runs the show (and has the liability), while “Limited Partners” provide the cash and have their risk capped at exactly what they invested.

Table_8 Legal Entities and Ownership Governance (continued)

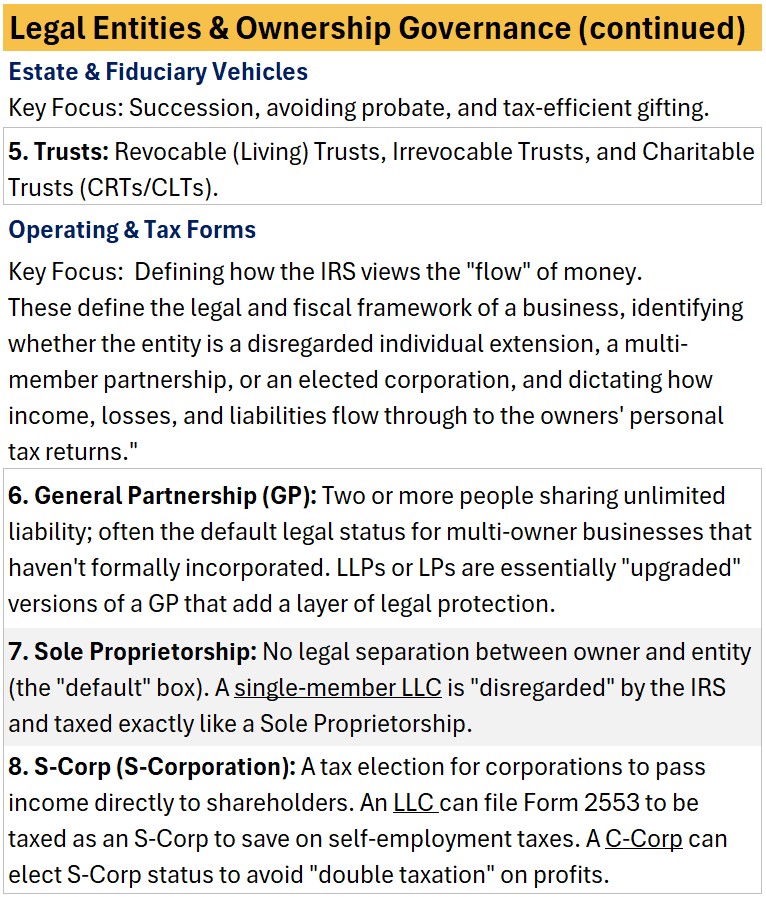

Category_2: Estate & Fiduciary Vehicles

“The Legacy Map”: These vehicles determine who gets your wealth, how they get it, and how much the government takes.

5. Trusts

- Revocable (Living) Trust: Your “Probate Bypass.” You control it while alive, and it moves your assets to heirs instantly upon death without a public court battle.

- Irrevocable Trust: The “Asset Vault.” Once you put money in, you can’t easily take it back, but it is now invisible to creditors and the estate tax.

- Charitable Trust (CRT/CLT): The “Tax-Efficient Gift.” Allows you to give to charity while receiving an immediate tax break and an income stream for life.

Category_3: Operating & Tax Forms

“The IRS Lens”: This category is purely about how the IRS views the “flow” of your money.

It defines whether the government taxes the entity first or just follows the money straight to your personal 1040 return.

6. General Partnership (GP)

- The “Accidental Business.”

- If two people start a business without filing paperwork, they are a GP.

- Warning: Every partner is 100% liable for the other’s mistakes.

7. Sole Proprietorship

- The “Default Setting.”

- If you are a freelancer or side-hustler with no LLC, you are a Sole Prop.

- You and the business are legally the same person.

8. S-Corp (S-Corporation)

- The “Tax Magic Election.”

- It is not a legal entity—it is a tax status.

- By electing S-Corp status via Form 2553, an LLC or C-Corp can avoid “double taxation” and significantly reduce self-employment taxes by splitting income into “Salary” and “Distributions.”

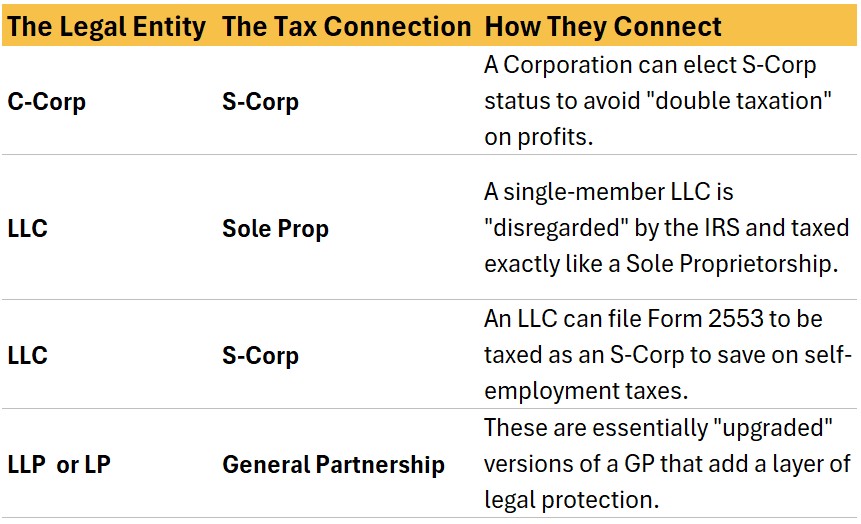

Connection between Legal Entities and Tax Entities

In table_9 below I show the relationship between items 1 – 4 (C-Corp, LLC, LLP, LP) and 6 – 8 (Sole Corp, S Corp, General Partnership) in tables 7 and 8 above.

The relationship between these tables highlights the difference between a legal structure and its operational form.

For instance, an S-Corp is not actually a separate type of company you form at the state level;

- rather, it is a tax election that C-Corps and LLCs ‘nest’ within.

In the same vein, LLPs and LPs function as specialized versions of a General Partnership,

- where the law has modified the standard GP rules to provide limited liability to the participants

Table_9 Connection between Legal Entities and Tax Entities

Traditional IRAs and Roth IRAs

First rolled out in 1974, IRAs (Individual Retirement Accounts) were designed to give individuals personal control over their retirement security.

Today, they remain the two most popular tools for independent saving, distinguished primarily by their tax structure.

Traditional IRA

- You contribute dollars that may be tax-deductible depending on your income and whether you have a workplace retirement plan.

- If eligible, it lowers your taxable income today;

- if not, you are making “non-deductible” contributions.

- Your investments grow tax-deferred, but

- you will pay ordinary income tax on all withdrawals during retirement.

- You contribute dollars that may be tax-deductible depending on your income and whether you have a workplace retirement plan.

Roth IRA

- You contribute after-tax dollars, so there is no immediate tax break (no deductions).

- In exchange, your investments grow tax-free, and

- qualified withdrawals in retirement are completely exempt from federal taxes.

The IRA: History

The Individual Retirement Account (IRA) was born out of a crisis of confidence.

In the early 1970s, high-profile corporate pension failures—most notably the collapse of the Studebaker-Packard motor company—left thousands of workers with nothing after decades of service.

In response, Congress passed the Employee Retirement Income Security Act (ERISA) of 1974.

Signed into law on Labor Day by President Gerald Ford, ERISA created the “Traditional IRA” to give workers a way to save for retirement independently of their employers.

The Evolution of the “Bucket”

For fifty years, the IRA has evolved from a simple safety net into a sophisticated wealth-building tool.

- 1974 (The Beginning): The Traditional IRA is created.

- The official legal name used by the IRS and the 1974 legislation (ERISA) is Individual Retirement Arrangement.

- The term “Arrangement” was chosen to be broad enough to cover both bank-style accounts and insurance-style annuities.

- However, because the vast majority of people open their IRAs at banks or brokerages, “Account” became the common shorthand

- 1981 (Expansion): The Economic Recovery Tax Act makes IRAs available to all working Americans, regardless of whether they have a pension at work.

- 1997 (The Roth Revolution): Named after Senator William Roth, the Roth IRA is introduced.

![]()

- It flips the script: you pay taxes today, but the money grows and is withdrawn tax-free in the future.

- 2026 (The SECURE Era): Following the landmark SECURE 2.0 Act, the IRA has become more flexible than ever.

- There is no longer an age limit for contributions, and

- the “catch-up” limits for those over 50 are now adjusted annually for inflation to protect your purchasing power.

At its core, the IRA is your personal tax-sheltered “container.”

While 401(k)s and other workplace plans are tied to your job, the IRA is tied to you.

It is the most accessible way for any individual with earned income to take control of their financial destiny.

IRA First Principles

Before diving into the “logic” of which IRA to choose, we need to establish some “first principles”.

These are the non-negotiables that the IRS applies regardless of which path (Traditional or Roth) the investor takes.

Here are the essential IRA “truths”.

1. IRAs are Individual only (No “Joint” IRAs exist)

Unlike a standard bank account or a taxable brokerage account, an IRA cannot be held as “Joint Tenants with Rights of Survivorship” or “Community Property.

- Every IRA is tied to a single Social Security number.

- You cannot add a spouse or child as a co-owner.

- The Spousal Exception (Contribution, not Ownership):

- A common point of confusion is the Spousal IRA.

- While a working spouse can fund an IRA for a non-working spouse, the account itself is still opened in only one person’s name.

- The non-working spouse is the sole legal owner of that account.

- How Couples “Jointly” Manage Them

- Since they can’t be jointly owned, couples typically use two strategies to treat them as joint assets:

- Beneficiary Designations: You name your spouse as the primary beneficiary.

- In many states (and under federal law for some plans), a spouse has an automatic right to the account unless they waive it in writing.

- Coordinated Strategy: Couples often view their separate IRAs as one “household” portfolio, balancing the investments across both accounts to hit their target asset allocation.

2. The “Single Bucket” Rule (Aggregate Limits)

Traditional IRAs and Roth IRAs DO NOT have separate limits.

- You can have several different IRA accounts at several different banks, but your total combined contribution for the year is capped at one number.

- For example, for 2026, the limits are:

- $7,500 ($8,600 if age 50+).

- You can split this $4,000/$3,500, or put it all in one, but you cannot exceed the total.

3. The “Earned Income” Floor

You cannot contribute “passive” money to an IRA. It has to be “earned income”.

- The Rule: Your contribution cannot exceed your Taxable Compensation (wages, tips, bonuses, or self-employment income).

- If you had a bad year in business and your net profit was only $3,000, your IRA contribution is capped at $3,000, even if you have $1 million sitting in a savings account.

- The Spousal IRA.

- If one spouse works and the other doesn’t, the working spouse’s income can “fund” an IRA for the non-working spouse (provided they file jointly).

4. The “Tax Year” Overlap (The April Window)

The IRA calendar doesn’t end on December 31.

- The Window: You can contribute for a tax year starting January 1 of that year all the way until the April Tax Deadline of the following year.

- Why it matters:

- From January 1 to April 15, you are in the “Overlap Zone” where you can choose which year your contribution counts toward.

- You must explicitly tell your custodian which year you are choosing.

5. The “Pro-Rata” Aggregation (The Backdoor Trap)

When the IRS looks at your IRAs for tax purposes (especially during a Roth Conversion or “Backdoor” move which we will discuss later), they don’t see separate accounts.

- The Reality:

- They see one giant “IRA Bucket.”

- If you have $90,000 in a Traditional IRA from an old 401k rollover and you try to do a $7,500 “Backdoor Roth” with new after-tax money, the IRS will tax you on ~92% of that conversion because of the existing pre-tax money.

- The Fix:

- This is why “Reverse Rollovers” (moving IRA money back into a 401k) are a prerequisite for many high-income strategies.

6. Age is No Longer a Barrier

A legacy rule used to stop people from contributing to Traditional IRAs after age 70.5.

Current Status:

- As of the SECURE Act (and confirmed in 2026), there is no upper age limit for contributions.

- As long as you have earned income, you can contribute at age 100.

9. Catch up money

You can usually add more money if you are over a certain age barrier.

- For 2026: Contribution limit = $7,500 (under 50) or $8,600 (50+)

10. Custody

To maintain the tax-advantaged status, the IRA assets must be held by a qualified trustee or custodian.

The Legal “Gatekeeper”

The IRS requires a neutral third party to act as the official record-keeper, asset safekeeper, and rule enforcer.

Who Qualifies?

These are the custodians (hold the assets and execute your trades but do not provide investment advice):

- Banks and Credit Unions

- Brokerage Firms (like Fidelity, Schwab, or Vanguard)

- Trust Companies (often used for “Self-Directed” IRAs that hold real estate or private equity)

Rules and Requirements for Funding IRAs

Navigating IRA contributions requires balancing income limits, workplace retirement plans, and tax-deductibility rules.

The following decision trees provide a step-by-step path to determine your eligibility, starting with

- Traditional IRAs,

- moving through “Front Door” Roth options, and

- concluding with “Backdoor” Roth strategies for high-income earners

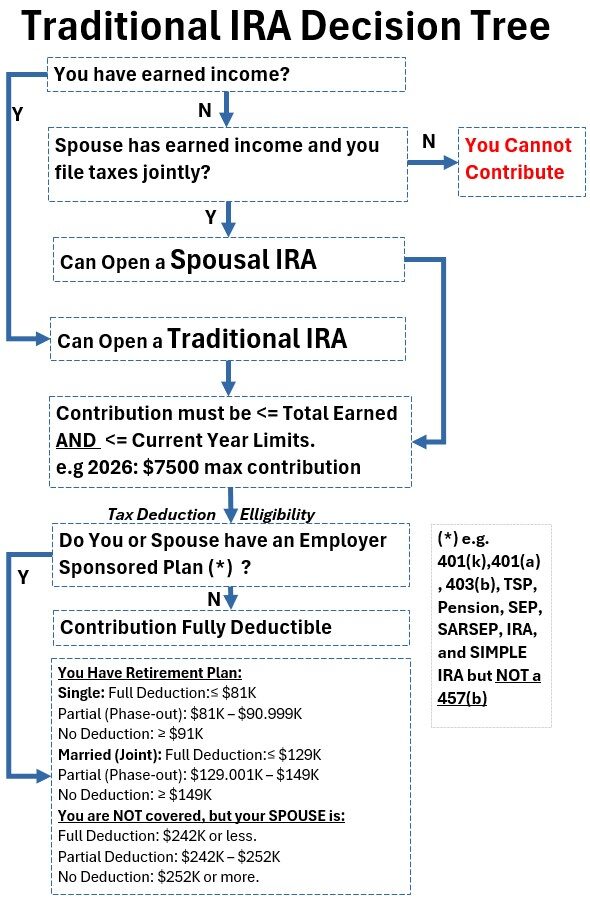

Let’s start with the Traditional IRA: Check out its decision tree graphic below.

Chart_Traditional IRA Decision Tree

Guide to Funding A Traditional IRA (See Chart Above; 2026 tax year)

1. The “Gatekeeper” Rule: Earned Income

Before looking at limits or deductions, you must pass the income test.

- The Rule: You (or your spouse, if filing jointly) must have taxable compensation.

- This includes wages, salaries, tips, and self-employment income.

- What Doesn’t Count: Passive income (dividends, interest, rental property) or Social Security benefits.

- The Spousal Loophole: If you have $0 in earned income but your spouse works, you can open a “Spousal IRA” based on their earnings, provided you file a joint return.

2. Contribution Limits (2026)

This is the “ceiling” for how much cash can actually enter the account.

- Standard Limit: $7,500 per person.

- Catch-Up: If you are age 50 or older, you can contribute an extra $1,100 (total $8,600).

- The “Lesser Of” Clause:

- You cannot contribute more than you actually earned.

- If you only made $3,000 in 2026, $3,000 is your maximum contribution.

3. The Tax Deduction “Phase-Out”

Unlike a Roth IRA (where anyone under an income cap. can contribute), anyone with earned income can contribute to a Traditional IRA.

The “decision” in the flow chart is whether that contribution is tax-deductible.

Scenario_A: Neither you nor your spouse have a retirement plan at work

The Result: You get a full deduction regardless of how much money you make.

Scenario_B: You ARE covered by a retirement plan at work

- Your deduction depends on your Modified Adjusted Gross Income (MAGI)

- Filing Status: Single

- Full Deduction:≤ $81,000

- Partial (Phase-out): $81,001 – $90,999

- No Deduction: ≥ $91,000

- Filing Status: Married (Joint)

- Full Deduction:≤ $129,000

- Partial (Phase-out): $129,001 – $149,000

- No Deduction: ≥ $149,000

Scenario_C: You are NOT covered, but your SPOUSE is

- Full Deduction: MAGI of $242,000 or less.

- Partial Deduction: MAGI between $242,000 – $252,000.

- No Deduction: MAGI of $252,000 or more.

If you find you are in the “No Deduction” zone, you can still make a nondeductible contribution.

- You won’t get a tax break today, but the money grows tax-deferred.

- In that case, many people look into the “Backdoor Roth” strategy.

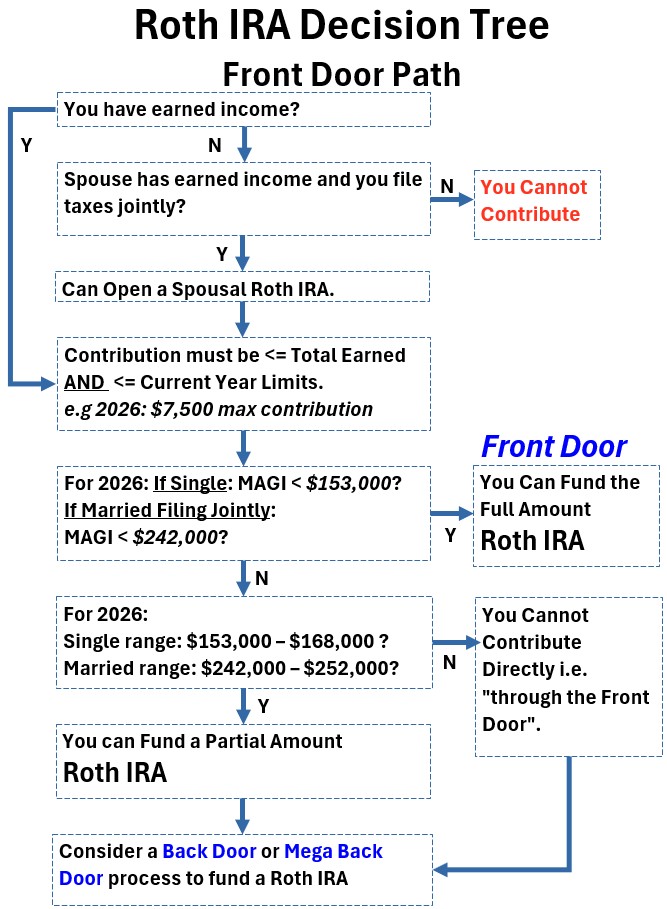

Let’s next take a look at the chart below which shows the so called “Front Door” path to funding a Roth IRA.

Chart_Roth IRA (Front Door) Decision Tree

Guide to Funding a Roth IRA via the “Font Door” (See Chart Above; 2026 tax year)

1. Requirement: Earned Income

Just like the Traditional IRA, the door is locked if you didn’t work.

- The Rule: You must have taxable compensation (W-2 wages, tips, or self-employment profit).

- The Limit:

- Your contribution cannot exceed your earned income.

- If you earned $5,000, you can only contribute $5,000.

- Spousal Exception: If you didn’t work but your spouse did, you can use their income to fund your own Roth IRA (Spousal Roth), provided you file jointly.

2. Annual Contribution Limits (2026)

This is the maximum amount of “after-tax” cash you can put in.

- Under Age 50: $7,500

- Age 50 and Older: $8,600 (includes the $1,100 catch-up)

3. The Income Test (MAGI)

The “Front Door” stays open or shut based on your Modified Adjusted Gross Income (MAGI).

If your income is too high, the IRS forces you to use the “Backdoor” route.

- Single or Head of Household

- You can make a full contribution if your MAGI is under $153,000.

- Your ability to contribute is reduced (phased out) between $153,000 and $167,999, and

- the door is completely closed at $168,000 or more.

- Married Filing Jointly

- You can make a full contribution if your joint MAGI is under $242,000.

- Your contribution is reduced between $242,000 and $251,999, and

- the door is completely closed at $252,000 or more.

- Married Filing Separately

- If you lived with your spouse at any time during the year, your ability to contribute is reduced immediately starting at $0 and the door is completely closed once your MAGI hits $10,000.

4. The “Partial” Math

If you fall in the Phase-out range, your $7,500 (or $8,600) limit is reduced proportionally.

- Example: If you are Single and earn $160,500 (exactly the midpoint of the phase-out),

- your contribution limit is cut in half to $3,750.

- Pro-tip: Most people in the phase-out range skip the math and just do the Backdoor Roth anyway

- to ensure they hit the full $7,500 limit without over-contributing.

Key Takeaway

If your MAGI is below the “Full Contribution” threshold and you have earned income, you simply open the account, deposit the cash, and you’re done.

If you’re above it, stop here and switch to your Backdoor decision tree.

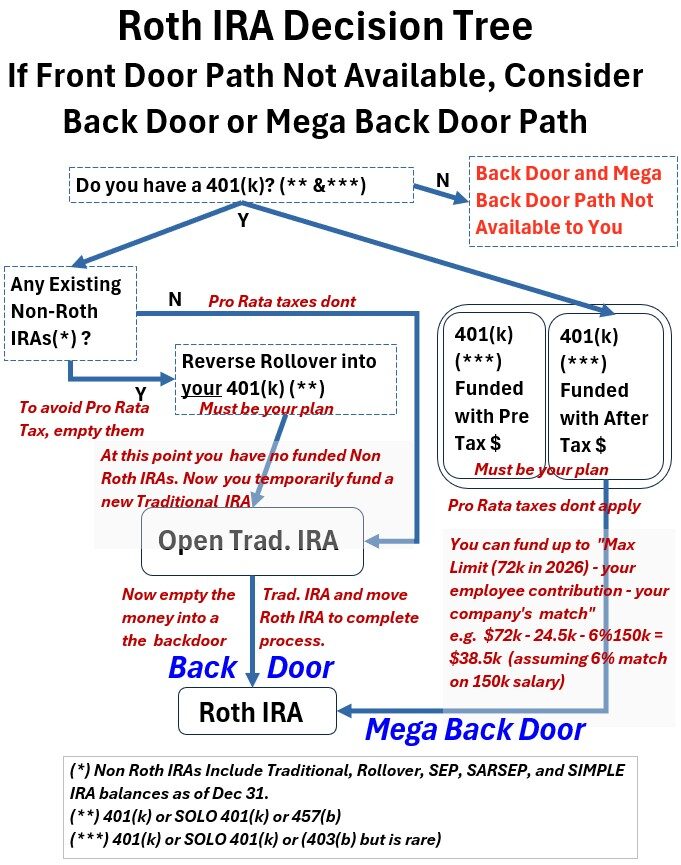

Now let’s take a look at the “back door” methods for funding a Roth IRA (See Chart below).

Chart_Roth IRA (Backdoor) Decision Tree

Guide to Funding a Roth IRA using “Back Door” Techniques (See Chart Above; 2026 tax year)

When the “Front Door” is locked due to high income, you pivot to the Backdoor and Mega Backdoor paths.

These are essentially legal workarounds to get money into a Roth environment.

1. The Backdoor Roth IRA (The “Standard” Loophole)

Use this if you exceed the Roth income limits but still want to put $7,500...for 2026 ($8,600 if 50+..for 2026) into a Roth account.

- Step_A: The Contribution. You make a non-deductible contribution to a Traditional IRA.

- You get no tax break now, but anyone can do this regardless of income.

- Step_B: The Conversion. You immediately move (convert) that money into a Roth IRA.

- The “Pro-Rata” Trap: This only works cleanly if you have zero other pre-tax money in any Traditional, SEP, or SIMPLE IRAs.

- If you have $100k in an old Rollover IRA and try to do a $7,500 Backdoor Roth, the IRS will tax the conversion proportionally based on that $100k balance.

- The Fix: If you have pre-tax IRA balances, try to “Reverse Rollover” them into your current 401(k) first to clear the way.

2. The Mega Backdoor Roth (The “Whale” Loophole)

This happens inside your workplace 401(k) (or other plan) and allows you to shield up to $72,000 (total plan limit for 2026) in a Roth account.

The Prerequisites

Your employer’s plan must allow two specific things, or this is a “No-Go”:

- After-Tax Contributions: Not “Roth” and not “Pre-tax,” but a third category called “After-tax.”

- In-Service Distributions: The ability to move those after-tax dollars out to a Roth IRA (or into the Roth 401(k) side) while you are still employed.

How the Math Works (2026)

You fill the “gap” between your regular contributions and the IRS total limit:

- Start with the Limit: $72,000 (standard) or $80,000 (age 50+).

- Subtract your 401(k) contribution: -$24,500.

- Subtract your Employer Match: (e.g., -$9,000).

- Remaining Gap: $38,500. You can contribute this entire amount as “After-Tax” and then immediately convert it to Roth.

Which one to Choose? Roth or Traditional?

All examples in this section are based on 2026 rules.

So, Before you decide which is better (Traditional IRA, Roth IRA), you have to look at the decision trees and see which ones are legal for your specific income level and workplace status.

Traditional IRA Decision Tree (Can I deduct)?

This depends on your income.

For example,

- If you have a 401(k) and make over $91k (Single) / $149k (Joint) in 2026, this tree ends in a “No.”

- You can still put money in, but you get no tax break today.

Front-Door Roth Tree (Can I contribute directly)?

This also depends on your income.

For example,

- If you make over $168k (Single) / $252k (Joint) in 2026, this tree ends in a “No.”

- The “Front Door” is locked.

Backdoor Roth Tree (Is the “Side Door” open)?

- This tree is almost always a “Yes” regardless of income, provided you don’t have other large Traditional IRA balances (because of the “Pro-Rata Rule”)

- You might be able to avoid the Pro-Rata tax with a reverse rollover in your retirement plan as described in the decision tree.

The “Cross-Roads” Question: Traditional vs. Roth

Once you know which trees are still standing, then you can start comparing your available options for best choice.

Scenario_A: The High-Earner Choice

If you make $200k+, you cannot deduct a Traditional IRA and you cannot do a Front-Door Roth.

- The Choice: Do I do a “Non-deductible Traditional” (worst option) or a Backdoor Roth (best option)?

- Decision: The Roth wins 100% of the time here because “Tax-Free later” is better than “Taxed later” when you didn’t get a break today anyway.

Scenario_B: The Mid-Earner Choice

If you make $70k, both the Traditional (deductible) and the Roth (front-door) trees are “Yes.”

- The Choice: Do I want the tax break now or later?

- Decision Matrix:

- Traditional: If you are in your peak earning years now and think you’ll be in a lower bracket in retirement.

- Roth: If you are in a low bracket now or think tax rates will rise significantly in the future.

Scenario_C: The Low-Earner Choice

If you make < $40k ($80k Joint), both doors are open, but you have a third factor: The Saver’s Credit.

- The Choice: Do I choose the Roth for the long-term tax-free growth, or the Traditional to lower my income for a bigger government credit?

- Decision Matrix:

- Roth: The default winner.

- Since your current tax rate is already very low (10–12%), a deduction is worth very little.

- You’re better off locking in tax-free growth forever.

- Traditional: Only if your income is slightly over a “cliff” for the Saver’s Credit

- e.g., you earn $26k but need to get under $24,250 to qualify for the 50% credit.

- In this case, the Traditional IRA acts as a tool to “buy” a larger tax credit from the IRS.

- Roth: The default winner.

By looking at it this way, you realize that for many people, the “Decision” is actually made for them by their income.

- Low Income: Both doors are open: Choose Roth (usually).

- Middle Income: Both doors are open: The Real Debate (Tax Arbitrage).

- High Income: Only the Backdoor is open: Backdoor Roth is the only logical move.

Maximum Dollar Capacities for Various Household Scenarios

Let’s come back to the organization chart (Chart_2) which I show again below.

How does one go about choosing

- which plans are available?

- how much money can be put in them?

- what (if any) order to use them in?

Chart_2 Capital Allocation Structures (Legal And Tax Frameworks)

You want to do this in two broad steps

- Determine the available “containers” and the amount of money you are allowed by law to invest in them

- And then stack them in a certain order to optimize tax efficiency and maximize investment growth

Marriage and Working Status Scenarios

Navigating the grid of retirement and tax-advantaged accounts depends entirely on two variables:

- your household filing status and

- your source of income.

While a

- corporate job provides structured benefits like a 401(k),

- self-employment often unlocks higher contribution ceilings, and

- non-working status requires utilizing “spousal” rules to keep a tax-advantaged strategy alive.

By layering in Health Savings Accounts (HSAs) and IRAs (Individual Retirement Accounts or Arrangements), you can create a “triple tax-advantaged” shield that protects your wealth regardless of your employment configuration.

Let’s explore the various retirement plans available to 9 different household scenarios as listed below.

The 9 Household Scenarios

1. Single: NW (Not Working)

2. Single: CORP (Working for Company; gets a W-2)

3. Single: SOLOB (Solo Business Owner; gets a 1099)

4. Married: CORP + CORP

5. Married: CORP + SOLOB

6. Married: SOLOB + SOLOB

7. Married: CORP + NW

8. Married: SOLOB + NW

9. Married: NW + NW

General Notes

As you review the retirement container options for each of the 9 household scenarios please be aware of the following:

HSAs

- HSAs must have an HDHP-compatible health plan to open an HSA , but check for exceptions.

- HDHP stands for High Deductible Health Plan. Traditional PPOs or HMOs are not HDHPs.

IRA Types

- The two types are the Traditional and the Roth which we discussed in detail in a previous section.

- You have to follow a decision tree to see which you qualify for and how much you can add to them.

- Note that SEP IRAs and SIMPLE IRAs are not individual retirement accounts. They are workplace plans.

Workplace Plans

- 401(k)

- These are the standard corporate plans.

- They allow employee deferrals plus employer matching/profit sharing.

- Solo 401(k)

- These follow the same rules as a 401(k) but are designed for owner-only businesses.

- It allows you to act as both employee (deferral) and employer to hit the maximum cap faster.

The following are called IRAs, but they are more closely aligned with 401ks because they are also workplace plans.

- SEP IRA

- An employer-only plan.

- No employee deferrals allowed.

- The business contributes up to 25% of your pay, capped at $72,000.

- Best for high-income solo earners who want zero-paperwork flexibility.

- SIMPLE IRA

- A “light” workplace plan for small teams.

- Has a lower employee limit ($17,000) and a mandatory employer match (usually 3%)

In all the scenarios with Solo Business retirement options, we will assume the 401(k) is the chosen option.

See Appendix 1 for more information.

2026 Tax Advantaged Plan Limits

HSA

- $4,400 (Single)

- $8,750 (Family)

- $1,000 Catch-up (Age 55+)

- Note that these are individual accounts so a married couple would each have their own and the 1000 catch would apply to each person.

- So if they are both 55 or older then max will be $8,750 + $2,000 = $10,750.

- ?Why have two separate limits when there is only a 50 dollar difference (2 x 4400 vs 8750)?

IRA

- $7,500

- $1,100 Catch-up (Age 50+) for a total of $8,600

401(k)

- Employee: $24,500

- $8,000 Catch-up (Age 50+): $32.5k total

- $11,250 Super Catch-up (Age 60-63): $35.75k total

Solo 401(k)

- Total Cap: $72,000

- Depending on what type of legal entity your business is, there will be a 20% to 25% cap on how much employer match you can get.

- This means that to hit the $72,000 total limit in 2026, your income must be high enough to support that percentage:

- S-Corps (25% Cap): You need a W-2 salary of $190,000 ($24.5k deferral + $47.5k employer match).

- Sole Proprietors (~20% Cap): You need a net profit of $240,000 (because the IRS forces you to subtract taxes and your own contribution first, effectively lowering your 25% cap to 20%).

- 8,000 Catch-up (Age 50+)

- $11,250 Super Catch-up (Age 60-63)

- Total Cap: $72,000

Household Scenarios/Capacity Dollars – Introduction

The following Listings (I through IV sections below) are designed to show the maximum legal capacity for various household and employment scenarios in 2026.

Reaching these numbers depends on several critical “real-world” factors.

- Income Constraints: You must have enough taxable earned income to cover your contributions;

- for example, you cannot contribute $7.5k to an IRA if you only earned $3k in wages.

- Health Plan Requirement: All HSA figures assume you are enrolled in a High Deductible Health Plan (HDHP).

- Without one, your HSA capacity is $0.

- Employer Plan Rules: While the IRS allows a “Super Catch-up” for ages 60–63, your specific company’s 401(k) plan must officially adopt these SECURE 2.0 provisions for you to use them.

- The Roth Requirement: For 401(k) catch-ups, if you earned over $150k in the previous year (2025), the IRS requires that your catch-up contributions be made as Roth (after-tax).

- Phase-outs: High-income earners may face “phase-outs” that reduce or eliminate the ability to contribute directly to a Roth IRA or deduct Traditional IRA contributions.

Household Scenarios/Capacity Dollars – Important Notes on 2026 Strategy

We are now going to look at capacity dollars available for our 9 household scenarios (The listings under I. to IV. starting in the next section)

These show the 2026 maximum legal capacity for

- various household and

- employment scenarios

- and for different age groupings

They are intended to highlight significant tax-saving opportunities for you to investigate, but you must look further to determine your exact limits:

Workplace Plans

- The household capacity listings (I. through IV. below) prioritize 401(k) and Solo 401(k) structures because they provide the highest legal contribution ceilings for 2026.

- SEP IRAs and SIMPLE IRAs were not included because they often result in lower total capacities (See Appendix 1)

- Specifically, a SIMPLE IRA caps your employee contribution at $17,000 (vs. $24,500), and

- a SEP IRA lacks catch-up provisions for those over 50.

- If SIMPLE or SEP IRAs are the only plans available through your current employer, your actual maximum capacity will likely be lower than the figures shown in the listing.

Income & Entity Constraints

- Your actual contribution limit is contingent on your legal entity type (which sets a 20% to 25% cap on non-employee money) and your income level.

- For example, hitting the $72,000 Solo 401(k) max generally requires earnings in the $190k–$240k range.

IRA Selection

- The lists in I. through IV. below show total IRA capacity, but do not specify the type of IRA (Traditional vs. Roth).

- Your eligibility to deduct a Traditional IRA or contribute directly to a Roth depends on your specific Modified Adjusted Gross Income (MAGI) and workplace coverage, as outlined in the IRA decision paths described earlier in this article.

HSA Paperwork

- While the “Family” limit is $8,750, catch-up contributions ($1,000) are individual.

- If both spouses are 55+, you must use two separate HSA accounts to capture the full $10,750 ($8,750 + $1,000 + $1,000) household capacity.

I. Household Scenarios/Capacity Dollars/Under Age 50

k = $1,000; Capacity means maximum possible and not necessary what you will be able to get.

1 Single: NW

- Capacity: $4.4k

- Math: $4.4k (HSA)

2 Single: CORP

- Capacity: $36.4k

- Math: $4.4k (HSA) + $7.5k (IRA) + $24.5k (401k)

3 Single: SOLOB

- Capacity: $83.9k

- Math: $4.4k (HSA) + $7.5k (IRA) + $72k (Solo)

4 Married: CORP+CORP

- Capacity: $72.75k

- Math: $8.75k (HSA) + $15k (2 IRAs) + $49k (2 401ks)

5 Married: CORP+SOLOB

- Capacity: $120.25k

- Math: $8.75k (HSA) + $15k (2 IRAs) + $24.5k (401k) + $72k (Solo)

6 Married: SOLOB+SOLOB

- Capacity: $167.75k

- Math: $8.75k (HSA) + $15k (2 IRAs) + $144k (2 Solos)

7 Married: CORP+NW

- Capacity: $48.25k

- Math: $8.75k (HSA) + $15k (2 IRAs) + $24.5k (401k)

8 Married: SOLOB+NW

- Capacity: $95.75k

- Math: $8.75k (HSA) + $15k (2 IRAs) + $72k (Solo)

9 Married: NW+NW

- Capacity: $8.75k

- Math: $8.75k (HSA)

II. Household Scenarios/Capacity Dollars/Ages 50-54

k = $1,000; Capacity means maximum possible and not necessary what you will be able to get.

1 Single: NW

- Capacity: $4.4k

- Math: $4.4k (HSA)

2 Single: CORP

- Capacity: $45.5k

- Math: $4.4k (HSA) + $8.6k (IRA) + $32.5k (401k)

3 Single: SOLOB

- Capacity: $93.0k

- Math: $4.4k (HSA) + $8.6k (IRA) + $80k (Solo)

4 Married: CORP+CORP

- Capacity: $91.0k

- Math: $8.75k (HSA) + $17.2k (2 IRAs) + $65k (2 401ks)

5 Married: CORP+SOLOB

- Capacity: $138.5k

- Math: $8.75k (HSA) + $17.2k (2 IRAs) + $32.5k (401k) + $80k (Solo)

6 Married: SOLOB+SOLOB

- Capacity: $186.0k

- Math: $8.75k (HSA) + $17.2k (2 IRAs) + $160k (2 Solos)

7 Married: CORP+NW

- Capacity: $58.5k

- Math: $8.75k (HSA) + $17.2k (2 IRAs) + $32.5k (401k)

8 Married: SOLOB+NW

- Capacity: $106.0k

- Math: $8.75k (HSA) + $17.2k (2 IRAs) + $80k (Solo)

9 Married: NW+NW

- Capacity: $8.75k

- Math: $8.75k (HSA)

III. Household Scenarios/Capacity Dollars/Ages 55-59

k = $1,000; Capacity means maximum possible and not necessary what you will be able to get.

* = Married couples need two separate HSA accounts for dual catch-ups (the $10.75k total).

1 Single: NW

- Capacity: $5.4k

- Math: $5.4k (HSA + Catch)

2 Single: CORP

- Capacity: $46.5k

- Math: $5.4k (HSA) + $8.6k (IRA) + $32.5k (401k)

3 Single: SOLOB

- Capacity: $94.0k

- Math: $5.4k (HSA) + $8.6k (IRA) + $80k (Solo)

4 Married: CORP+CORP

- Capacity: $93.0k

- Math: $10.75k (HSA + 2 Catch*) + $17.2k (2 IRAs) + $65k (2 401ks)

5 Married: CORP+SOLOB

- Capacity: $140.5k

- Math: $10.75k (HSA + 2 Catch*) + $17.2k (2 IRAs) + $32.5k (401k) + $80k (Solo)

6 Married: SOLOB+SOLOB

- Capacity: $188.0k

- Math: $10.75k (HSA + 2 Catch*) + $17.2k (2 IRAs) + $160k (2 Solos)

7 Married: CORP+NW

- Capacity: $60.5k

- Math: $10.75k (HSA + 2 Catch*) + $17.2k (2 IRAs) + $32.5k (401k)

8 Married: SOLOB+NW

- Capacity: $108.0k

- Math: $10.75k (HSA + 2 Catch*) + $17.2k (2 IRAs) + $80k (Solo)

9 Married: NW+NW

- Capacity: $10.75k

- Math: $10.75k (HSA + 2 Catch*)

IV. Household Scenarios/Capacity Dollars/Ages 60-63 (Super Catch-up)

k = $1,000; Capacity means maximum possible and not necessary what you will be able to get.

1 Single: NW

- Capacity: $5.4k

- Math: $5.4k (HSA)

2 Single: CORP

- Capacity: $49.75k

- Math: $5.4k (HSA) + $8.6k (IRA) + $35.75k (401k)

3 Single: SOLOB

- Capacity: $97.25k

- Math: $5.4k (HSA) + $8.6k (IRA) + $83.25k (Solo)

4 Married: CORP+CORP

- Capacity: $99.5k

- Math: $10.75k (HSA) + $17.2k (2 IRAs) + $71.5k (2 401ks)

5 Married: CORP+SOLOB

- Capacity: $147.0k

- Math: $10.75k (HSA) + $17.2k (2 IRAs) + $35.75k (401k) + $83.25k (Solo)

6 Married: SOLOB+SOLOB

- Capacity: $194.5k

- Math: $10.75k (HSA) + $17.2k (2 IRAs) + $166.5k (2 Solos)

7 Married: CORP+NW

- Capacity: $63.75k

- Math: $10.75k (HSA) + $17.2k (2 IRAs) + $35.75k (401k)

8 Married: SOLOB+NW

- Capacity: $111.25k

- Math: $10.75k (HSA) + $17.2k (2 IRAs) + $83.25k (Solo)

9 Married: NW+NW

- Capacity: $10.75k

- Math: $10.75k (HSA)

Example of how to Use the Household Capacity Lists I. through IV.

Let’s say I had a solo business and my wife worked for a company and had a 401K.

We are both 51 years old in this example.

- Choose list II. Household Scenarios/Capacity Dollars/Ages 50-54

Choose scenario 5 Married: CORP+SOLOB

- Capacity = $138.5k

- Math = $8.75k (HSA) + $17.2k (2 IRAs) + $32.5k (401k) + $80k (Solo)

- So as a starting point, we should consider the following for funding.

- 2 HSAs: max of $8,750 total

- 2 IRAs: 2 x ($7,500 + $1,100) = $17,200 (includes catch up contributions)

- 1 401k: $24,500 + $8,000 = $32,500 (not including the company match which typically will be a single percentage of salary).

- 1 solo 401k: $24,50o(employee) + up to [$72,000 – $24,500 = $47,500] (employer) +$8,000 catchup = maximum of $80,000

- If the solo business is an S corp, then the employer amount will be 25% x W2 salary up to $47,500

- Total = $8.75k +$17.2k + $32.5k + $80k = $138.5k

- So a potential funding capacity of $138,500 is available!

Nesting: The Combination of Legal and Tax Structures

Having

- established the various tax structures—from Qualified and Statutory plans to Philanthropic vehicles—and

- mapped out the Max Capacity for various household scenarios,

we can now discuss the power of combining these entities.

While the “Order of Operations” (Stacking) ensures you fund the right accounts at the right time, a powerful aspect of wealth management involves Nesting.

Nesting is the strategic process of layering legal entities (LLCs, Trusts) and tax structures (like 401ks, HSAs, and IRAs) together to create a multi-dimensional shield for your assets.

Often you’ll hear these legal or tax entities called wrappers because of how they can envelope or wrap around another entity.

The Nesting Principle: Layering Tax & Legal Entities

Nesting occurs when you place one container inside another to achieve three specific goals:

- Absolute Asset Protection,

- Extreme Privacy, and

- Probate Avoidance.

A tax-advantaged account (like a 401k or a Brokerage) is a Tax Wrapper.

An LLC or a Trust is a Legal Wrapper.

You can “wrap the wrapper” depending on your primary goal:

- If Privacy/Probate is Paramount:

- You wrap the asset in a Trust.

- This removes your name from the public title and ensures the asset skips the court system (probate) entirely when you pass away.

- If Protection is Paramount:

- You wrap the asset in an LLC.

- This creates a liability firewall.

- If the asset (like a business or rental) causes a problem, the damage is trapped inside the LLC and can’t reach your personal life.

- If Both are Needed:

- You nest the LLC inside the Trust.

- The LLC acts as the “armor” for daily life, and

- the Trust acts as the “key” that hands the armor to your heirs privately.

Examples

Here are 4 examples of how we could wrap one entity into another entity for purposes of liability protection, privacy, and wealth transfer.

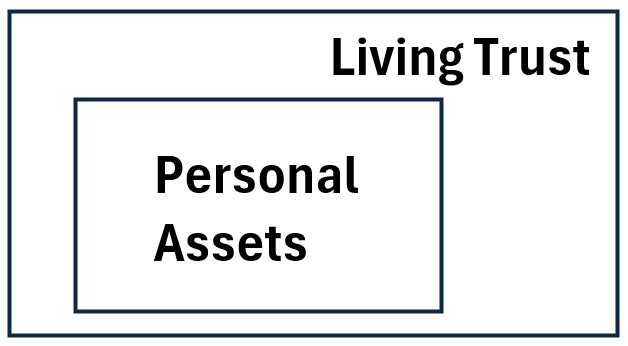

1. The Direct Family Trust (No LLC)

Goal: Privacy + Probate Avoidance.

- The Wrapper (Revocable Living Trust): Directly holds the title to assets.

- The Nested Assets: Your primary home (depends!), personal bank accounts, or heirlooms.

- The Benefit:

- Since there is no business risk, you don’t need a liability shield.

- This wrapper ensures that when you pass away, your assets transfer to your family privately and instantly without a public court process (probate).

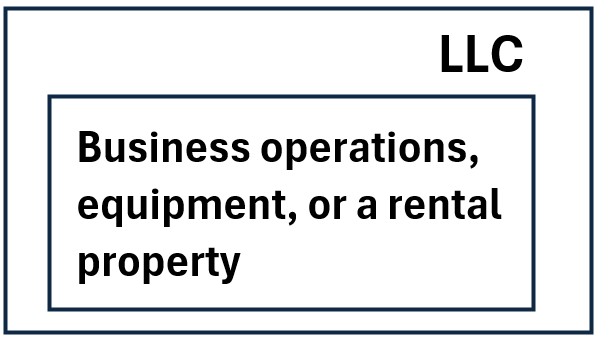

2. The Standard LLC (No Trust)

Picture: LLC of a business, equipment, rental, etc.

Goal: Asset Protection + Liability Shield.

- The Wrapper (LLC): Acts as a legal “wall” between your work and your life.

- The Nested Assets: Your business operations, equipment, or a rental property.

- The Benefit:

- If the business is sued, the liability is trapped inside the LLC wrapper.

- It cannot “leak” out to touch your personal home or savings.

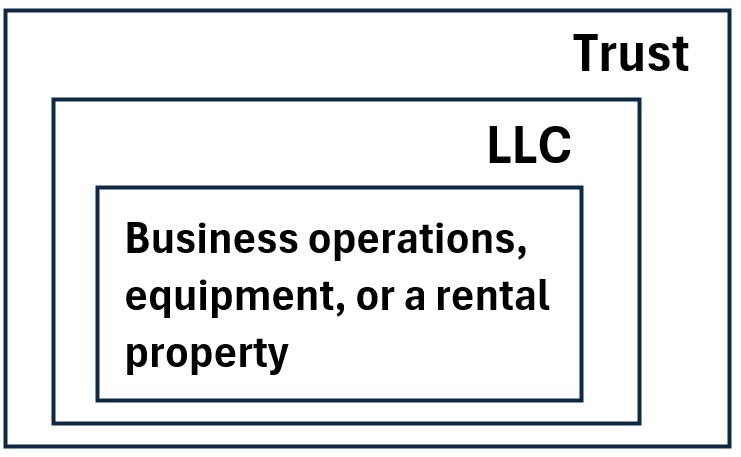

3. The “Privacy Shield” (Trust + LLC)

Picture: LCC inside a Trust

Goal: Anonymity + Liability Protection.

- The Inner Wrapper (LLC): Holds the risky asset (like a rental house).

- The Outer Wrapper (Anonymous Trust): Owns the LLC.

- The Benefit:

- On public records, the property is owned by an LLC, and the LLC is owned by a Trust.

- Your name is nowhere to be found, making it difficult for “lawsuit hunters” to see what you own.

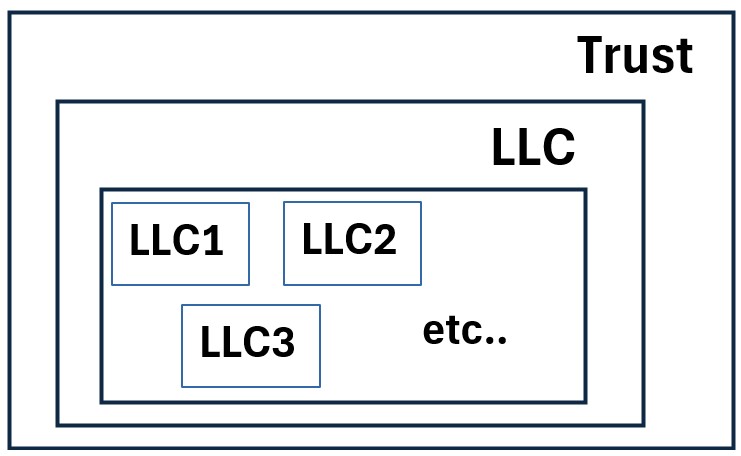

4. The “Full Legacy” (The Triple-Nested Structure)

Picture: Multiple LLCs inside a Holding LLC inside a Trust

Goal: Total Protection + Wealth Transfer + Tax Efficiency.

- The Inner Layer (LLCs): Holds the specific businesses or properties.

- The Middle Layer (Family Holding LLC): Consolidates everything into one management unit.

- The Outer Layer (Irrevocable Trust): Owns the Holding LLC.

The Benefit:

You get the liability protection of the LLCs, the centralized control of the Holding Company, and the estate tax benefits and permanent legacy protection of the Irrevocable Trust.

The Bottom Line

We are just barely touching the surface of this topic.

Entity layering is a massive field that can become incredibly powerful for shielding your “Max Capacity” savings from the eyes of the public and the reach of creditors.

But remember, any plan is better than no plan.

You don’t need to build a three-layer fortress today—simply adding an Umbrella Policy for immediate protection and possibly an asset trust for privacy would be a great start.