Introduction

A financial plan is only as strong as its weakest link.

To move from financial instability to long-term wealth, you need a repeatable framework that accounts for math, taxes, and human psychology.

The following four-phase roadmap provides a direct, step-by-step path:

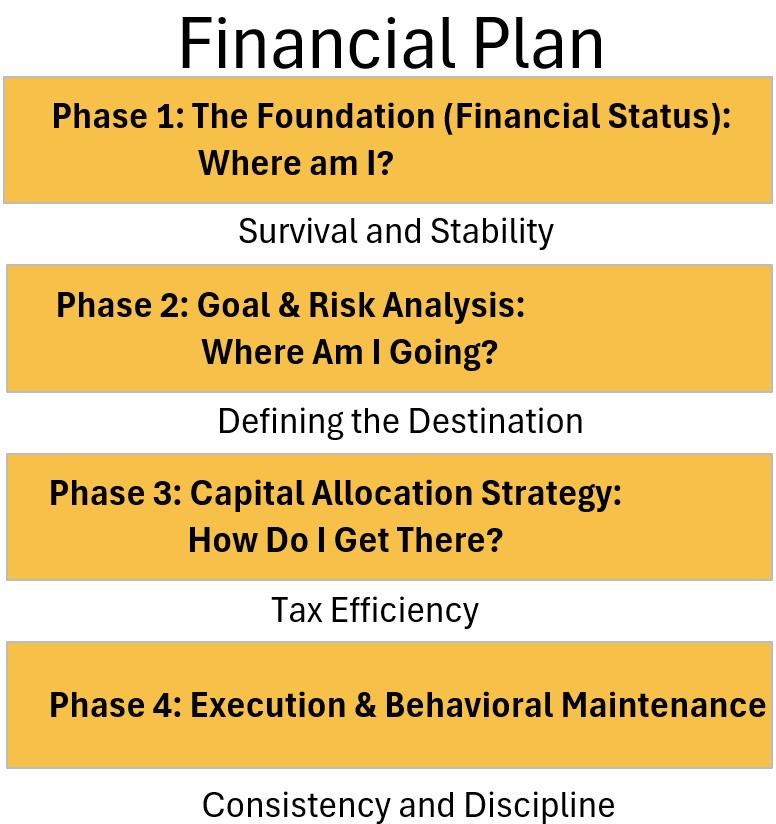

Table: Financial Plan Phases

Phase 1: The Foundation (Financial Status)

- Start with a rock-solid foundation.

- Theme: Survival and Stability

This initial stage is about stripping away ambiguity to understand your current net worth, cash flow, and immediate liabilities.

By establishing a “ground zero,” you create the security necessary to move from reactive survival—like managing high-interest debt—to proactive stability.

The focus here is on building a cash reserve that acts as a buffer against life’s unpredictability.

Phase 2: Goal & Risk Analysis

- Define your retirement target.

- Theme: Defining the Destination

Once the floor is leveled, you must determine the specific “why” behind your wealth-building, whether that is early retirement, a primary residence, or legacy planning.

This phase involves quantifying your time horizon and your emotional capacity for market volatility.

Mapping out these variables transforms vague desires into a concrete mathematical target and a risk profile that prevents panic during market downturns.

Phase 3: Capital Allocation Strategy

- “Stack” your capital into the most tax-efficient accounts

- Theme: Tax Efficiency

With a destination in mind, you select the specific vehicles—such as 401(k)s, IRAs, or brokerage accounts—that will carry your capital toward your goals.

High-level strategy focuses on optimizing “asset location” to minimize the long-term erosion caused by taxes and fees.

Choosing between tax-deferred and tax-exempt accounts, like a Roth IRA, ensures that you keep the maximum amount of your compound growth.

Phase 4: Execution & Behavioral Maintenance

- Automate the behavioral discipline required to stay the course.

- Theme: Consistency and Discipline

The final phase is the longest, requiring the automation of contributions and the emotional fortitude to ignore short-term market noise.

Success here isn’t about brilliant timing, but rather the boring, repetitive habit of staying invested through various economic cycles.

It is the bridge between a well-designed plan on paper and the actual realization of financial independence.

Before I address each phase with a little more data, the next section contains a template of the whole process that you can print out or copy.

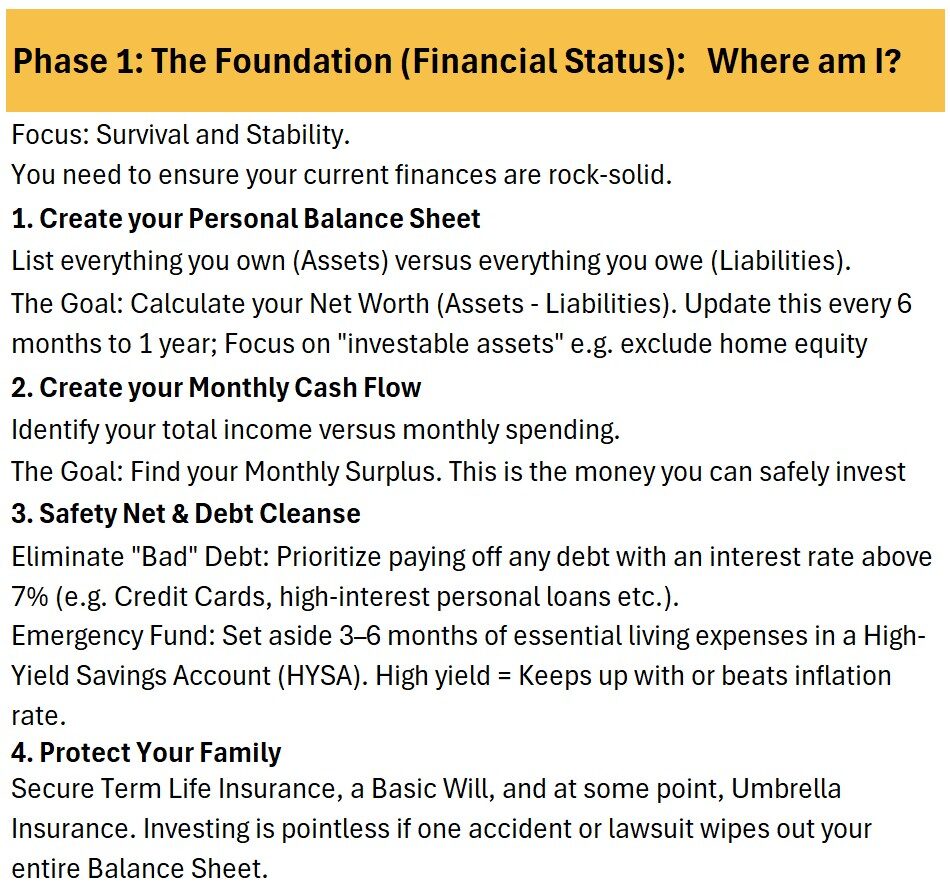

Financial Plan Phase 1: The Foundation (Financial Status)

Objective: Establish survival and stability.

Develop a budget and update it on some frequency.

Compute and track your net worth.

Before investing, you must secure your current position by auditing your

- Personal Balance Sheet (investable assets vs. liabilities) and

- calculating your Monthly Cash Flow. The goal is to identify a reliable monthly surplus.

- See Appendix 1 for a cash flow (budgeting) template and

- See Appendix 2 for a personal balance sheet (net worth calculator) template

Immediate actions include:

- Debt Cleanse: Eliminating “bad” debt (interest > 7%)

- Liquidity: Building a 3–6 month emergency fund in a High-Yield Savings Account.

- Risk Mitigation: Securing term life, a basic will, and umbrella insurance (when needed) to protect assets from catastrophic loss.

- See Appendix 3 for more on term life insurance and umbrella insurance.

Table Financial Plan Phase 1: Determine Your Financial Status

A monthly cash flow analysis might seem a bit too much, so don’t worry about following the exact guideline.

Depending on your situation and your familiarity with your budget, you can adjust the update frequency as needed.

The important thing is to get started and start getting familiar with your specific financial condition.

You can’t change or improve what you don’t monitor.

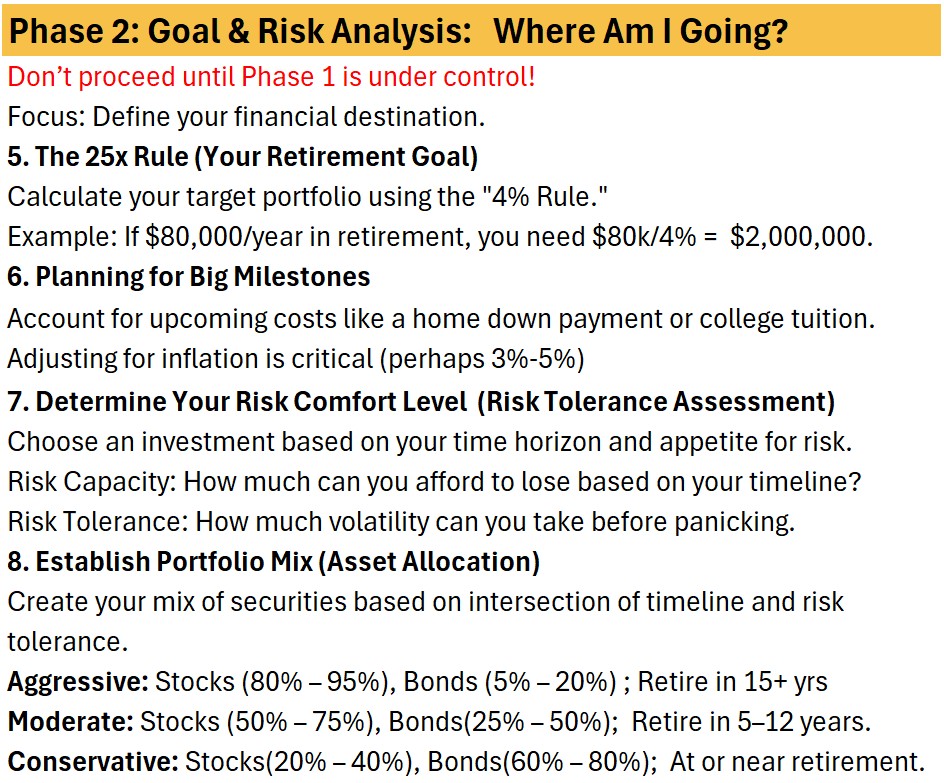

Financial Plan Phase 2: Goal & Risk Analysis

Objective: Define the destination and the vehicle/s.

Once you know where you are, you can start figuring out where you want to go.

Use the 25x Rule (4% withdrawal rate) to determine your target retirement amount.

See my post: Bang for your Bengen: The 4 Percent Rule

Account for major milestones like tuition or real estate, adjusting for a 3–5% inflation rate.

Understand your risk tolerance and design a basic Investment asset allocation.

Your Asset Allocation is built at the intersection of:

- Risk Capacity: Your mathematical ability to weather losses based on time horizon.

- Risk Tolerance: Your psychological ability to handle volatility.

- Portfolio mixes should shift from aggressive (80–95% stocks) to conservative (20–40% stocks) as you approach your target retirement date.

Table: Financial Plan Phase 2: Goal and Risk Analysis

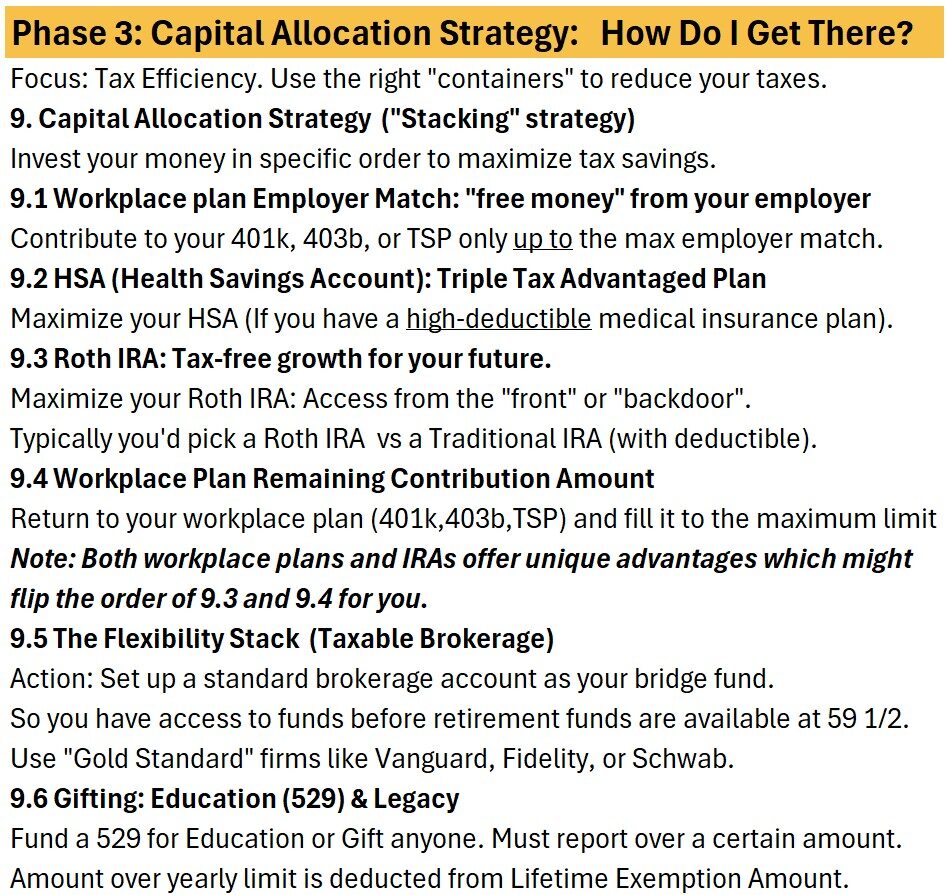

Financial Plan Phase 3: Capital Allocation Strategy

Objective: Maximize tax efficiency through “stacking.”

To optimize every dollar, assets should be deployed into specific “containers” starting with the order provided below.

See my post Tax Advantaged Plans and Other Capital Allocation Structures for more details on the various legal and tax related containers (wrappers, buckets, entities, vehicles) available to you.

Focus: Tax Efficiency. Use the right “containers” to reduce your taxes.

1. Workplace plan Employer Match: “free money” from your employer.

- Contribute to your 401k, 403b, or TSP only up to the max employer match.

2. HSA (Health Savings Account): Triple Tax Advantaged Plan.

- Maximize your HSA (If you have a high-deductible medical insurance plan).

3. Roth IRA: Tax-free growth for your future.

- Maximize your Roth IRA: Access from the “front” or “backdoor”.

- Typically you’d pick a Roth IRA vs a Traditional IRA (with deductible).

4. Workplace Plan Remaining Contribution Amount.

- Return to your workplace plan (401k,403b,TSP) and fill it to the maximum limit.

- Note: Both workplace plans and IRAs offer unique advantages which might flip the order of 3 and 4 for you.

5. The Flexibility Stack (Taxable Brokerage)

- Action: Set up a standard brokerage account as your bridge fund.

- So you have access to funds before retirement funds are available at 59 1/2.

- Use “Gold Standard” firms like Vanguard, Fidelity, or Schwab.

6. Gifting: Education (529) & Legacy

- Fund a 529 for Education or Gift anyone. Must report over a certain amount.

- Amount over yearly limit is deducted from Lifetime Exemption Amount.

You’ll probably have to tailor the above for your specific situation and the specific versions of the rules for the year in question.

So take this as a starting point.

And as I mentioned, see my article Tax Advantaged Plans and Other Capital Allocation Structures for much more on the various types of containers available.

Table: Financial Plan Phase 3: Capital Allocation Strategy

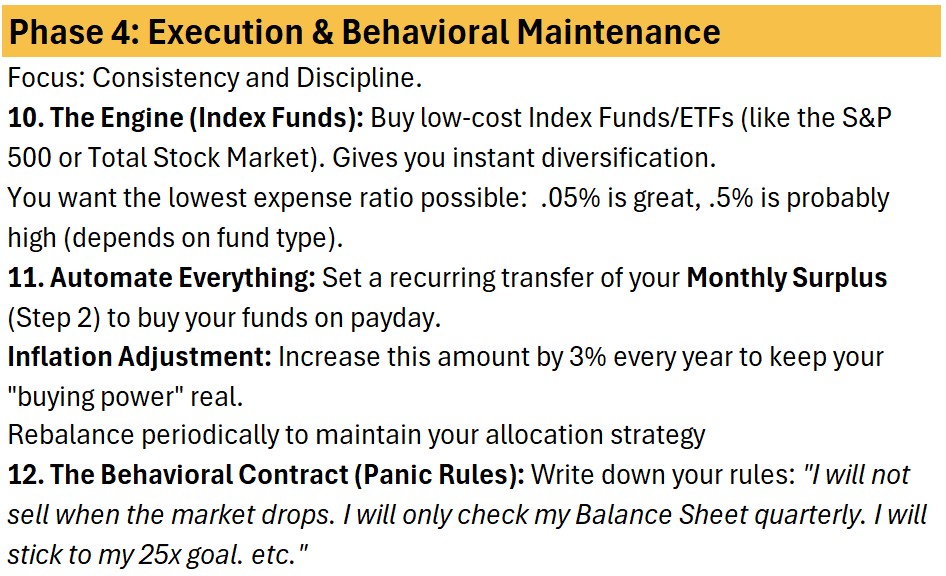

Financial Plan Phase 4: Operational Consistency

Objective: Disciplined execution and automation.

Strategy fails without a repeatable process.

Utilize low-cost Index Funds (targeting expense ratios near 0.05%) to achieve instant diversification.

- Automation: Set recurring transfers of your monthly surplus to trigger on payday.

- Inflation Scaling: Increase contributions by 3% annually to maintain purchasing power.

- Behavioral Governance: Establish a “Behavioral Contract” to prevent emotional selling during market volatility and restrict portfolio reviews to a quarterly basis.

I may have browsed over the following comment, but I thought it important to mention that term life insurance should be considered when others depend on you for financial reasons and/or stability vs a single person. Hopefully this is self explanatory. Additional details could be mentioned as to the amount of term life insurance you need, but for now, simply research this topic and customize accordingly. Overall article is a solid basis or guideline.

Thanks man. I added a linked appendix 3 describing the basics of term life and also umbrella policies.